JPMorgan mener, at al erfaring med geostrategiske kriser viser, at det betaler sig for investorer at diversificere og at holde sig til kvalitetsaktier med høj indtjening. Der bør også skabes en bedre balance mellem value- og vækstaktier, mener banken. Men banken går ikke ind for en egentlig omlægning af porteføljerne og advarer investorerne mod at lægge alt for megen vægt på aktuelle prisstigninger på energi og fødevarer, da de ikke spiller så stor en rolle for økonomien og købekraften som tidligere. Dog advarer JPMorgan mod europæiske aktier i forbindelse med Ukraine-krigen. Analysen er lavet den 28. februar.

Thought of the week

Following Russia’s invasion into Ukraine, markets saw a sharp sell-off in risk assets, while safe-haven assets (i.e. Treasuries, USD and gold) outperformed. Russia-linked commodities popped with European natural gas +60% and Brent prices crossing $100/barrel. However, by the end of Thursday, markets largely reversed their course with only minimal moves to the 10Y (-1bps) and WTI (+$1).

Looking ahead, markets will be sensitive to sanctions and Russia’s counter response to them. This is a balancing act as the West wants to punish Russia, but not at the expense of other economies. It is further complicated by the fact that Russia is the 2nd largest producer of oil and natural gas and a major commodities supplier (i.e. fertilizer, wheat, aluminum). As of Friday, sanctions have involved Russian oligarchs, new Russian sovereign debt, Russia banks and Nord Stream 2. But, they have not yet involved Russia’s use of SWIFT or Russian oil and gas.“

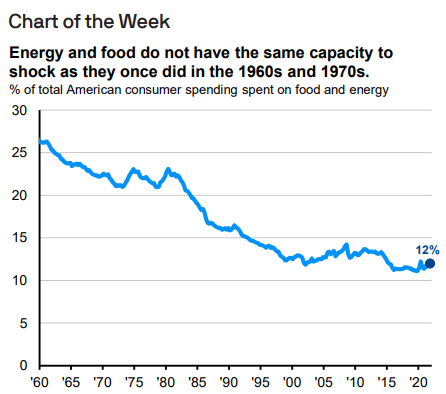

While we might see price pressure on energy and food in the near term, they do not have the same capacity to shock as they once did. As illustrated in the chart, energy and food spending now represents much less of Americans’ overall wallet share – 12% of total spending vs. an average of 23% throughout the 60s/70s. Furthermore, America has a greater degree of energy independence and the luxury of natural resources that Europe does not, which should also soften the blow.

In terms of investment implications, remember that staying invested in a diversified, goals-aligned portfolio has paid off through countless geopolitical crises and should continue to do so. Ultimately, portfolios should benefit from quality stocks with durable profits and fixed income for portfolio ballast. We are not advocating for broad rebalancing at this time, but rather are seeking balance between value vs. growth and U.S. vs. international. Diversification will remain key as we ride out volatility.