Uddrag fra FTs Authers

What If Markets Declare Victory? |

There has always been a risk that President Donald Trump would declare victory in the Middle East conflict prematurely. That’s what he does; it seems to have worked for him in the fracas over Greenland, and he usually gets away with it.

In the latest blindside from the White House, released before Wall Street opened on Monday, attacks on Iranian energy sites have been put back by five days because of “very good and productive conversations regarding a complete and total resolution of our hostilities in the Middle East.” Here is that Truth in full:

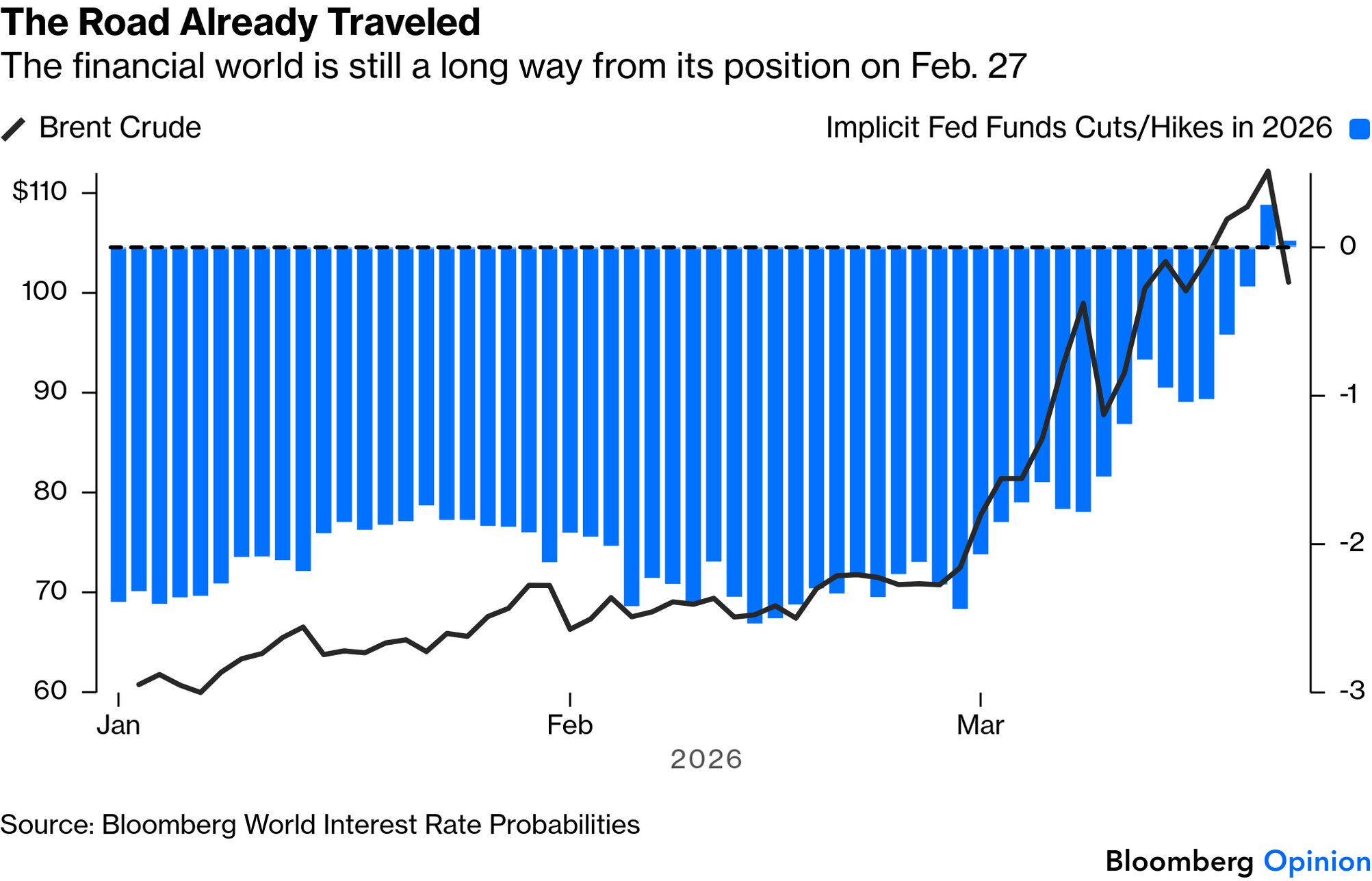

This followed Truth Social posts on Friday and Saturday nights, US time, which first declared that military operations would be wound down (even if the Strait of Hormuz stayed closed), and then made a 48-hour ultimatum it would launch an attack on Iranian energy facilities. The combined effect of those three utterances — followed by Iran’s denials of any talks — sparked a massive rally at Monday’s open, which fizzled to leave the Nasdaq 100 more or less exactly where it had started Friday morning:

After such wildly inconsistent pronouncements, it’s tempting to ignore the president, but that would be unwise. As Tina Fordham of Fordham Global Foresight puts it, relief is “clearly justified:”

The threatened attacks on energy infrastructure would have had potentially catastrophic consequences on the future outlook for regional oil production (a threat to all parties), while strikes on power plants risk Iran becoming a failed state of 92 million desperate, thirsty people.

It’s also now clear that the president wants to end the war and avoid major escalation. To quote Marko Papic of BCA Research: “The reality is that he’s reached his constraints and he’s becoming aware of them. That’s a positive, and the market is reacting appropriately.”

Markets are rightly skeptical that Trump can declare victory and walk away against a motivated opponent that maintains control over the Strait as leverage. But the prices that set the guidelines for the financial world did move — very significantly. Brent crude dropped back below $100, while fears that central banks will respond with rate hikes abated:

Oil prices and central bank projections can be self-reinforcing. They can also collude with markets to decide that a continuing conflict doesn’t matter. Wars in sub-Saharan Africa cause great bloodshed but no financial losses for the Western world as they don’t affect energy supply or monetary policy; Israel’s conflicts of the last 50 years have had minimal market impact as they don’t directly threaten oil. And Papic points out that the Iran-Iraq war carried on from 1980 to 1988 with a million casualties and endangering exactly the strait of water that is at issue now without impeding a historic bull market in stocks.

This points to a new risk. Markets — not the US or Iran — might declare that the war is over. That would hurt anyone still prudently guarding against the risk of further escalation, but it’s a real possibility.

