fra OfTwoMinds blog,

Can the stock market completely ignore these changes and keep powering higher on the fumes of Mario Draghi’s promises?

Judging by October’s rocket launch, the stock market is back to where it should be, i.e. in rally mode. Yee-haw! All it took to keep the party going was another rate cut in China, another “whatever it takes” assurance from Mario Draghi and blowout earnings from a few tech giants.

So we seem to be right back we we’ve been for seven years: more central bank easing triggers more stock market mania, and stock buybacks and “earnings surprises” push stock valuations ever higher.

But a couple of things have changed recently:

1. China’s expansion has ground to a halt. China’s insatiable demand for commodities and capital has pulled the global economy’s cart for seven long years. Now that this demand is faltering, there is no equivalent economic/financial engine of demand to replace it.

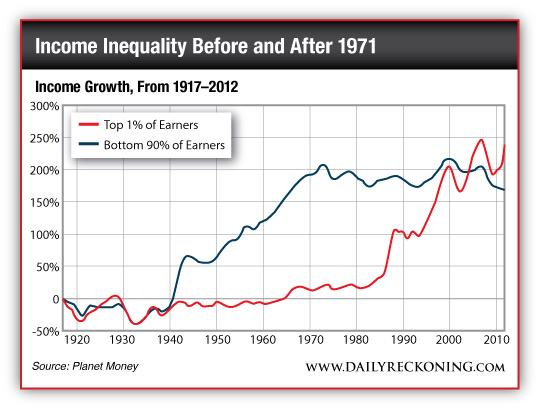

2. Income for the bottom 90% in the developed world is stagnant/declining. The most basic assumption of central bank monetary policies since 2008 (QE, etc.) was that household income would rise as the economy recovered, enabling more household consumption/debt.

This has not turned out to be true: for a variety of structural reasons, income of the bottom 90% of households has actually declined since 2000 when adjusted for official inflation.

3. The “wealth effect” from boosting global stock and junk-bond markets has been very limited. The second basic assumption of central bank monetary policies since 2008 was that the rise in financial assets (stocks, bonds and real estate) would “trickle down” to households who would respond to the psychological sense of increasing wealth by borrowing and consuming more.

What actually happened was the assets of the bottom 90% were gutted in the crashes of 2000-02 and 2008-09 and in many cases never recovered.

In terms of stocks, many in the bottom 90% decided against gambling money in the stock market after being wiped out by the dot-com crash. As a result, they missed out on the extraordinary gains of the past seven years.

Many of those who traded up in the housing bubble of 2000-2008 and took on big mortgages found that the recovery in housing prices has at best restored their marginal equity but hasn’t enriched them (with the exception of those who managed to buy in Manhattan, West L.A., San Francisco, etc., where gains have now exceeded the 2007 highs).

Millions of households that do not own homes in these hyper-hot globally attractive (and relatively small) markets are either still under water (they owe more than the home is worth after commissions and closing costs), or their equity is so limited that it doesn’t create a “wealth effect.”

4. None of the structural problems that triggered the 2008 Global Financial Meltdown have actually been fixed. I don’t mean risky banking or lending fraud, as destructive as these were–I mean the demographics that have mooted the entire financial foundation of pensions, the rise in healthcare costs (let’s estimate 750 million Baby Boomers globally are going to retire and need more medical care–75 million in the US alone), the unstoppable rise of automation that replaces human labor, the environmental disasters that have been papered over but not actually solved–the list is long.

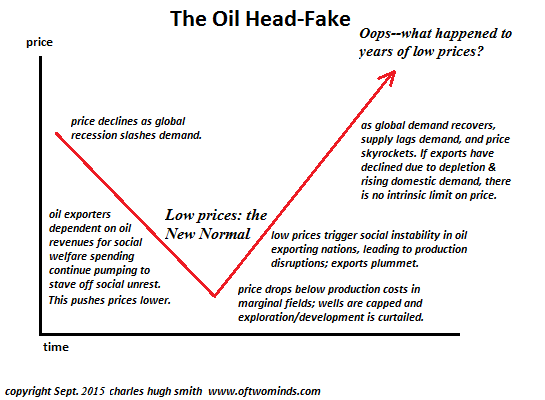

5. The Oil Head-Fake I have often described is playing out. As demand plummets, oil producers have no choice but to keep producing to service their debts or fund their social welfare program costs. This sets up a mismatch in demand and supply that has pushed energy prices lower, gutting the budgets of oil exporters and crushing their currencies.

The Decline of Oil: Head-Fake or New Normal? (September 9, 2015)

So the question going forward is: can the stock market completely ignore these changes and keep powering higher on the fumes of Mario Draghi’s promises and another rate cut or three in China?

At some point reality will trump fumes, and the manic rally will falter and the mania in stocks will end in tears.