Fra Zerohedge:

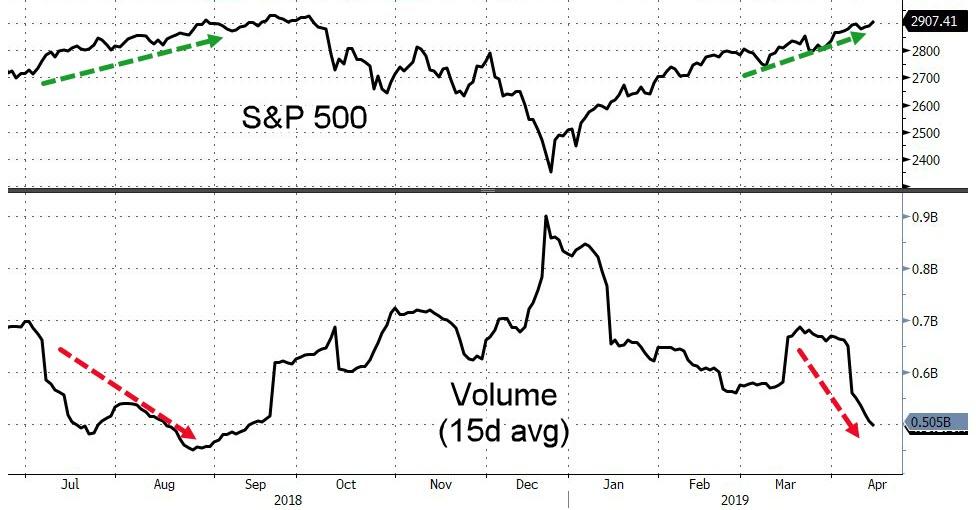

As stocks hit their 2019 highs on Friday, trading volumes collapsed to their weakest since the similar ramping equity gains in August that marked the previous peak…

But, as former fund manager Richard Breslow notes, it hasn’t been quite as calm as a cursory look at the overnight ranges and trading volumes might suggest.

But it should have been.

For every trading thesis out there, there is a counterpoint making the rounds.

Not in the sense of, it takes two to make a market.

Rather, as in, the global economic and geopolitical situation is so opaque that it’s getting harder and harder to gauge just how committed investors will remain to anything but short-term views.

It’s common to declare oneself to be data-dependent. But there is no consensus about what data we are meant to be watching.

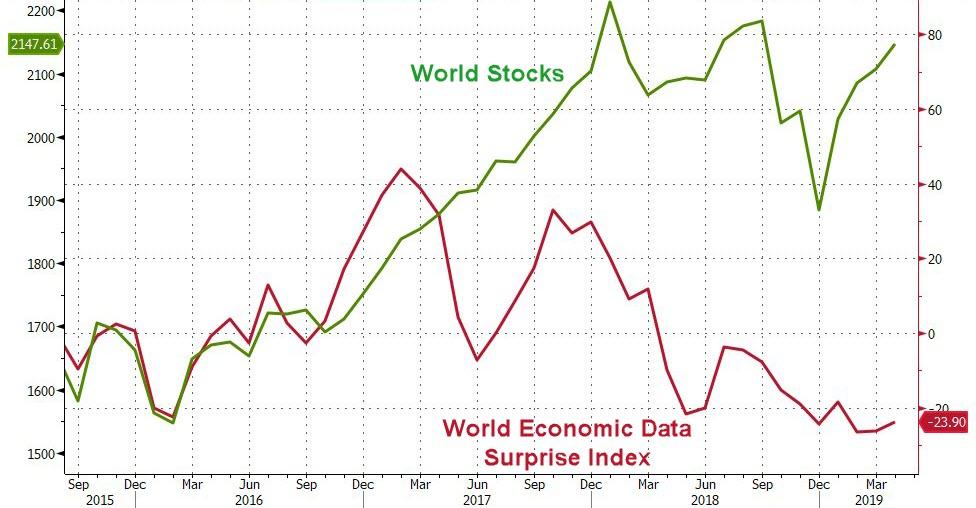

- The IMF continues to lower growth forecasts and warn about downside risks. Meanwhile, private economists continue to expect a second-half pick-up. The market is said to be priced too pessimistically and is getting ahead of itself on the possibility of rate cuts. Traders aren’t buying it. For them, “patience” isn’t a calming word.

- Progress on trade is promised on an almost daily basis. Yet the various fronts where the battle may be fought keep demonstrating that a solution isn’t so straightforward as a single bilateral negotiation. Just ask the Japanese as they come to the U.S. this week. Or better yet, try to figure out what was going through the minds of people trading Japanese assets last night.

- It was a strange day for the Topix index to decide to play catch-up with better performing exchanges elsewhere, the economic number beats out of China, notwithstanding. Ironically, the explosive gap higher for the Shanghai index on trade optimism, supposedly gave way in large part because traders posited that better numbers could make the PBOC less generous with stimulus. There is a lot of circular logic going on.

- One hot topic where there is broad consensus concerns central bank independence. Partially because the efforts to influence the Fed have been so ham-fisted. And there are few things that economists like to debate quite as much as something they all agree on. It’s an important issue, nonetheless. But only the threat it’s being portrayed as if the legislature and the FOMC allow themselves to be seen, let alone act, as enablers. Politicians trying to influence policy is certainly nothing new. Undue efforts, however, are unacceptable. And they don’t, in all cases, warrant extreme politeness in response.

- In a developed world desperately in search of inflation, it is a bad argument to warn that meddling might turn investors back into bond vigilantes. No one is going to sell 10-year Treasuries because of a rant. But they might if their Chairman meets with partisan politicians behind closed doors. Isn’t avoiding the appearance of improper influence an important part of the whole issue?

- I was looking at charts this morning. And one thing that struck me was the number of cases where the asset at hand looks like potential reversals of recent trends are a real possibility. But I can’t make the case that there is some generalized risk-on or off move coming. When you take a look, don’t focus on crowded trades. Emerging markets, for instance, still look reasonable. Even if not every opportunity within the asset class was created equally. Look for the trades, that everyone takes for granted. Oil might be a good place to start. Or go for the ones, like the dollar, that just haven’t been trading well lately. Whatever the story associated with it.