Analytikerne hos JPMorgan ser bekymret på den kommende udvikling. De meget høje værdiansættelser på nogle selskaber er virkelig kommet under pres. Mange selskaber er værdiansat alt for højt. Derfor mener JPMorgan, at investorerne skal satse på moderat værdiansatte selskaber, som er solide og pålidelige. Feltet for aktionærerne snævrer sig altså ind. Men der er også nogle muligheder. Europæiske aktier er ikke så højt værdiansatte som amerikanske, og kinesiske aktier er blevet mere attraktive efter et fald på 50 pct. Analytikerne venter, at der stadig skal være et fald i værdiansættelserne, og der skal skabes tillid til udviklingen, før der kan ventes generelle kursstigninger.

Global Equity Views 2Q 2022

In Brief

- Despite recent weakness in global markets, many of our portfolio managers remain rather cautious about the outlook. Economic growth is slowing, inflation looks stubbornly high, and interest rates are on the rise in most regions.

- The very high valuations awarded to innovative companies with rosy growth forecasts have come under severe pressure this year. But the gap between high and low priced equity valuations is still wide, and the fundamental outlook for some of the high priced cohort is not as good as was once believed.

- Although great opportunities will doubtless emerge, most of our managers are cautious about adding to beaten-down growth stocks, and we are also wary of the risks for disappointments from companies more exposed to the economic cycle. Quality and predictability, as well as modest valuations, matter most in this more difficult environment.

Taking stock

The rough start to the year for global equity markets has continued into the second quarter. At the time of writing, the MSCI All Country World Index was down 17%, with losses in all regions and most industries. Despite lower prices, our equity investors remain somewhat cautious for the most part, with most expecting average or below-average returns from markets over the next couple of years. The economic backdrop looks tricky, with the extraordinary boom conditions created by the aggressive fiscal and monetary response to the pandemic now fading. Growth is slowing, inflation remains stubbornly high, and central banks are raising interest rates far more quickly than was expected just a few months ago.

The boom in the real economy was mirrored in a stock market boom that created some dangerously high valuations. The S&P 500 multiple peaked at 24x forward earnings last year, a level not seen since the late 1990s. The prices of faster-growing, innovative companies moved decisively into bubble territory. As equity prices fall and valuations drop, these excesses are corrected. Although the overall U.S. equity market now sells at a much more reasonable 17x earnings, this is still not a low valuation, especially if profits disappoint as growth cools, which they may well do. Internationally, valuations look more reasonable, but across global markets we need to watch out for falling earnings expectations and remaining pockets of high valuations.

Every crisis brings opportunities. For the most part, our investors continue to be cautious on the winners of the past decade (see below). In our portfolio construction, we emphasize higher quality companies, focusing on high returns on equity and strong balance sheets.

But we also spot some interesting opportunities emerging. Chinese equities, for example, are heavily out of favor, facing a very difficult economic environment and aggressive government policy toward many of the most successful companies. But the Chinese stock market has fallen 50% from last year’s peak and now trades at an attractive valuation. The near-term outlook looks especially tough as the government grapples with COVID-19 outbreaks that are exacerbating weakness in the economy. But for long-term investors, these valuations look interesting.

High growth companies: Are we there yet?

Much of our discussion at recent equity quarterly meetings focused on the market’s fervor for innovative, fast-growing companies powered by technology and threatening to disrupt many different industries. This enthusiasm peaked last year, and sentiment has soured very quickly in recent weeks. The Nasdaq market, for example, has lost nearly USD 6 trillion in market capitalization from its peak, a 24% decline (that compares with a 65% decline in the 1999-2000 period). A third of the stocks now listed on Nasdaq have plunged 75% or more from their highs. The group of “not yet profitable” companies that we monitor worldwide has now underperformed by 51% since the end of 2020, after 81% relative gains in the previous two years.

Do these dramatic declines correct the earlier excesses? Many of our portfolio managers think that to get much more positive, we need to see both lower valuations and more time for the market to adjust expectations. In our quantitative work, the gap in valuations between high and low priced growth stocks remains almost as wide as at last year’s peak. That is mostly because the near-term profit outlook for many low priced stocks (especially in energy) has improved even faster than the stocks have appreciated.

