Referat af morgenkommentar fra FTs Authers bearbejdet til dansk:

Kommentaren behandler hvordan krig og blokeringer i Den Persiske Golf kan udvikle sig til en global fødevarekrise.

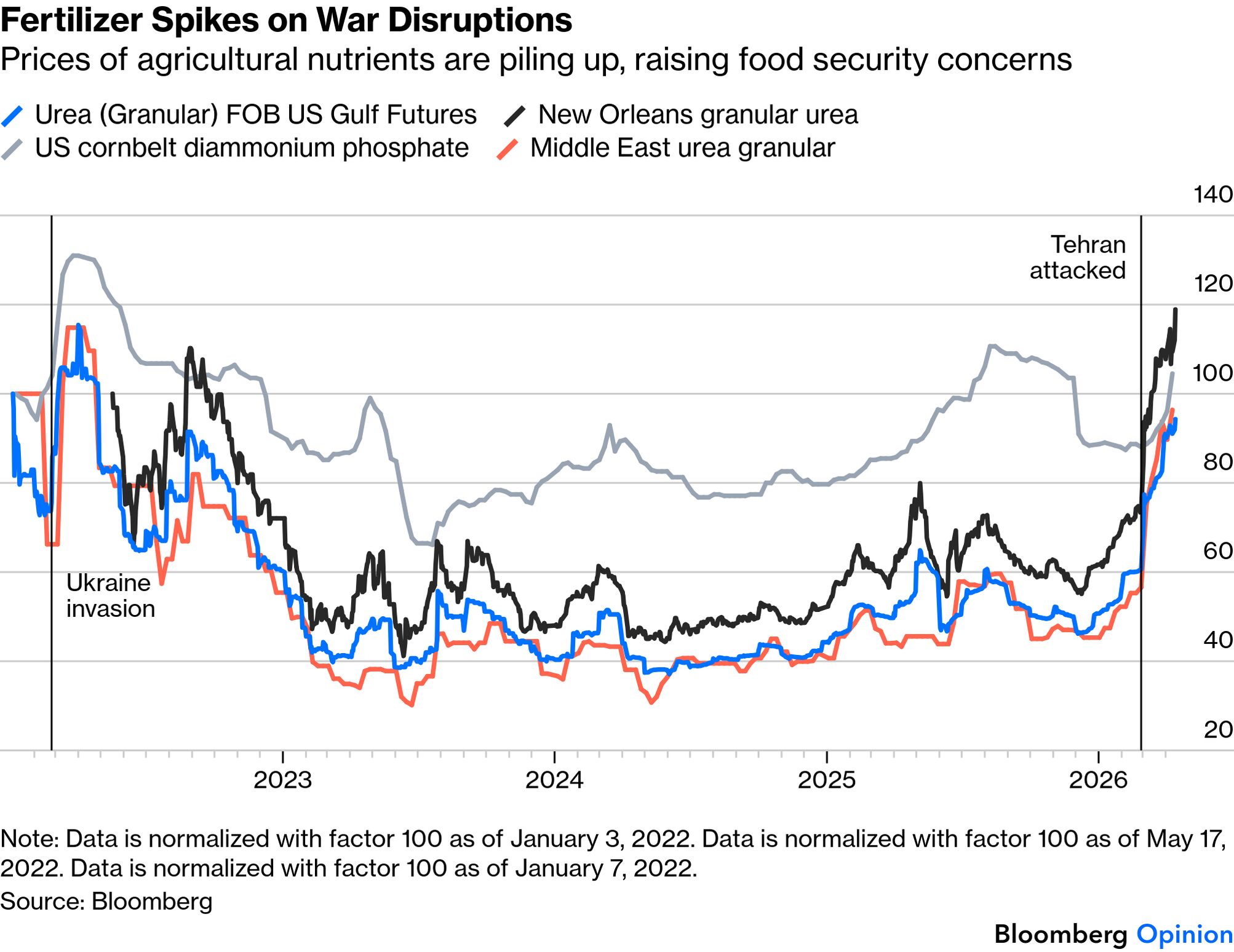

Hovedpointen er, at selv om olie naturligt fylder meget i debatten om krigens økonomiske konsekvenser, er fødevarer i virkeligheden det mest præcise mål for, hvor dybt forstyrrelserne stikker. Teksten fremhæver, at gødning fra Golfregionen udgør mindst 30 procent af den globale forsyning, og at en blokade af Hormuz strædet derfor ikke blot rammer energimarkederne her og nu, men også landbruget med en forsinkelse. Konsekvensen vil især blive synlig ved høsttid, fordi gødning er et nødvendigt input i dyrkningen, og fordi prisstigninger eller manglende tilgængelighed først slår fuldt igennem senere i produktionskæden.

Konflikten har allerede sendt priserne på gødning markant op. Golfstaterne er over de seneste tre år blevet de største regionale eksportører af ammoniak samt næststørste eksportører af diammoniumfosfat. Samtidig er flydende naturgas en vigtig forudsætning for gødningsproduktion i lande som Indien, Pakistan, Bangladesh og Tyrkiet. Dermed bliver virkningen global og ikke kun regional. Teksten understreger, at højere gødningspriser næsten uundgåeligt vil føre til højere fødevarepriser, men med tidsmæssig forsinkelse. I et længerevarende krigsforløb beskrives stigende fødevarepriser paradoksalt nok som det mindst dårlige udfald, fordi alternativet er, at landmænd springer gødningssæsoner over, hvilket kan føre til lavere udbytter, endnu højere priser senere og en bredere trussel mod global fødevaresikkerhed.

