Uddrag fra Authers;

Regime change may be afoot in Iran. Decapitation in the successful killing of Ayatollah Ali Khamenei and a number of other senior leaders has already happened with breathtaking swiftness.

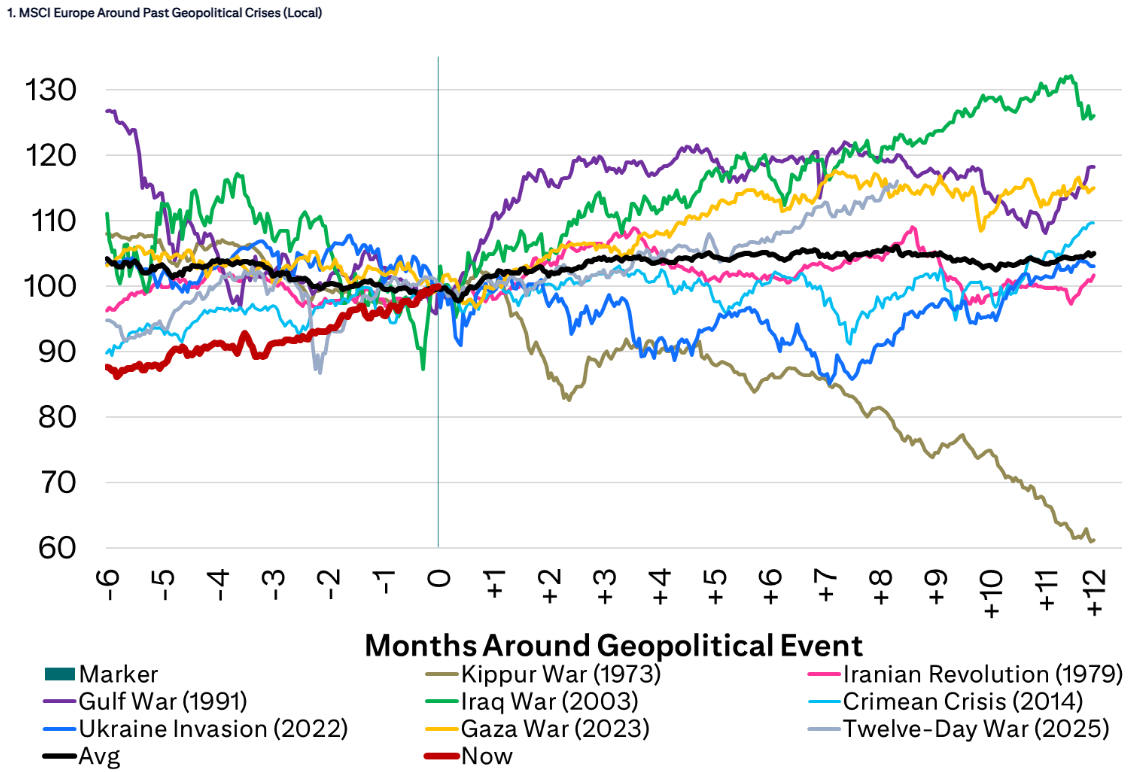

The range of potential longer-term consequences for the American role in the developing new world order, and for the balance of power in the Middle East, is equally breathtaking. But there’s no template. The breadth of responses to similar shocks in the past has been varied, as Citi demonstrates in this chart.

The huge outlier was the 1973 Yom Kippur War, which triggered a massive bear market. It was different from the others because it led to a protracted reduction in the supply of oil to the rest of the world. Shocks that passed quickly, or in which the threat to the oil supply was decisively countered, often proved to be buying opportunities.

