dansk resume af Authers morgenkommentar

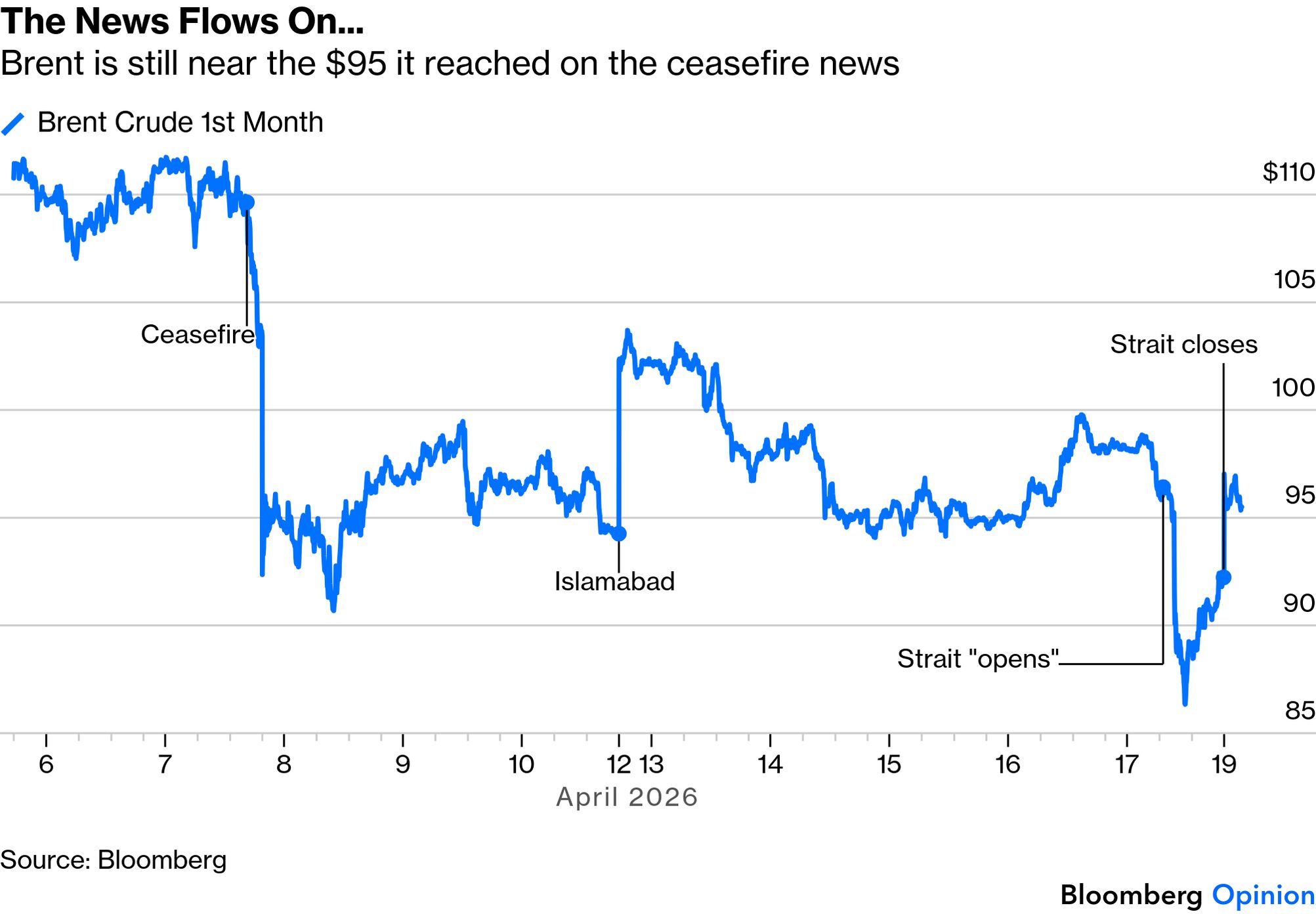

Authers beskriver et marked, der reagerer overraskende roligt og endda positivt på en meget usikker og farlig geopolitisk situation mellem Iran og USA. På overfladen kom der fredag meldinger om, at Hormuzstrædet var åbent, og at Iran ville aflevere sit nukleare materiale, men i weekenden viste det sig, at virkeligheden var langt mere kaotisk: iranske angreb på udenlandske skibe og amerikansk beslaglæggelse af et iransk fartøj skabte tvivl om våbenhvilen og udsigterne til nedtrapning.