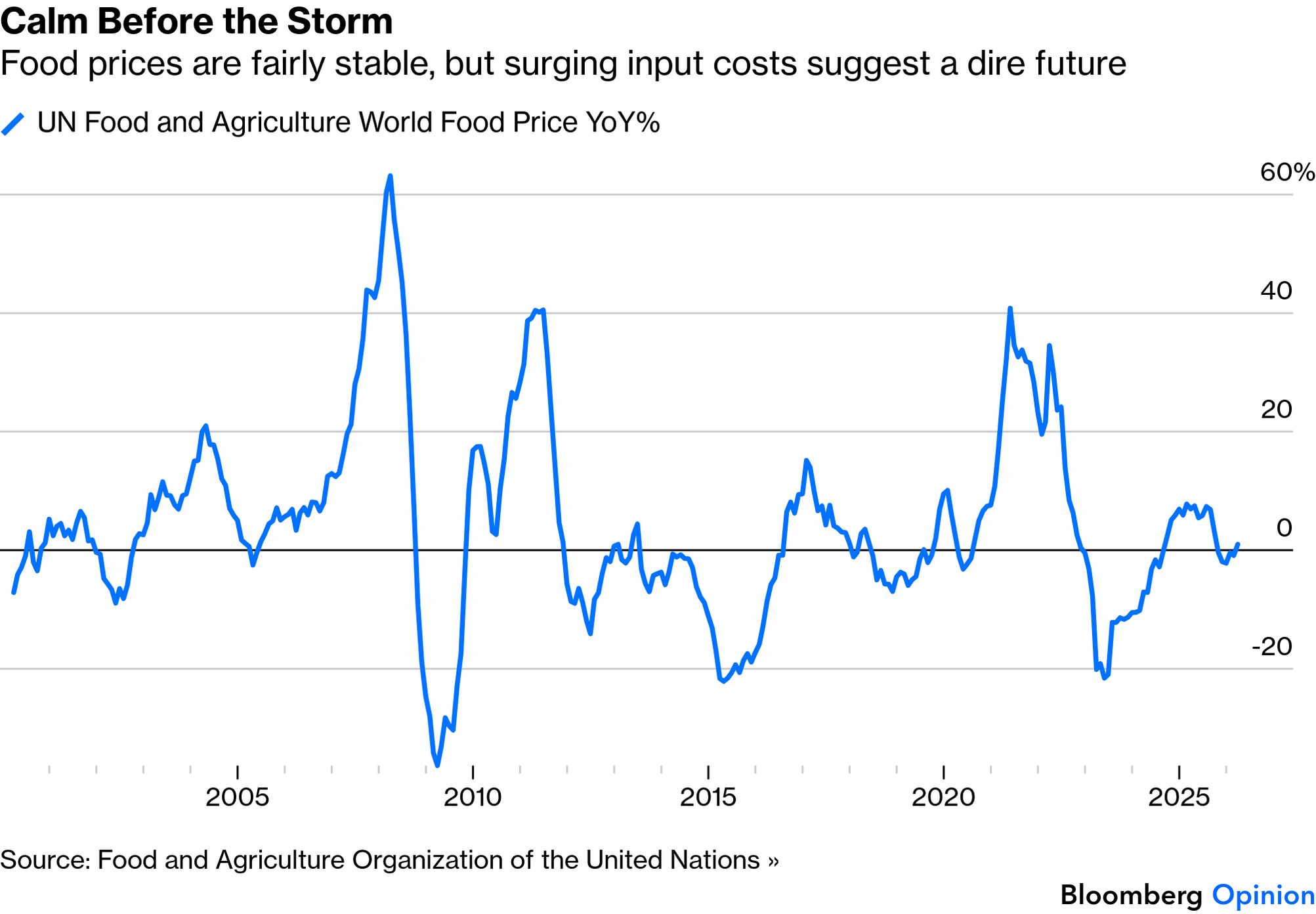

Authers spørger derefter, om disse bekymringer er berettigede, og svarer ja ved at pege på erfaringerne fra Ruslands invasion af Ukraine og lukningen af Sortehavet. Her bruges den tidligere fødevarekrise som eksempel på, hvor følsom den globale fødevareforsyning er over for geopolitiske chok. Selvom den makroøkonomiske baggrund i dag beskrives som sundere end under Ukraine-krisen, er typen af forstyrrelse ifølge teksten ubehageligt velkendt, og de politiske følger af stigende fødevarepriser ligger stadig frisk i erindringen.

Teksten flytter herefter fokus til amerikansk landbrug og de indenlandske konsekvenser af høje inputpriser. Det amerikanske justitsministerium undersøger høje priser på gødning, maskiner og andre landbrugsinput. Samtidig viser en undersøgelse fra Farm Bureau, at over 70 procent af landmændene ikke har råd til al den gødning, de har brug for. Der citeres også en aktør fra branchen for, at nogle inputpriser er fordoblet siden pandemien, hvilket har presset nogle landmænd ud af markedet og efterladt andre i en situation, hvor de kun lige akkurat løber rundt.

