JPMorgan har analyseret PMI-tallene fra april i de store industrilande og konkluderer, at de peger på en robust genopblomstring af økonomien. Det vil især hjælpe de sektorer, som har været hårdt ramt, f.eks. flysektoren, som ventes at få et brake-even til sommer, samt banksektoren. Det bekræfter JPMorgan i, at det blive cykliske aktier, herunder value og internationale aktier, der får fremgang.

Thought of the week

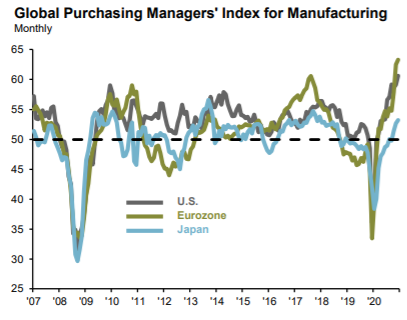

Last week provided a first look at the April PMI data for the major developed market economies. Manufacturing and services PMIs came in at 63.3 and 50.3, respectively, for the euro area and 53.3 and 48.3, respectively, for Japan.

While manufacturing activity continues to look robust, the continued recovery in services on the back of vaccination efforts and the gradual lifting of social distancing measures should lead to accelerating growth over the remainder of the year.

Although Japan’s services PMI came in below 50 at 48.3, household spending on services continued to improve on a year-over-year basis, indicating that services is indeed on the road to recovery.

Similar to Europe and Japan, U.S. April flash PMI data came in above 50, with manufacturing and services PMIs rising relative to the prior month.

Unsurprisingly, this improvement in economic data has coincided with solid earnings results, particularly among the industries hit hardest by the pandemic like financials and airlines.

Looking ahead, a steeper yield curve and improving credit metrics have eased some pressure on bank margins, and while the airlines are still posting net losses, increased mobility has led most airlines to project they will begin to break even by the summer.

Broadly, an environment of accelerating economic growth and rising rates should support the more cyclical parts of the market, and reinforces our constructive view on both value and international equities.