Normalt burde så modstridende signaler og høj geopolitisk risiko føre til store markedsudsving, men i stedet har aktiemarkederne været præget af et usædvanligt kraftigt rally. Samtidig reagerer oliemarkedet mere i tråd med risikoen, fordi trafikken gennem Hormuzstrædet, som er afgørende for verdens olieflow, næsten er gået i stå. Effekten mærkes dog endnu ikke fuldt ud i verdensøkonomien, fordi oliefragt og lagre forsinker konsekvenserne.

Forfatteren fremhæver, at aktiemarkedets styrke virker mærkelig, især fordi økonomiske nøgletal har skuffet, og fordi usikkerheden omkring krigen fortsat er høj. Flere analytikere indrømmer, at de har svært ved at forklare kursstigningerne. En mulig forklaring er, at investorerne ser gennem den aktuelle uro og fokuserer på fremtidige rentenedsættelser, AI-drevet vækst og forventninger om stærkere virksomhedsindtjening senere på året.

Pointen er, at markedet tilsyneladende satser på en deeskalering og en hurtig normalisering. Men netop fordi investorerne er strømmet så massivt ind i markedet, er der også en betydelig risiko for et nyt fald, hvis antagelsen om nedtrapning viser sig at være forkert. Weekendens begivenheder kan derfor blive en vigtig test for, om rallyet kan holde.

Uddrag fra FTs Authers:

Who to believe? On Friday, while markets were still open, the Iranian leadership announced that the Strait of Hormuz was open, while the US declared that Iran was surrendering all its nuclear material. Over the weekend, we learned that these things weren’t strictly true. Foreign ships came under Iranian fire, and US forces seized an Iranian ship. This happened during a ceasefire still due to last until Wednesday.

Volatility like this, with two regimes who dislike and distrust each other showing no message discipline whatsoever, should be a recipe for turbulent and choppy markets. Instead, they’ve fostered what is now one of the most remarkable one-way rallies in history. Monday offers the next chance for all the scary news to have a financial impact. So far in Asian trading, equities are muted but oil has had a big reaction:

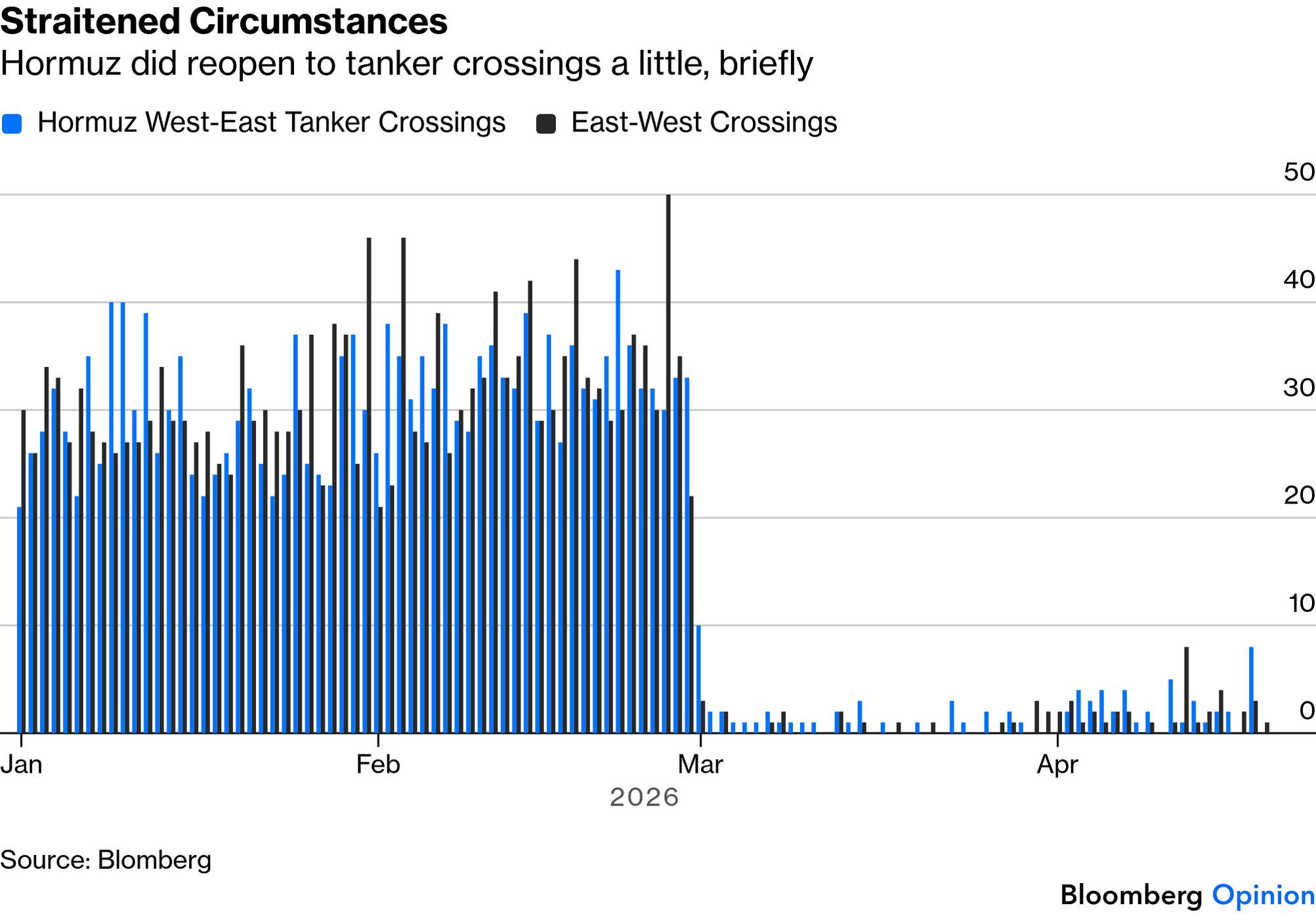

The Strait — through which flows 20% of the world’s oil and many other vital commodities — is not a faucet that can simply open or close. The flow of tankers through the waterway fell virtually to nothing a week into the conflict, and had shown only the slightest sign of recovery:

As oil traders point out, the effects wouldn’t yet be evident in much of the world, as it typically takes a tanker about six weeks to get from the Strait to New York and almost a month to reach Shanghai. Companies keep inventories of oil. The problem is yet to make itself felt with full force in the world’s two biggest economies.