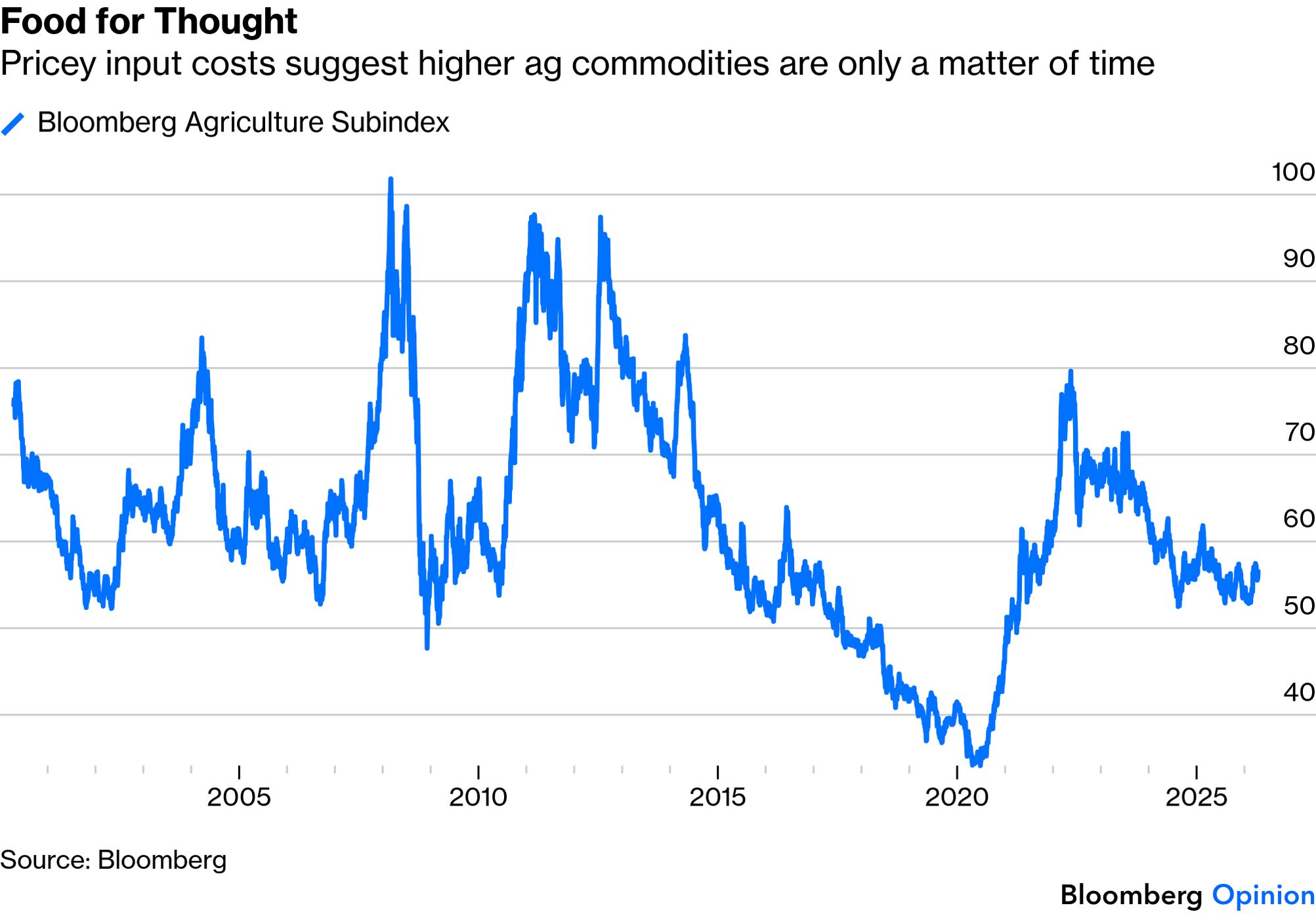

Midlertidig offentlig støtte beskrives som utilstrækkelig; i stedet argumenteres der for, at USA bør investere mere målrettet i teknologisk infrastruktur, så landbruget bliver mere selvforsynende og økonomisk effektivt. Selv om Bloomberg Agricultural Commodities Index antyder, at priserne indtil videre er forholdsvis afdæmpede sammenlignet med Ukraine-forstyrrelserne, advarer teksten om, at de højere inputomkostninger endnu ikke for alvor er slået igennem i forbrugerpriserne. Derfor kræves der efter forfatterens vurdering ikke blot våbenhvile og genåbning af Hormuzstrædet, men også bredere politisk handling for at holde fødevarer økonomisk tilgængelige.

Tre hovedkonklusioner

1. Krigens alvorligste økonomiske følge kan vise sig at være fødevarer snarere end olie.

Teksten argumenterer for, at olie fylder debatten, men at gødning og dermed fødevareproduktion er den dybere og mere langsigtede sårbarhed. Fordi Golfregionen spiller en central rolle i den globale gødningsforsyning, kan en blokade af Hormuzstrædet få forsinkede, men alvorlige konsekvenser for høstudbytter, fødevarepriser og global fødevaresikkerhed.

