FRA MAULDIN

The World Is Slowing Down

Jeffrey Snider of Alhambra Investment Partners sent out a note last week highlighting some of the current conditions. In his piece entitled “Not Just Manufacturing, the Global Slowdown Is Monetary,” Jeffrey cites a Wall Street Journal article that highlights the very serious slowdown in orders for new big rigs and other trucks. Inventories are at their highest level since before the financial crisis, and sales in March were down 37% from a year ago as fleets remained very cautious about expanding in this environment. Quoting:

Some of this reduction in 2016, as the Journal reports, is due to companies over-ordering in 2014 and 2015 based on the narrative that the economy was actually healing, or at worse would stay in its “new normal.” It raises the issue as to whether these conditions and the manufacturing recession they reflect are cyclical or structural, or both.

As I wrote yesterday, the contraction in goods and the US economy’s basis for them may or may not be heading toward recession. It is clear, however, that whatever the ultimate cycle reality, there are deeper imbalances that run back several years, likely traced to decades of financialization that is now overturning, and thus really supersedes cyclical discussion. What we see in the US is not limited to the US, however; it is a global phenomenon, which can only mean one possible explanation.

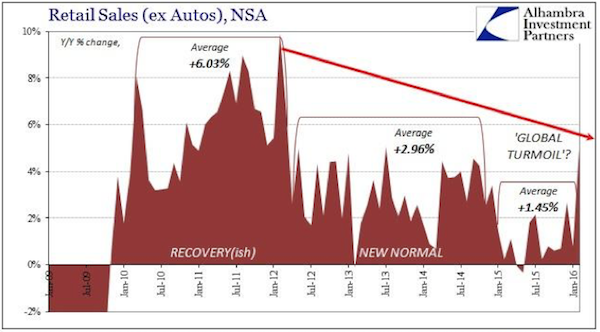

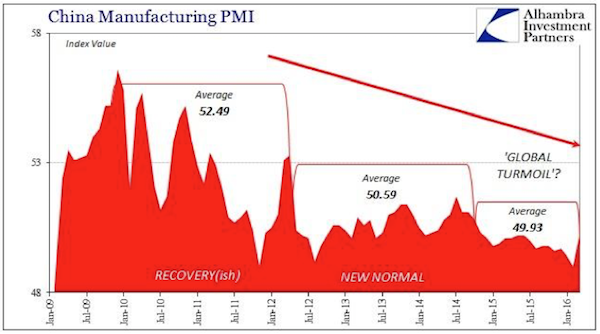

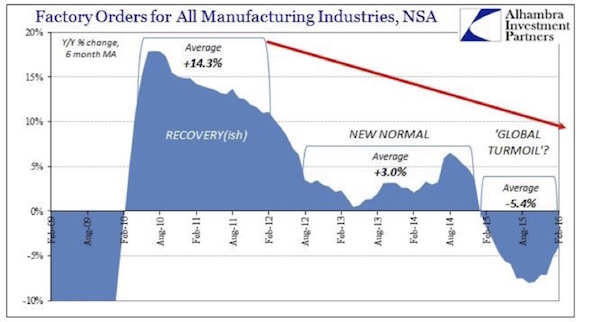

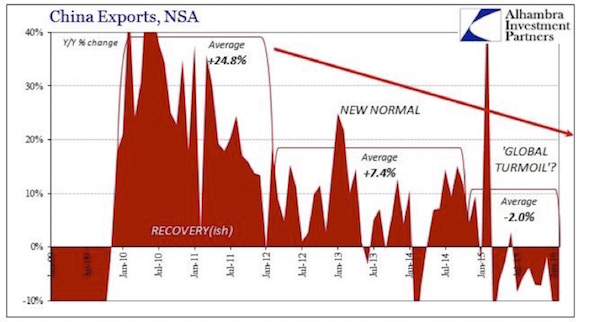

Jeffrey offers several charts that I think tell the story better than 1,000 words.