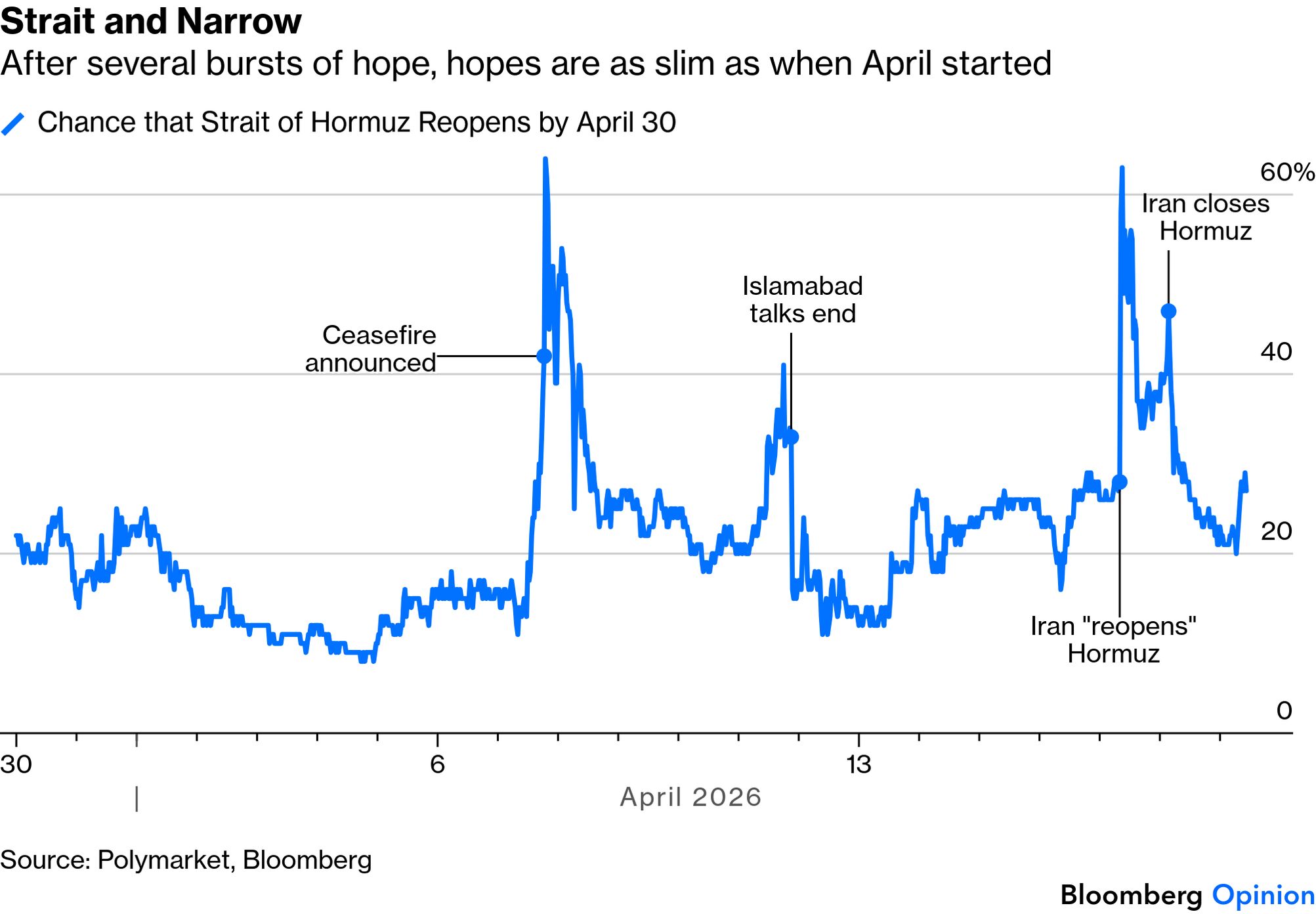

As for the chances of traffic returning to normal by the end of this month (i.e. Thursday of next week), as defined by Polymarket, bettors now think it’s only a one-in-five shot. The gyrations in this probability over the last two weeks have been intense:

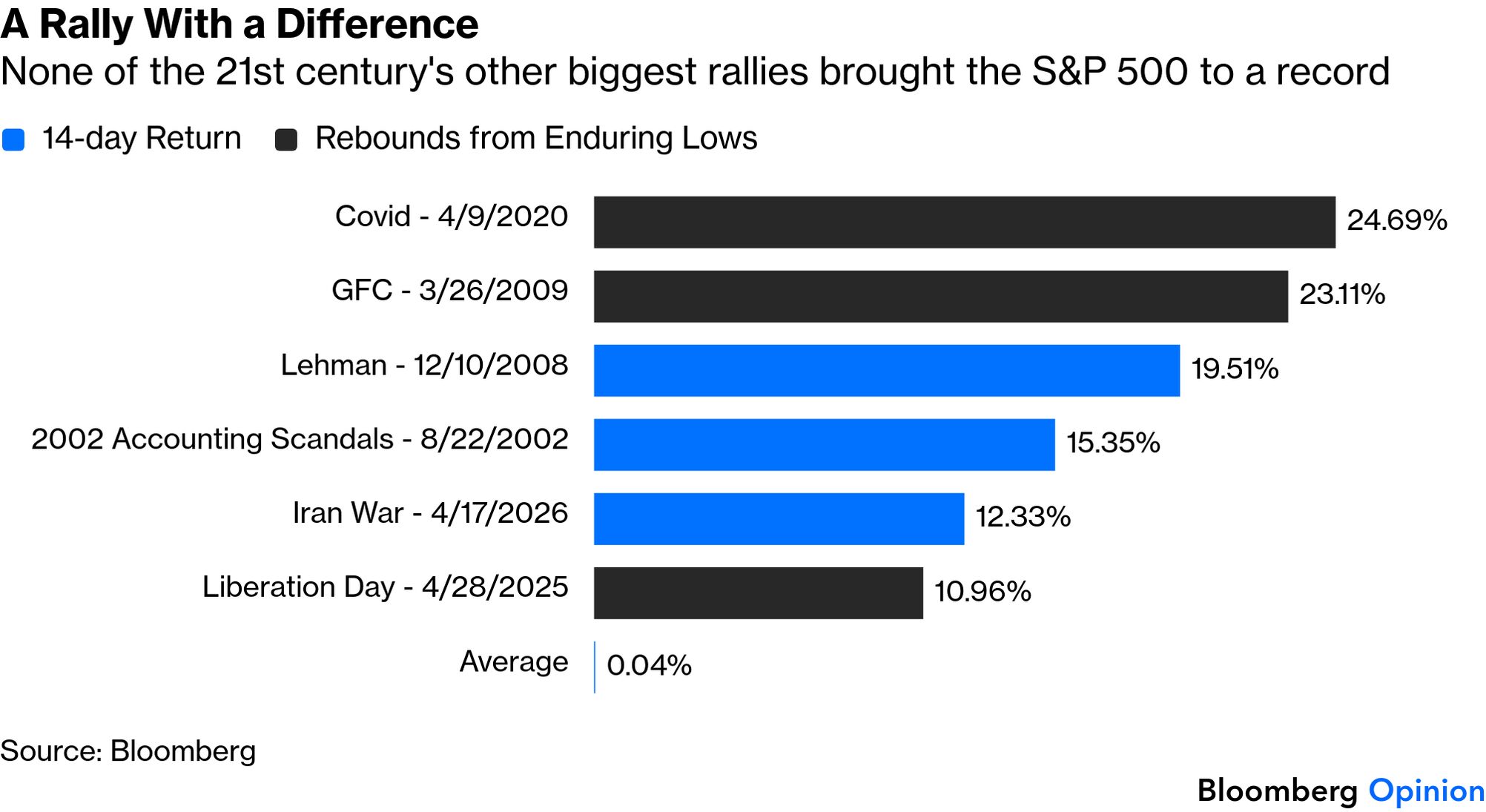

Futures suggest that US stocks will fall Monday on the back of the latest news. They suggested that last Monday, too, after the Islamabad talks broke down, and proved wrong. If Monday is a down day for the S&P 500, it will be only the second since the rally ignited on March 31, catalyzed at the time by a comment from Iran’s President Masoud Pezeshkian that the country was ready to end the war but “needed guarantees.”

In the subsequent 14 trading days, the S&P rose 12.33%, marking only the fifth time this century it rallied so far this fast. It was the first such rally to bring the market to an all-time high. All previous such rebounds came from terribly oversold conditions driven by bad news, and two of them — in December 2008 during the Global Financial Crisis and in August 2002 during the fallout from the dot-com bubble — proved fools’ rallies with a new low to come before the recovery could start:

If the mixed signals from both sides are bizarre, the market rally is even weirder. Many analysts admit to bafflement. This is Academy Securities’ Peter Tchir:

I was nowhere near as optimistic on the broad stock market rally as I should have been. Even today, with the benefit of hindsight, it still seems a bit “magical” (or “mechanical”) how well markets behaved in light of the actual headlines. Not the perception of headlines, but the actual headlines.