2. Høje landbrugsinput presser allerede landmændene, og problemet kan vokse, før det ses fuldt ud hos forbrugerne.

Teksten viser, at stigende priser på gødning og andre input allerede rammer landmænd hårdt, og at mange ikke har råd til nødvendige indkøb. Derfor er den aktuelle relative ro i råvareindeks ikke nødvendigvis betryggende, fordi effekten på fødevarepriserne først forventes at slå igennem senere. Midlertidig støtte vurderes ikke at være nok; der efterlyses mere strukturelle løsninger.———-

Originaltekst:

Oil dominates the affordability debate for good reason, but as Points of Return discussed here, the truest measure of the war’s disruption is food. Fertilizer from the Persian Gulf region accounts for at least 30% of global supply. The effect of the Strait of Hormuz blockade will only be visible months from now, at harvest time.

The conflict has already driven fertilizer prices to astronomical levels. Over the past three years, Gulf countries have emerged as the largest regional exporters of urea and ammonia, both nitrogen-based fertilizers, and the second-largest exporters of diammonium phosphate. Liquefied natural gas is a key input for fertilizer production in countries with limited domestic gas, like India, Pakistan, Bangladesh and Turkey.

This will impact food prices, but with a lag. Yet given the tight link between fertilizer costs and food inflation, it’s only a matter of time before the effects become visible, perhaps long after the conflict. In a long war, ironically, the best-case outcome may be higher food prices. The alternative would be missed fertilizer-application seasons leading to lower crop yields, and thus even higher prices down the road, plus a broader threat to global food security.

Are these fears warranted? The disruption after Russia’s invasion of Ukraine, another major agricultural hub, and the subsequent closure of the Black Sea offer ample evidence of what could happen. The UN Food and Agriculture Food Prices index shows just how sensitive food security is to geopolitical events:

Pandemic restrictions were only beginning to ease when Ukraine was invaded, while wider inflationary pressures were driving up prices. These exacerbated the effect on food prices. Today’s macro backdrop is healthier, but the nature of the disruption is uncomfortably familiar — and the memories of its political consequences are fresh:

Now, the US Justice Department is probing high costs for fertilizer, machinery, and other farm inputs. Deputy Agriculture Secretary Stephen Vaden has met with Justice and Federal Trade Commission officials to discuss lines of inquiry, and knows that “farmers have a lot of information that might be relevant to these investigations.”

Whether due to profiteering or supply chain stresses, a Farm Bureau survey shows that more than 70% of farmers cannot afford all the fertilizer they need. Arthur Erickson of Hylio, who works closely with farmers, points out that some input costs have doubled since the pandemic. That has driven some farmers out of business, and those who remain are barely breaking even. Resources from the Agriculture Department will likely provide only temporary relief:

I think that’s a Band-Aid. And in fact, that could come back to bite us even harder, just simply due to inflation and the negative effects of that. The US government needs to take a much more focused approach to building out the country’s technological infrastructure, which will allow us to be more self-sustaining and economically efficient in our farming.

Meanwhile, the Bloomberg Agricultural Commodities Index suggest prices remained fairly contained relative to the Ukraine-related disruptions:

That’s reassuring, but higher input costs will take time to seep into food prices. Limiting that pass-through will require decisive action. Pausing hostilities and reopening the Strait is necessary but only a starting point. Beyond that, more needs to be done to ensure that food on the table isn’t prohibitively expensive.

—Richard Abbey

Meanwhile, Back at the Fed… |

This is getting tiresome. There is no longer a prospect of wholesale change in the Federal Reserve’s leadership in a Trumpian direction, as the regional governors have been reconfirmed in their posts for another five years. It should be time put the issue of Fed independence on the back burner.