These charts have slowdown written all over them. And you can see the trend even more clearly when you look at factory orders on a non-seasonally adjusted basis over the years since the recovery:

The slowdown is not limited to the US. Look at what is happening to China exports:

The latest quarterly edition of the China Beige Book was out yesterday. The China Beige Book is just about the only true gauge of the Chinese economy. My good friend Leland Miller’s firm surveys 2200 Chinese companies every quarter and reports on their findings. Their work is a must-read in serious economic circles. Leland, one of the savviest experts on China there is, provided me with a summary:

Led by rising layoffs at private firms, job growth dropped notably for the second consecutive quarter, sliding to a four-year low. Expectations of future hiring took a similar dive. Overall, the share of firms hiring this quarter fell to half of what we reported in 2012.

This deterioration has wide-ranging implications. Despite the economy’s overall deceleration, China has been able to defy calls to be more aggressive – either via reform or stimulus – because of the remarkable stability of its labor market.

This bought time, but Beijing hasn’t used it wisely. If the weakness in employment continues, the credibility of government policy will be challenged by those who matter most: not financial commentators but ordinary Chinese.

Leland went on to point out that this slowdown in hiring has been brought about by two rather uncomfortable trends: First, the multiyear slowdown in capital expenditures is continuing, and now we have seen what almost amounts to a crash as the number of companies reporting capital expenditure growth has plummeted by 40%. Reduced capital expenditures, of course, affect hiring.

And companies, particularly private companies, are borrowing less. Money is available, but they simply don’t want it. They’re trying to square up their balance sheets. Other anecdotal evidence from private sources suggests that what borrowing there is, is being used to pay off dollar-denominated debt. The debt-fueled growth that has driven China for these past seven years, sputtering on fumes now, seems headed for an abrupt end. Likewise, the shift from manufacturing to services seems to have lost momentum.

The government still reports 6.7% GDP growth, but as Leland notes, China’s weakness is not about GDP:

With perceptions about China likely to guide global markets again in 2016, it has become more important for investors to look beyond headline GDP numbers – official or private. After all, Beijing didn’t seem overly concerned when many indicators signaled weakness but job growth remained steady. If the opposite combination persists, China’s purported restructuring and reform could lose the faith not only of markets, but also of the masses.

I will be writing a detailed letter on Europe in the near future, and quite frankly I view the European economy to be even more problematic than China’s is.

Brazil is clearly mired in a recession, amid political turmoil. Commodity-market economies have recovered a little bit as prices have bounced off their lows. But the massive dollar-denominated debt in emerging markets is starting to come due, and most EM currencies are much weaker than they were when the debt was initially taken on. Major economic problems are brewing in a number of countries.

I know the equity markets are close to all-time highs, but I also see real interest rates negative out beyond 10 years and certainly below 1% even out to 30 years. Those are not conditions that you see in a dynamic, growing economy.

As I’ve been saying for almost two years, the admittedly weak US data still doesn’t give me any real conviction about a particular timeline for a recession in the US. But with the US economy barely growing at stall speed, an exogenous shock to the US economy could easily push us into recession. Whenever the next recession comes, it will not look like the last recession.

In my last two letters I offered a prescription for how to avoid a recession in the United States and how to trigger a new era of growth. Doing so would allow (or perhaps force) the Federal Reserve to normalize interest rates, which would allow savers to benefit once again from their years of saving. Pension funds and insurance companies would actually regain the chance to provide the benefits they have promised.