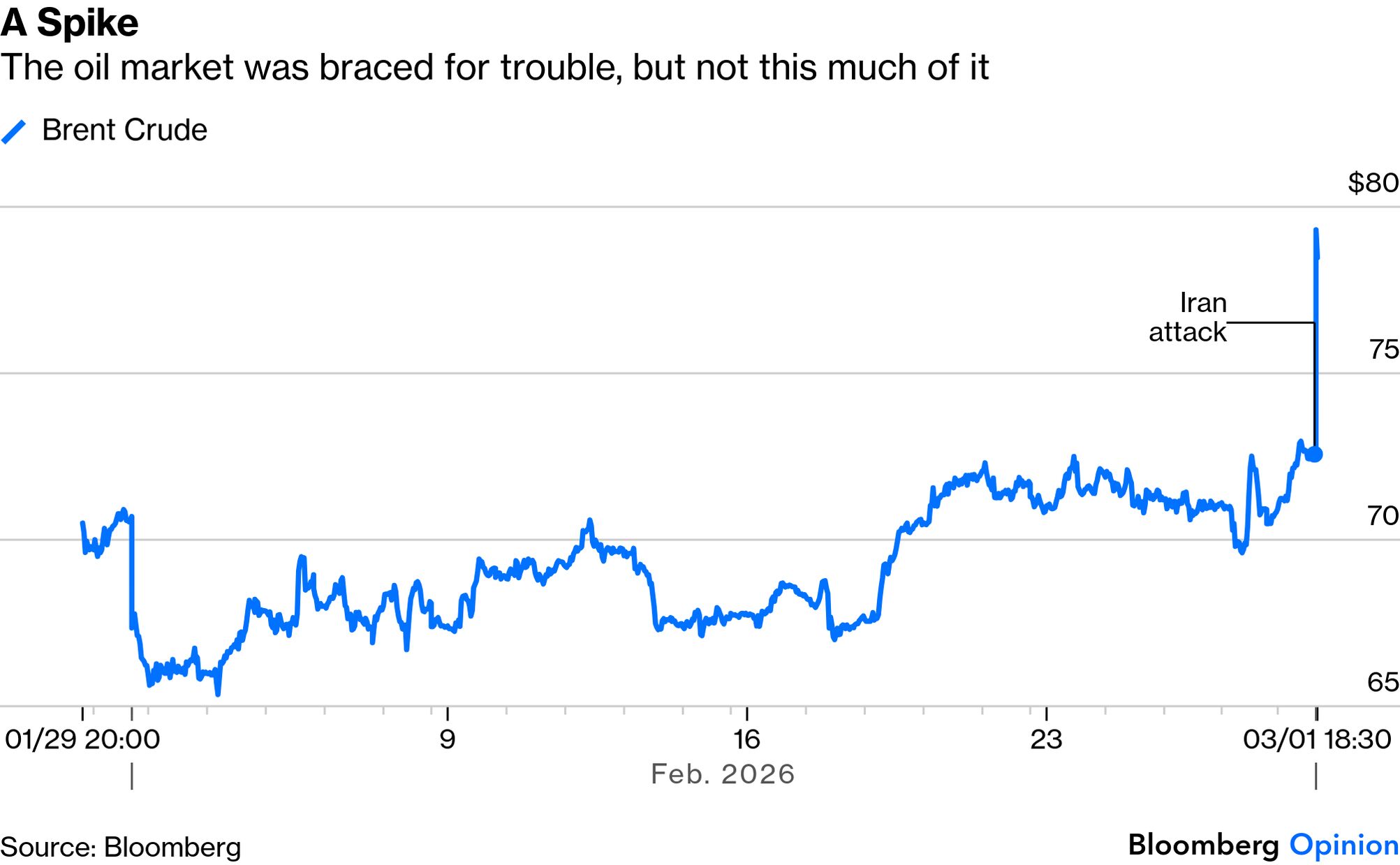

So as the oil markets reopen after an extraordinary weekend with a massive spike (Brent crude leapt 12.5% before stabilizing), it’s best to focus on what always matters most to markets in the short term after a geopolitical incident. Will it affect the supply of oil? Javier Blas argues in Bloomberg Opinion that the Iran strikes will be nasty for oil prices but won’t constitute a full-blown shock.

What’s different about this incident compared to other recent conflagrations is that there has been retaliation, which has hampered other countries in the region and cost American lives. The longer an outright shooting war continues, and the further it spreads, the greater risk that this becomes a major shock that brings down a range of markets.

