Fra Zerohedge

Last week’s non-committal ECB announcement caught markets by surprise, with the Euro jumping despite Mario Draghi’s best attempts to signal further easing even as he hinted at growing “downside risks”, prompting speculation that the ECB may have lost the last shreds of its credibility and leading Rabobank to publish a piece titled “Whatever It Takes” > “Whatever“.”

Not used to being spurred by markets, Mario Draghi refused to take such aggression against his legacy quietly – especially as the former Goldman partner is set to retire shortly – and on Sunday, the European Central Bank used its traditional trial balloon conduit, Reuters, which reported that ECB policymakers “are open to cutting the ECB’s policy rate again” if economic growth weakens in the rest of the year and a strong euro hurts a bloc already bearing the brunt of a global trade war, clearly hoping that this jawboning would be sufficient to slam the euro (it wasn’t with the EURUSD basically unchanged from its Friday close).

As a reminder, last Thursday the ECB said that its interest rates would stay “at their present levels” until mid-2020 but President Mario Draghi added rate setters had started a discussion about a possible cut or fresh bond purchases to stimulate inflation.

This conflicting message failed to convince some investors, who saw it as too tenuous a commitment to more stimulus, sending the euro rallying to a nearly 3 month high of $1.1347 against the U.S. dollar.

So in an attempt to convince the skeptics, Reuters cited its traditionally anonymous “two sources” familiar with the ECB’s policy discussions, who said a rate cut was firmly in play if the bloc’s economy was to stagnate again after expanding by 0.4% in the first quarter of the year.

“If inflation and growth slow, then a rate cut is warranted,” said one of the sources, who requested anonymity because the ECB’s deliberations are confidential.

The problem is that no matter what Draghi says, or “floats”, the market is concerned that the ECB is approaching the end of its credible ammo: with the ECB’s deposit rate already negative 40 bps and Germany’s yield hitting all time low. In this context, countering the euro’s strength, rather than lowering already rock-bottom borrowing costs, would be the main reason for a further cut to that deposit rate, one of the sources said.

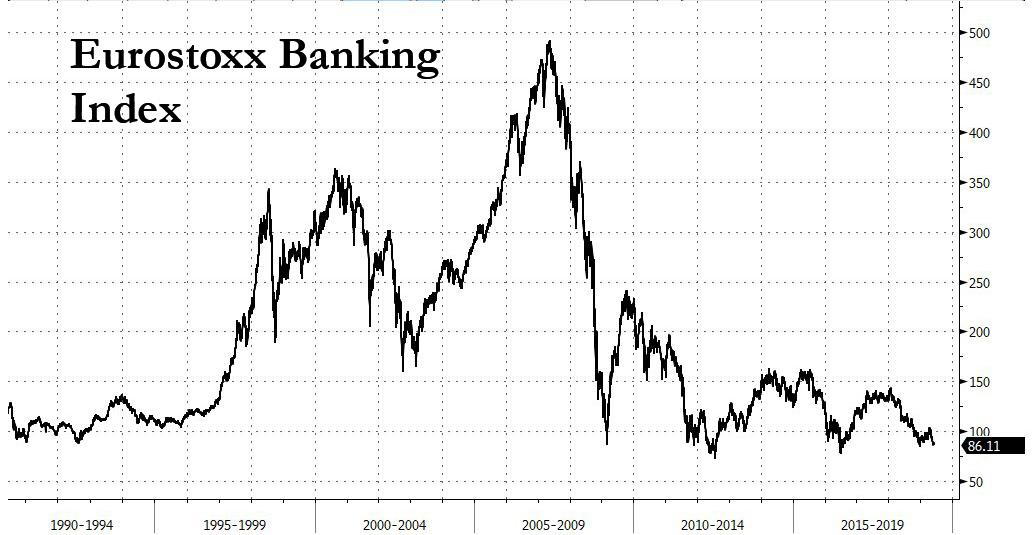

But how can the ECB pursue a “surgical” devaluation of the euro (amusingly nobody ever accused the central bank of manipulating its currency when in reality that is all it does) without also slamming government bond yields which have made Europe’s entire banking system into a NIRP zombie trading near record low levels?

“I’ll give you five reasons for a rate cut,” the source said before repeating “exchange rate” five times.

While the ECB doesn’t formally admit it targets an exchange rate – just like every other central bank – Draghi noted the euro’s appreciation in his news conference on Thursday and has long highlighted the currency as a crucial determinant of financing conditions.

So what FX level could trigger the ECB to move?

The Reuters source said a euro at $1.15 would still be tolerable for some but $1.20 would be a critical level to watch. And now that the bogey has been set, the market will certainly test the ECB’s resolve.

The bigger problem facing Europe is… the US. The comnmon currency has risen by 2% against the dollar in just over a week as the Federal Reserve itself signaled its willingness to cut its interest rates if needed. This, in turn, was seen by some analysts such as those from Goldman, as a sign the U.S. central bank was bowing to pressure from the White House to keep the dollar weak and strengthen the administration’s hand in its trade negotiations. Furthermore, Italy’s central bank governor Ignazio Visco also blamed the euro’s surge after the ECB’s latest decision on “interactions with U.S. interest rates”.

That said, even Reuters conceded that the argument for more quantitative easing from the ECB was less clear to some policymakers, according to the “sources.” One of them said more QE could help soothe stock markets if these were spooked by an escalation in the trade war, although there would be a risk for the ECB in appearing to kowtow to equity investors (not like that has ever stopped central banks, which in recent years have largely admitted their only mandate is preserving a levitating stock market).

Ironically, the other said the main benefit of QE was compressing the difference between short- and long-term borrowing costs, making access to finance easier for companies and households, but this so-called term premium was already low. What he meant is that should the ECB cut rates even more, European banks – already on the edge – will start toppling over like dominoes as the bank business model no longer works under a NIRP regime.

As such it will be poetic irony that the same central banks that launched unprecedented “unorthodox” policies to preserve the world’s banking giants a decade ago, will be the culprits behind the wholesale devastation of these same banks. Luckily for Mario Draghi, he will be far away, merrily enjoying his retirement on the shores of one of central Europe’s scenic (if not too secluded) lakes. His successor however, will not be so lucky.