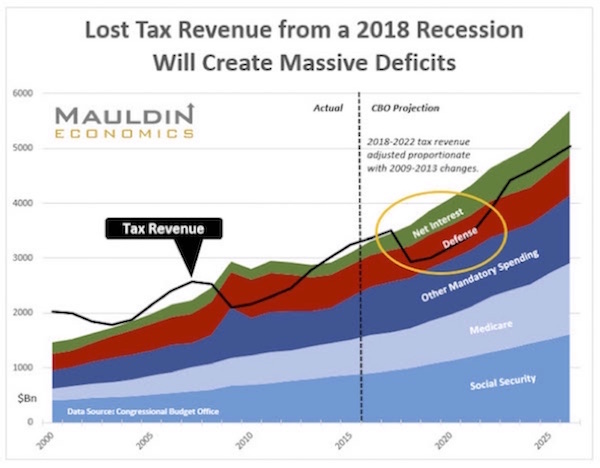

We may not see a recession this year, and hopefully not even next year – though that’s a hope and not a prediction – but sooner or later we’re going to see one; and if we haven’t completely revamped our incentive and tax structures, allowing the Fed to normalize rates, monetary policy will be impotent during the next recession, and Congress will be facing $1.5 trillion deficits with very little room to provide any real stimulus. I know I have shown you the following chart in the last two or three letters, but I want you to burn this picture into your mind. This is what is going to happen to the federal deficit when we go into recession:

I have lived through six recessions in my business life – and that’s the point: we do live through them. This recent recovery has been the weakest we have seen in the last 40 years, and I will make you a side bet that absent any restructuring of the tax and incentive systems, the next recovery will be even weaker, with the real potential for the United States to catch “Japanese disease.”

But we will suffer the slow-growth, no-recovery symptoms of Japanese disease without the cushion that Japan’s massive savings and current account surplus provide. We won’t have 20 years to muddle through as Japan has done. Unemployment will rise to uncomfortable levels, and I fear that the Federal Reserve will begin to experiment with extreme forms of monetary policy, including negative interest rates. I acknowledge that there are very smart economists who think that negative rates can deliver positive benefits, but I simply think they are wrong. The evidence I’m looking at demonstrates that negative rates abuse savers and distort normal markets by obliterating the signals that the price of money (i.e., the interest rate) is supposed to send. The total financialization of the world’s reserve currency will not end well.

As I laid out in my last letters, our economic future doesn’t have to end this way. And candidly, the proposals I’ve suggested are not the only way that we can sort out our tax and incentive structures and achieve positive results. I can think of quite a few paths we could take. But just tinkering around the edges and more or less doing what were doing now is not going to get us where we need to go.

A recession is an avoidable dilemma, but averting the nasty economic storm that is brewing now will require leadership and compromise that haven’t been seen in Washington DC for some time. In general, the feedback I’ve gotten from my letter to the would-be president series has been quite good – much better than I expected. But the one real pushback from friends and readers is the very simple, skeptical question, “John, you don’t really think that this will happen, do you?”

Sadly, I must admit that I don’t. I am generally an optimistic person, and I would like to think that the people we elect this fall will do the right thing. But we’ve been saying that for about 16 years now. Our so-called leaders’ record on doing the right thing with regard the deficits and the economy is not cause for jubilation.

So, I think the more likely outcome is that we’ll have a recession and $1.5 trillion deficits and mountainous deficits as far as the eye can see, because it is really quite an impossible task to balance the budget without new taxes and growth incentives and without the massive fiscal stimulus that could come by repurchasing the Federal Reserve’s balance sheet to invest in infrastructure that would create 2 million+ jobs.

It was Rahm Emanual, the beleaguered current mayor of Chicago (why on God’s green earth did he want that job?), who once said, “Never let a good crisis go to waste.”

While the next recession will surely plunge us into a crisis, that crisis will afford an opportunity that those who want to restructure our federal government. The attempt will, quite frankly, require an end run around Congress. Thankfully, the founders of the republic stuck a helpful little section for that purpose into the Constitution. It’s called Article 5. It allows for 34 states to call a Convention of States to propose amendments to the Constitution, which then have to be sent back to the various state legislatures to win the approval of 38 states – no small feat. I will readily admit that it will take a crisis to push some of the needed states into the “let’s just do it” category. Getting 34 states to agree is a daunting task, but we might just get the crisis we need to accomplish that, and hopefully the country will not waste it.