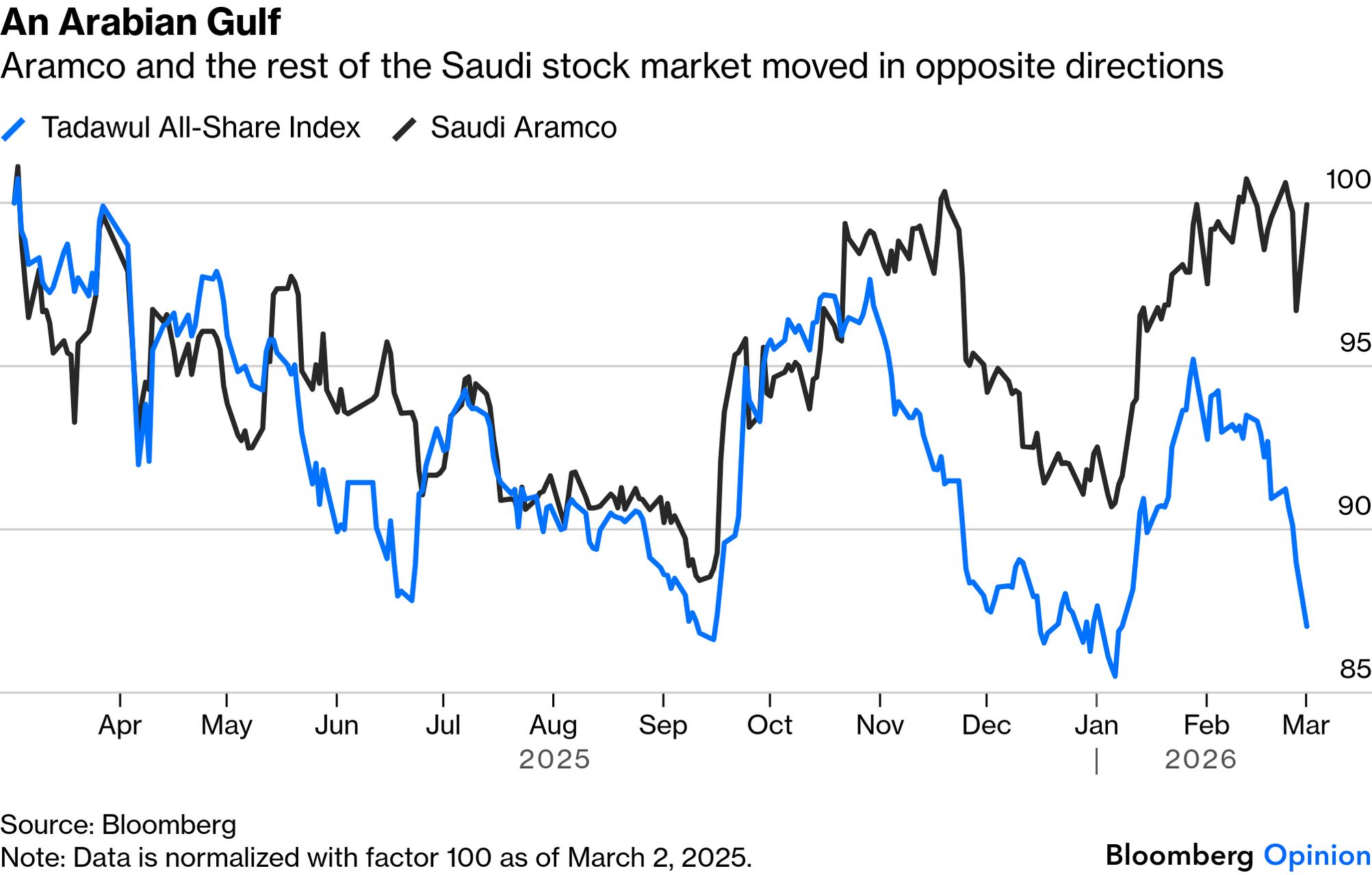

The immediate response in Saudi Arabia, which traded on Sunday, shows that such risks should be taken seriously. Usually the fortunes of the oil producer Saudi Aramco, which accounts for 16% of the main Saudi equity benchmark, are inextricably linked to the overall market. Not this time. Aramco surged on the outlook for higher oil prices, but that didn’t stop the overall index from plummeting:

The key issue is the Strait of Hormuz, through which about 20% of global oil exports are transported. If Iran wants to close them, it can — at great financial cost to itself and to other Gulf countries. There are already reports of attacks on ships. Hubert Marleau of Palos puts the prospects for the oil price as follows:

A true Hormuz disruption would constitute a tail scenario, which could easily increase the price of Brent to $125 a barrel, whereas a quick regime change would oppositely restore normalcy and bring oil prices back to $60 a barrel. There is a third scenario, where the oil flows under threat not in an apocalyptic manner as OPEC+ increases oil production at an accelerating pace; but nonetheless in an escalating one, constraining supply and running the price to an $80 peak.

The third is arguably the likeliest. For now, the problem is that an interruption of some duration to oil supply, and therefore a hike in the price, is a given until there is greater clarity. Even though Iran has formally announced that it does not intend to close the strait, the impact on the flow of oil from the region is still significant, as the emerging markets investment group Gramercy explains:

Commercial shipping has largely paused regardless, as insurance underwriters withdrew war-risk coverage within hours of the initial strikes. Our assessment is that the binding constraint on oil flows is currently the insurance market, not a military blockade

On this basis, the immediate surge above $80 for Brent seems to make sense, and there is also no need for the price to move much further without material new developments. For the immediate future, markets will try to adjust the risk premium on equities — it should be higher, but it’s not at all clear how much. They will also look for winners and losers from the conflict, much the exercise that they’ve been carrying out for AI of late. There could be some strange collateral beneficiaries, including the UK. Citi equity strategist Beata Manthey pointed out: “The UK market is tilted heavily towards commodities and defensive sectors along with a sizable share of aerospace & defense, and thus serves as an effective ‘geopolitical hedge’ within equity portfolios.”