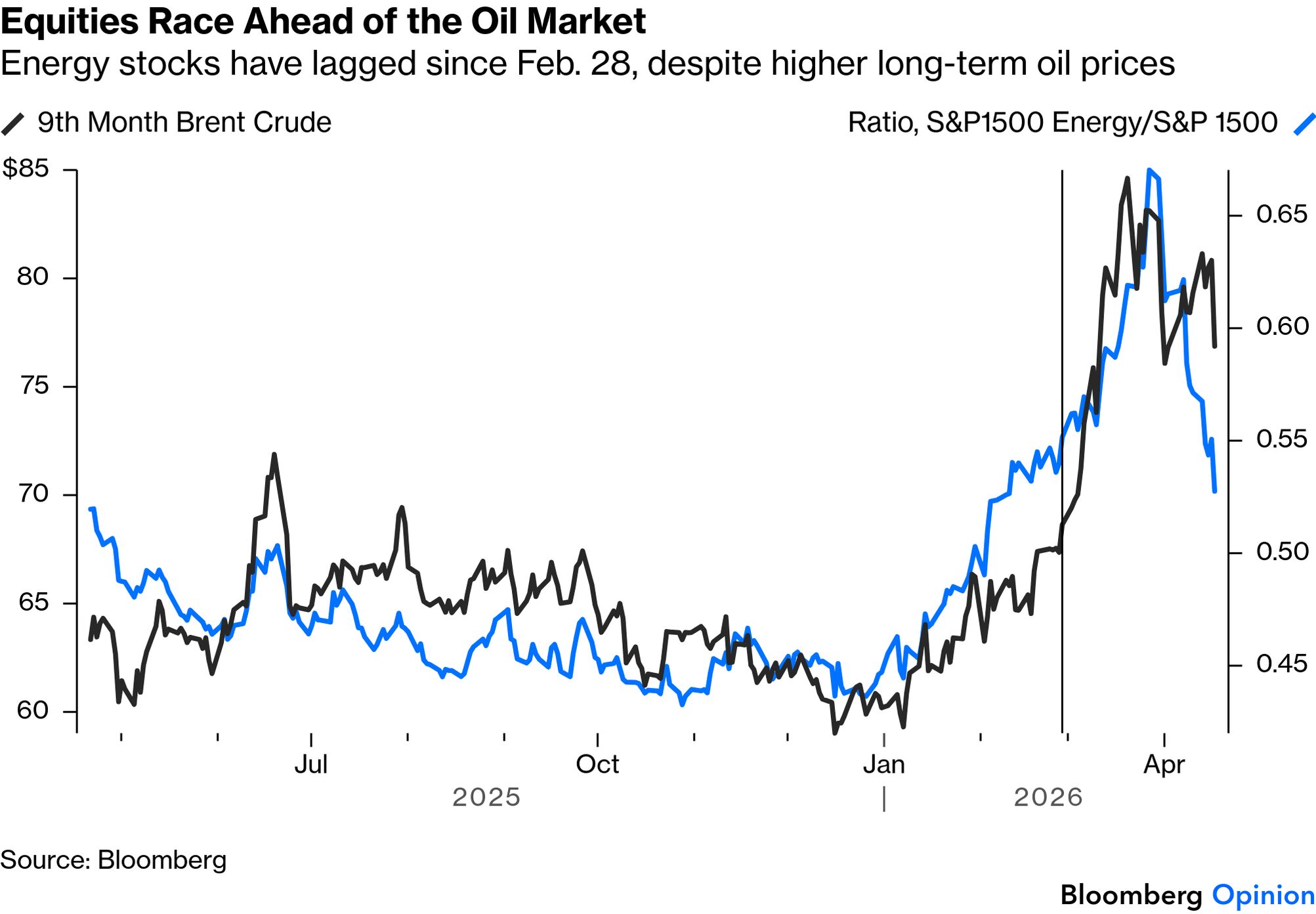

For one illustration, this is how the energy sector’s performance relative to the rest of the market has moved with the 9th-month crude future price. Naturally, energy companies do better when oil is priced to trend higher. The way everyone else has outstripped them over the last two weeks, even as oil traders remain braced for much more expensive oil, is strange:

The oil market isn’t the only factor that drives the stock market, of course. War broke out just as Americans were starting to receive tax refund checks, and at a point where the biggest stocks set to benefit from artificial intelligence had been moving horizontally for many months. A new Fed chairman, who says he thinks rates should be lower, will face his confirmation hearing at the Senate this week.

But it’s hard to attribute this rally to the economy, because data has been disappointing since the war broke out, and particularly as the first numbers reflecting the impact of the Iranian events have been published in the last two weeks. Citi’s economic surprise index provides no excuse for stocks to rally:

But then there are earnings. The prevailing belief is that the effects of this war will have washed out of corporate P&Ls by the end of the year. Excluding the “Magnificent Seven” tech platforms, which gain disproportionately from AI excitement, full-year earnings expectations suddenly took off just as the war started. This is a coincidence, but if brokers had just written up forecasts this much, it’s not surprising that share prices burst upward as soon as the news flow from the war provided an excuse to do so:

On that basis, this rally reflects what happens when a ball that has been held under water is finally released (by improving news from the Gulf) and shoots far above the surface. Provided that some compromise allows the oil to start moving again, the argument goes, it’s dangerous to be out of the market. Beyond earnings forecasts, Gavekal Research’s Nicolas Oudin summarizes:

With the Trump administration appearing to pivot toward de-escalation at all costs, investors face a clear choice: lean into a scenario of rate cuts, a stabilizing US-China trade deal and a continuation of the artificial intelligence capex boom, or take a more tactical “buy the rumor, sell the fact” approach and step back while conditions remain favorable.

It’s understandable that investors chose the first option. But they did so in a stampede that now creates a real risk of a renewed dive if the assumption of de-escalation is tested. The weekend’s news might well provide that test.