Fra Zerohedge/Goldman

The Fed’s unprecedented attempt to hike rates out of the greatest recession since the Great Depression is over: and whether the Fed cuts in two weeks, or July, the futures market indicates a greater than 90% likelihood of at least one 25 bps rate cut in the funds rate by the end of 2019. In total, futures prices reflect 65 bps of expected easing during 2019 and an additional 30 bps of easing during 2020, reflecting a total of 4 rate cuts by the end of 2020.

Even more unprecedented, the market-implied year-end 2020 funds rate has plunged to 1.45%, down 85 bps since early March and 15 bps during the past week after Fed chair Powell said on Tuesday that the Fed would monitor developments on the trade conflict and “act as appropriate.”

And yet, despite broader market expectations of easier policy, professional forecasters remain less convinced according to Goldman’s David Kostin. According to FactSet data, 30 professional forecasters have revised or reconfirmed their funds rate forecasts during the past two weeks. The median forecaster in this sample expects the funds rate to be unchanged by year-end 2019, with 13 respondents expecting some amount of easing. Goldman’s own economists’ base case forecast is the Fed does not cut interest rates during the next 2 years, but it does see mounting trade tensions as a source of downside risk that is likely to get worse before it gets better.

Some more observations from Goldman’s chief US equity strategist, who notes that since 1988, on 13 occasions the futures market expected a cut in the funds rate the day prior to a scheduled FOMC meeting. The Fed cut rates in all 13 instances. In other words, the Fed has always cut interest rates when the market priced a cut on the day prior to a FOMC meeting.

And while as noted above, futures prices currently imply an unchanged funds rate by the June 19th meeting, the market is pricing 20 bp of easing by the July 31st meeting, nearly 40 bps by the September 18th meeting, and 65 bp by the December 11th FOMC meeting. And, if Goldman is indeed right and the bulk of Wall Street is wrong, and the Fed does not intend to ease policy this year, history suggests it is likely to gradually walk back market expectations for easing in coming months rather than deliver a hawkish disappointment.

Going back to Goldman, the bank’s chief equity strategist says that there are two questions surrounding the rate cut debate as critical:

- (1) if professional forecasters are correct and the Fed does not cut rates, what should investors own as the Fed walks back market expectations for easing?; and

- (2) if the futures market is right and the Fed does cut rates, what has historically outperformed following the start of past interest rate cutting cycles?

As noted above, there is not a single precedent during the past 30 years where futures discounted an interest rate cut 30 days prior to a scheduled FOMC meeting but the Fed did not cut. February 1990 and February 1992 stand out as two experiences where the market unwound its earlier expectation for a cut by the time of the meeting. In both these cases the S&P 500 fell during the month ahead of the meeting (-5% in 1990 and -1% in 1992). Sector and factor performance were mixed. In a major difference from today, both of these episodes occurred in the middle of ongoing Fed rate easing cycles. Another difference: the market soared in the past week as the expectation of a rate cut swept through the market as the start of an easing cycle was priced in. But did that action effectively doom a Fed rate cut?

As we summarized the reflexive nature between the Fed and the market on Friday, “Fed won’t cut until stocks plunge, which won’t happen because the Fed will cut”

zerohedge@zerohedgeFed won’t cut until stocks plunge, which won’t happen because the Fed will cut

So let’s assume the Fed does cut either this month or in July, what happens then?