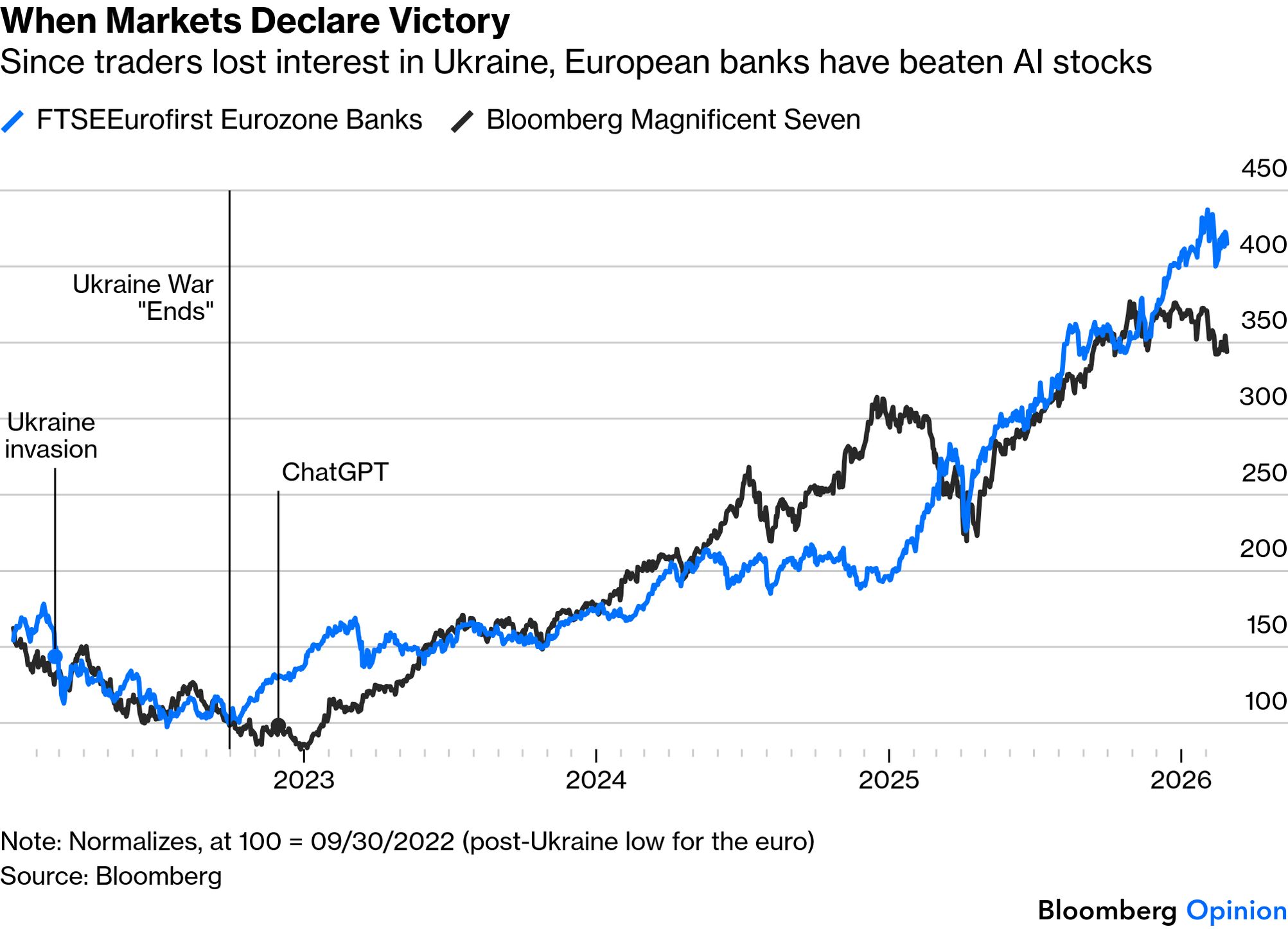

In Ukraine, the war continues to put the lives of young Ukrainians and Russians into a meat grinder to little obvious purpose. But since markets reassured themselves that it wouldn’t lead to nuclear conflict, and that Western Europe could find a way to survive without Russian natural gas — a point that came when the euro bottomed against the dollar on Sept. 30, 2022 — they’ve behaved as though the war is over.

Buying an index of euro-zone banks on that date would have beaten even the US Magnificent Seven tech platforms, which two months later would receive a massive boost from the launch of ChatGPT:

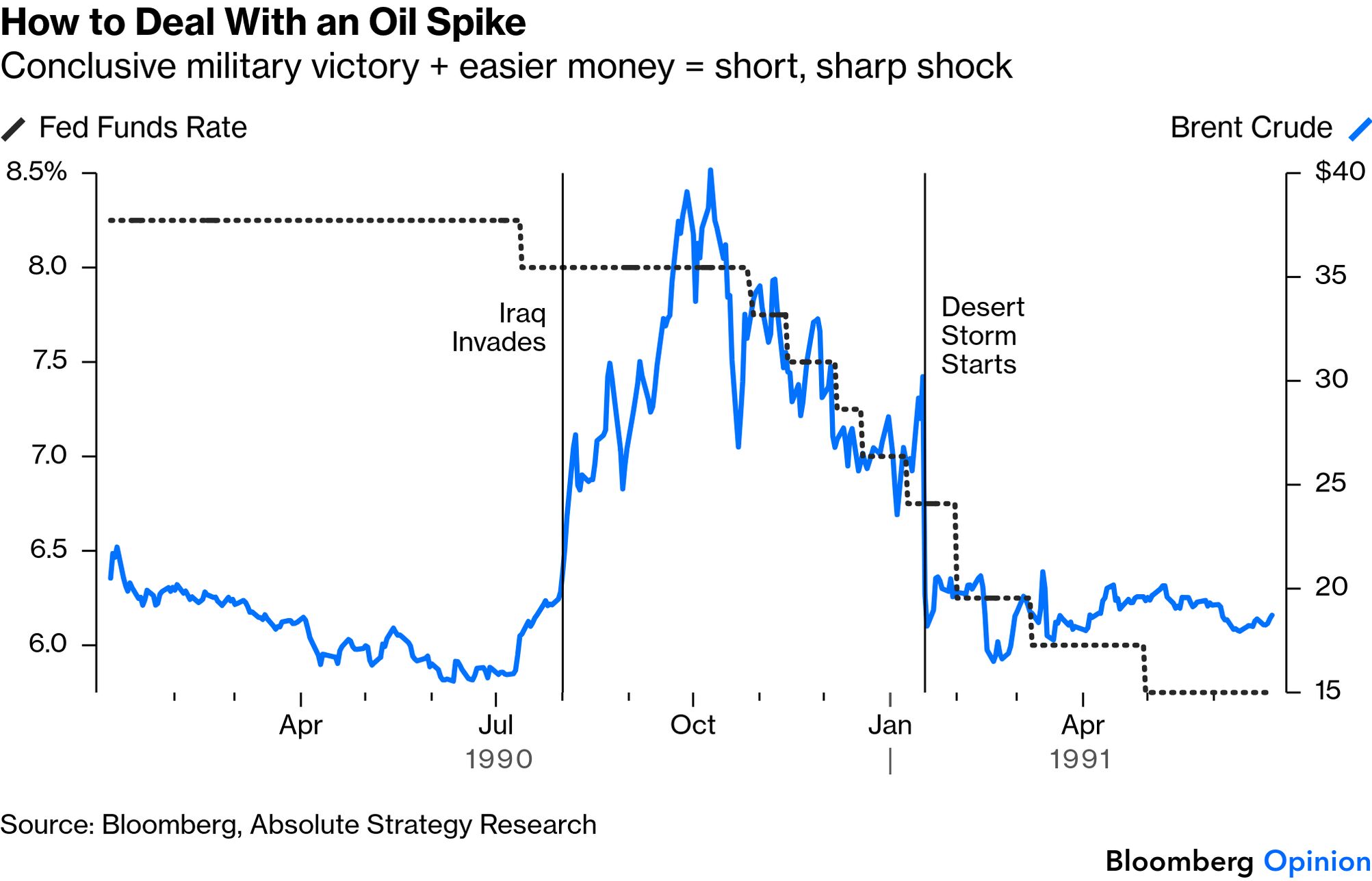

Look at the most comparable supply shock, when Iraq under Saddam Hussein invaded Kuwait in 1990, and the upside risks grow clearer. In hindsight, the administration of George HW Bush delivered a lesson in statecraft and strategy that successors should have heeded. But for markets the point is that oil peaked and plummeted three months before the start of Operation Desert Storm:

There are obvious differences. In 1990, the US followed the Powell Doctrine, established overwhelming superiority, won quickly, and resisted the temptation to enter Iraq. And the six months between the invasion and Iraq’s expulsion were punctuated by five rate cuts from the Federal Reserve. Easy money makes any shock easier for markets to stomach.