But we can’t. Justice Department officials have made an unannounced visit to the Fed in pursuit of their flailing probe against Chairman Jerome Powell over building renovation overruns, and also fighting in court — despite a ruling that the case was spurious — for the right to continue it. Until the legal proceedings end, Republican Senator Thom Tillis has promised to block Kevin Warsh’s nomination to succeed Powell when his term ends May 15. Powell has said he’ll stay as chairman if Warsh isn’t confirmed on time, and won’t resign from his remaining two years on the governing board until the prosecution ends. Trump says he’ll fire Powell as chairman if he tries to stay — and a Justice memo from 1979 suggests he has the right to do so.

This hideous mess is not over. But it hasn’t stopped a stock market rally that’s beginning to look historic. Why?

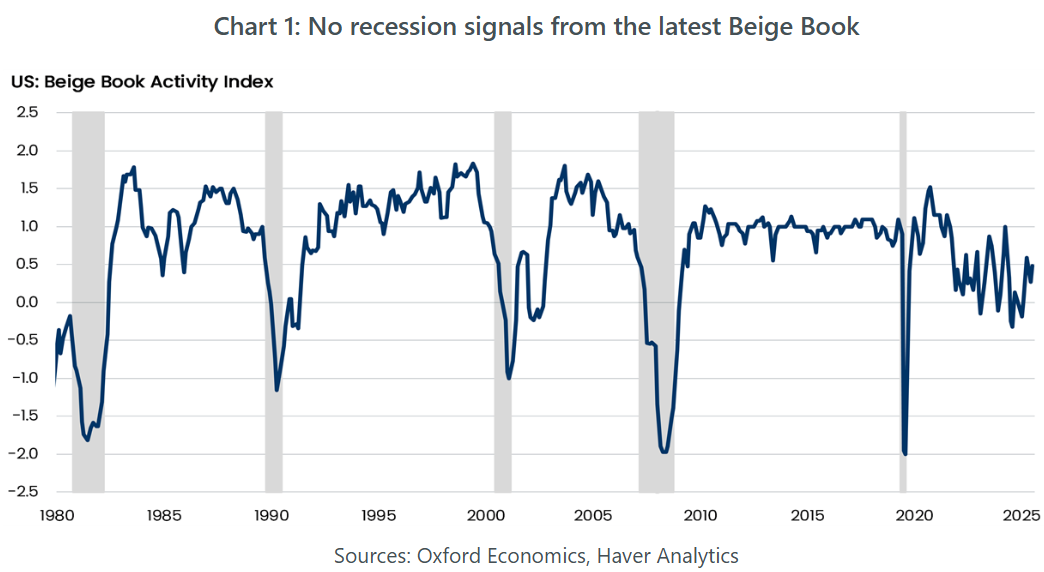

There are two main reasons. First, the war has made the Fed’s finer judgments irrelevant for now. They won’t be moving rates until there’s clarity on the extent of the price shock. Interestingly, even Treasury Secretary Scott Bessent appears to accept this, while the latest Beige Book collection of anecdotal evidence produced by the Fed’s regional branches suggests an economy in suspense with no call to move rates. This index was produced by Oxford Economics:

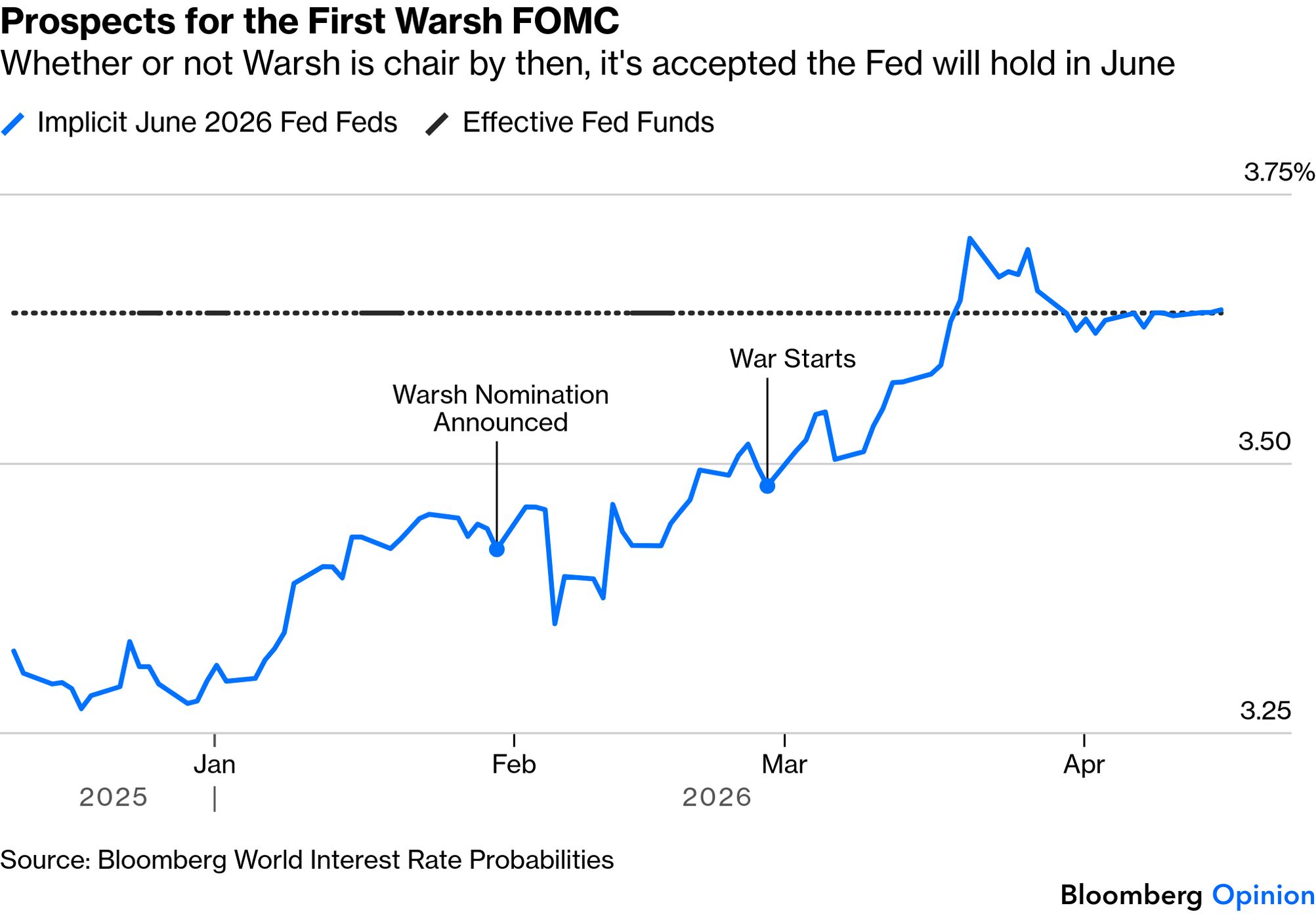

Whether or not Warsh chairs the Federal Open Market Committee meeting in June, the almost universal expectation now is that rates won’t change, and that the White House won’t press hard for a cut:

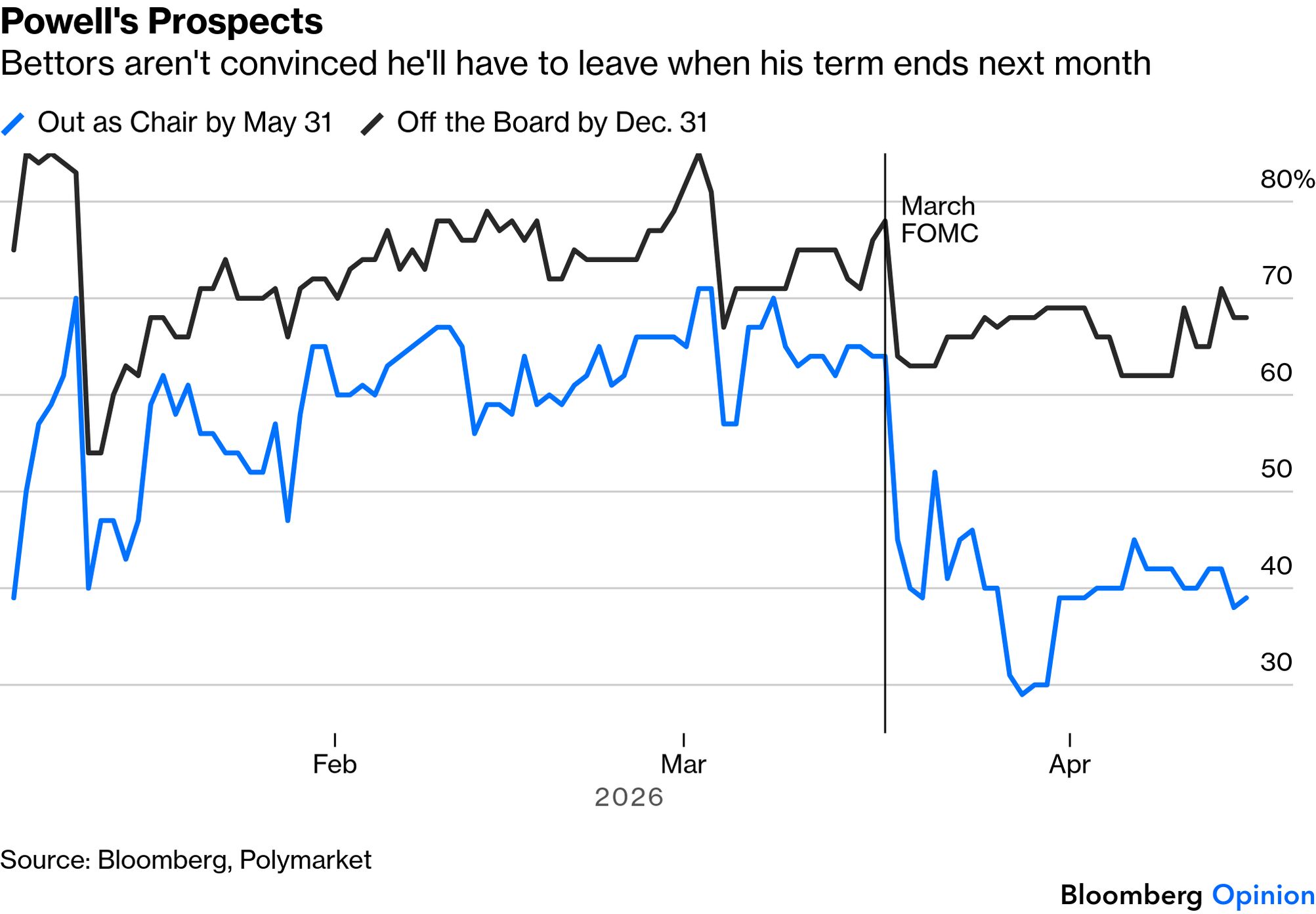

Second, there’s an ongoing belief that even through the Justice Department has to try to satisfy the president’s desire for revenge, these attempts aren’t going anywhere. Powell is expected to leave as a governor by year-end. Polymarket bettors still put a 60% chance on his hanging around for a while until the end of next month, but that’s more an expression of the belief that the Senate won’t have confirmed Warsh by then:

The president might just go through with his threat to fire Powell in May under these circumstances, and elevate a temporary chairman — possibly the ultra-dovish governor Stephen Miran. It could create a mess. For that reason, markets are working on the assumption that Trump won’t do it.

The situation is unnecessary and undignified. The chances remain that it won’t cause too much damage.