Fra Zerohedge:

Following the US Services sector’s collapse (and Canada and China’s plunge), US Manufacturing’s soft survey data tumbled in May.

The headline PMI fell to its lowest level since September 2009 as output growth eased (with output expectations crashing to the joint-lowest since records began) and new orders fell for the first time since August 2009.

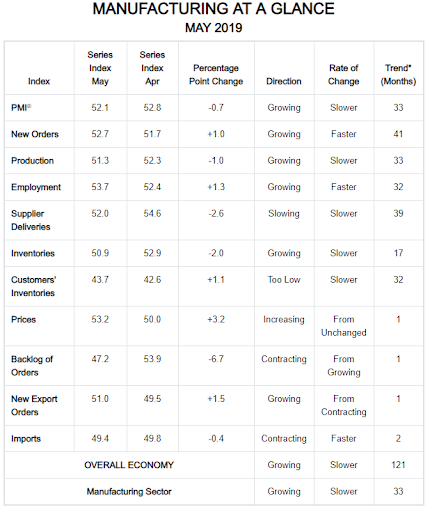

The ISM Manufacturing print also disappointed at 52.1 (53.0 exp), the weakest since Oct 2016 (despite a rise in new export orders and employment)

Three of five ISM components declined, including production, inventories and supplier deliveries,and stagflation looms as prices paid rose.

ISM’s production gauge dropped to 51.3 in May, the lowest level since August 2016, even as the gauge of backlogs declined to a two-year low.

As Bloomberg notes, the ISM index’s lowest reading of Trump’s presidency — down from a 14-year high in August — follows a slew of other economic data that suggest the sector was on shakier ground even before the latest escalation of tariffs between the U.S. and China began to pinch margins.

Respondents are unanimous in their tariff tantrums…

“Ongoing tariffs [issue is] impacting costs and influencing supplier realignment on country of origin. Border issue is causing delays in imports from Mexico.” (Computer & Electronic Products)

“The threat of additional tariffs has forced a change in our supply chain strategy; we are shifting business from China to Mexico, which will not increase the number of U.S. jobs.” (Chemical Products)

“Sales continue to decline. Volumes are off, [and] profits haven’t decreased in proportion to sales. Higher-margin vehicles continue strong sales, but low- to mid-range sales are down.” (Transportation Equipment)

“The threat of a 15-percent increase on Section 301 tariffs is a concern. Although the potential has been around for months, the recent deadline was not expected. We had calculated and communicated the potential cost impact to our leadership.” (Petroleum & Coal Products)

As Chris Williamson, Chief Business Economist at IHS Markit, noted:

“May saw US manufacturers endure the toughest month in nearly ten years, with the headline PMI down to its lowest since the height of the global financial crisis. New orders are falling at a rate not seen since 2009, causing increasing numbers of firms to cut production and employment. At current levels, the survey is consistent with the official measure of manufacturing output falling at an increased rate in the second quarter, meaning production is set to act as a further drag on GDP, with factory payroll numbers likewise in decline.

“While tariffs were widely reported as having dampened demand and pushed costs higher, both producers and their suppliers often reported the need to hold selling prices lower amid lacklustre demand. While this bodes well for inflation, profit margins are clearly being squeezed as a result.

“With future optimism sliding sharply lower in May, risks to nearterm growth have shifted further to the downside.

“While companies of all sizes are struggling, the biggest change since the strong growth seen late last year is a deteriorating performance among larger companies, where surging order book growth just a few months ago has now turned into contraction, the first such decline seen in the series’ ten-year history.”