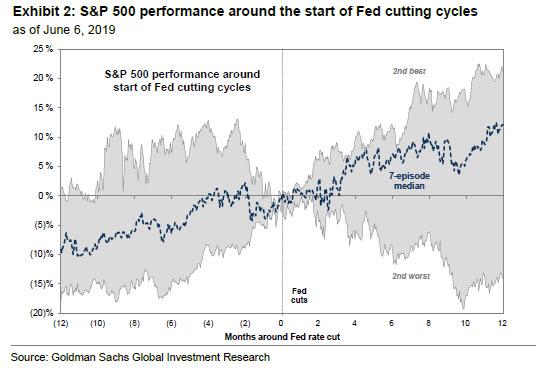

Well, as Kostin explains, to nobody’s shock, the S&P 500 has typically generated strong returns at the beginning of Fed cutting cycles:

We analyzed equity returns during the past 35 years following the start of 7 Fed cutting cycles, or the first interest rate cut during a trailing 12 month period. The index climbed by a median of 2% and 14% during the 3-and 12-month periods following the start of a Fed cutting cycle, respectively. Performance was strongest during the 12 months following the cuts in July 1995 and September 1998 (+23% in both instances), while the market declined following cuts in January 2001 (-12%) and September 2007 (-18%). We find roughly even contributions to returns from EPS growth and valuation expansion in the 5 cycles where the market rallied during the 12 months following a cut in interest rates.

Some more nuances observations on what works, and what doesn’t once the Fed starts cutting – and the Fed rarely if ever cuts “one and done” for a reason we will note below:

Among sectors, the defensive Health Care and Consumer Staples sectors performed best following the start of cutting cycles while Information Technology posted the worst returns(Exhibit 3). Health Care has outpaced S&P 500 by a median of 9 pp during the 12 months following the start of a Fed cutting cycle. Consumer Staples outperformed by a similar magnitude. The idiosyncratic Communication Services sector has generated the best relative returns and hit rate of outperformance during the subsequent 3 months (+4 pp, 100%), but has underperformed over a 12-month horizon. Info Tech ranks as the worst performing sector during the subsequent 12 months (-13 pp) [ZH: this is bad for a sector that has been the source of profit margin growth in the past decade].

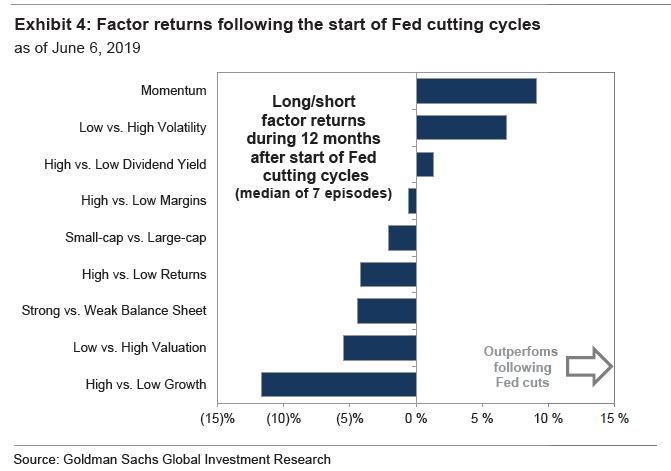

Thematically, momentum and low volatility have historically outperformed after the Fed begins to cut interest rates (Exhibit 4). Goldman’s long/short Momentum factor has returned a median of 9% during the 12 months following past rate cuts. Excluding the cuts in 1998 and 2001 that came as a surprise to investors (the market was pricing less than 12.5 bpof easing on the day before the meeting), Momentum has generated a median 13% return during the following 12 months. Both Momentum and low volatility performed extremely well last month (+10% and +9%, respectively). Growth has posted a strong 2019 YTD return but historically it has been the worst performing factor in the year after the start of Fed easing cycles, returning a median of -12% and falling in 5 of 7 episodes.

But while the market’s kneejerk response to a rate cut appears to be consistently higher – even if the market has fully priced in said rate cut as it has now – the reason why subsequent growth fades away is simple. As we first revealed in January, it is not the rate hikes that catalyze a recession, instead, the last three recessions all took place with 3 months of the first rate cut after a hiking cycle!

Which is why, if past is prologue, a July rate cut would mean that the next recession will start some time in November or December, and by the time of the presidential election in 2020, the US economy will be suffering a sharp contraction, hardly good news for the Trump presidential campaign.