While key secular trends, such as the move to cloud computing, are intact, we have also seen some notable disappointments among the high priced cohort of the market. Clearly, some of the strength in profits for growth companies last year was a temporary event, reflecting pandemic-driven changes in consumer behavior that are now fading as most of the world economy reopens.

We are also watching carefully for signs that the tremendous investments made in all things innovative may disrupt the disrupters as well. In short, we’re cautious. Our growth investors find more opportunities in industrial and financial companies than in the technology sectors that were at the heart of market enthusiasm in recent years.

European profits: Better than feared?

Many market commentators thought that 2022 would finally be the year in which European equity markets provided strong relative returns after so many years of lagging behind. But the outbreak of war in Ukraine seemed to dash those hopes, as energy prices soared (a price shock that matches those seen in the 1970s) and threatened to push the region’s economy into recession. Our research team has carefully reassessed the near-term outlook for profits, and its analysis does provide some grounds for optimism.

For three main reasons, we still expect modest profit growth for European companies this year. First, European consumers look well positioned to weather the storm, with an estimated USD 1 trillion in additional savings accumulated during COVID-19 lockdowns. Second, as the pandemic fades, European economies will enjoy the benefits of reopening this year. And finally, the companies represented in European stock market indices are globally diversified, with only 40% or so of their revenues sourced from Europe itself.

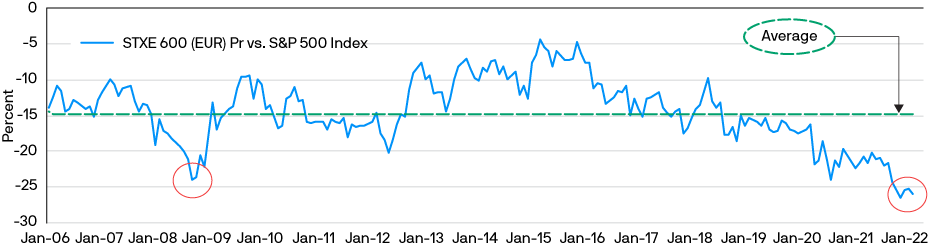

We think our profit estimates for 2022 still look reasonable. Of course, the region’s important energy sector will lead the gains, but we find reasons for optimism across many industries. With valuations below long-term averages, European equities may still offer a positive surprise this year (Exhibit 1).

In Europe, valuations look attractive compared with the U.S.

Exhibit 1: 12-month forward P/E discount of Europe vs. U.S.

Source: Bloomberg. LHS series rebased to 100 as of December 31, 1999 to April 4, 2022. Index in EUR and includes reinvested dividends. Indices do not include fees or operating expenses and are not available for actual investment.

Using data analysis to help our investment decisions

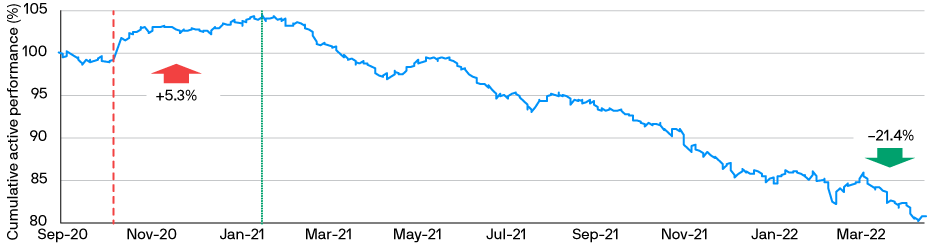

We have heard a great deal in recent years about the potential of new data sources to better inform investment decisions, and we’ve incorporated many of these into both our fundamental and our quantitative analysis. But we find it even more interesting to use new data analytical techniques for a fresh look at traditional data sets. For example, our equity failure model is designed to highlight the stocks at greatest risk of proving to be very poor investments (Exhibit 2). To measure the risk of failure, our team considers a range of both fundamental business factors and more market-based metrics, such as short interest and stock price volatility. The model has delivered good results: The bottom quintile of the failure model has underperformed global markets by almost 6% this year, after 15% underperformance in 2021. Clearly, these are names well worth avoiding.

Unattractive stocks highlighted in our equity failure model have performed poorly this year

Exhibit 2: Performances of stocks in the bottom quintile of our equity failure model, Sept. 2020–Apr. 2022