A recession had already started when Saddam invaded. That smoothed the way for the Fed, which — as now — had cut shortly before the outbreak of hostilities, to bring rates down further. But it waited until oil had peaked and began to decline before doing so. The US-led alliance’s superb military job was aided by a self-reinforcing declaration of victory by the markets. It could happen again.

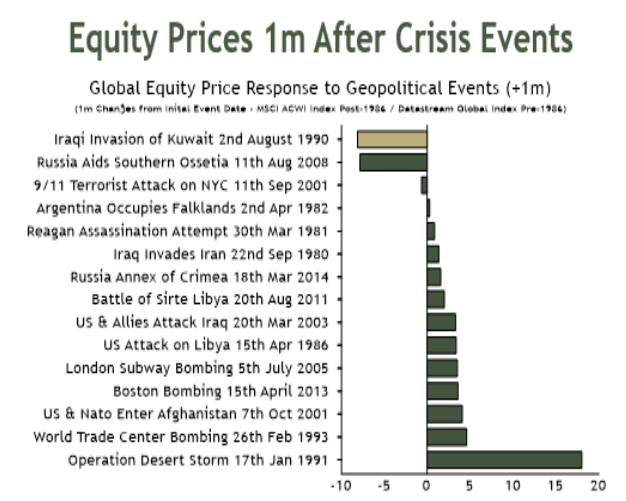

Generally with any geopolitical incident there comes a point where the worst is known. Investors want to buy ahead of that moment. Further, the initial reaction is often wrong. This ranking from Ian Harnett of Absolute Strategy shows the responses of world equities one month after the worst shocks that happened between 1980 and 2015:

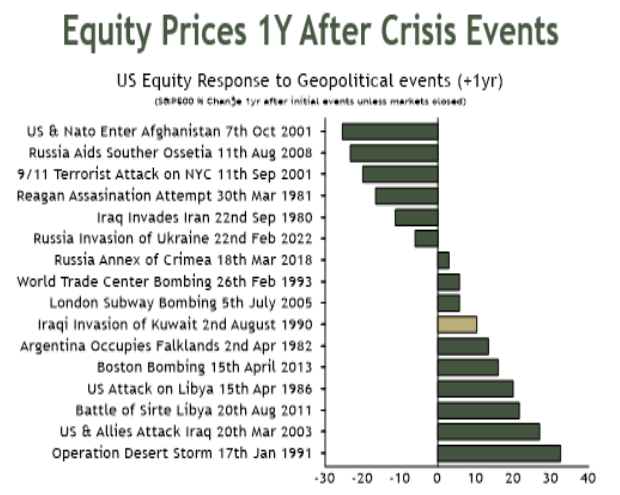

Here is the same list ranked according to returns 12 months later:

Shocks don’t happen in a vacuum. The selloff in late 2008 had far more to do with Lehman Brothers than with Russia’s incursion into Georgia. But several ugly events proved to be an opportunity to make great 12-month returns.

For now, risks are still high and markets won’t go up in a straight line, but traders are sensible to guard against upside risk. This is from Barclays Equity Tactical Strategies’ Alexander Altmann:

This narrative ultimately distills down to whether you think that both sides want an off ramp. If you believe both that the US are looking to dial down the temperature to salvage any form of political survival, and the IRGC want to still *have* a regime to control in the future (again, survival!), then diplomacy will prevail. Yes, ‘it takes two to taco’ … but that requires one party to initiative, and now both sides are dancing.

This logic is sound, but there is danger in any conflict situation. As Fordham points out, the Gulf countries are hardening in their position after suffering attacks in recent weeks, the US continues to send forces to the region, Trump is not declaring a ceasefire, and Iran has “potential escalation dominance” — it has greater military capability than thought, and can inflict extra pain much more easily and cheaply than its opponents. This isn’t over.

But upside risks are real and will probably continue to buoy share prices at least until the next terrifying presidential truth.