Tyskland har i årevis været den mest sparsommelige nation i Europa, men under coronakrisen har Tyskland åbnet pengekassen mere end alle andre, og det kan betyde, at Tyskland er et af de store lande, som først og bedst kommer ud af nedturen. 90 pct. af samfundsaktiviteten er tilbage på nivauet fra før coronakrisen. Men industrien og eksporten kommer dog ikke til at kickstarte økonomien. Derfor bliver hjemmemarkedet helt afgørende – og dermed hjælpepakkerne. Op mod 85 pct. af “fyrede” lønmodtagere er sikret en normal løn i et år. Tyskland vil blive førerhunden i et europæisk opsving.

Germany: Austerity champion turns into a big spender

Thanks to the government’s U-turn on fiscal policy, Germany should be one of the first and strongest countries to emerge from the crisis

Available hard data for the second quarter was dreadful. After declines in March, industrial production and exports continued to drop like a stone in April.

Without any changes in May and June, the economy would contract by up to 30% quarter-on-quarter. However, more experimental and real-time data suggests that the economy has experienced a sharp rebound since the lifting of the lockdown measures. Remember that Germany, together with Austria, was the first eurozone country to start easing the lockdown measures at the end of April.

Google mobility data and the German truck toll mileage index, social-economic activity had returned to some 90% of its pre-crisis level by early June. While the month of April was the worst month ever in terms of economic data, the month of May could become one of the best.

First a ‘v’ but then what?

Looking beyond the expected imminent rebound, the prospects for the two former growth engines of the economy do not look too promising.

Industrial production and exports – which had already been suffering from structural disruptions, the trade war, Brexit uncertainty and less demand from China – are unlikely to kick-start the recovery. During the financial crisis, Asian countries played an important role in the swift recovery of German industry. Today, there is no saviour in sight to boost external demand.

Therefore, the strength of the rebound will depend strongly on domestic demand.

Labour market under pressure

Up to now, a strong labour market had been the main argument in favour of continued strong domestic demand.

However, the tentative increase in unemployment and the sharp surge in short-term work schemes have weakened private consumption. In the current crisis, employees subject to these short-term work schemes will receive up to 85% of their last salary for up to 12 months. At the peak of the financial crisis, some 1.5 million employees were on such schemes.

However back then, it was largely the manufacturing sector which was hurting the most, with some 80% of all employees in this sector working on short-term schemes. In contrast, the current crisis has hit the economy almost indiscriminately, with between 25% and 31% of all employees in the manufacturing sector, trade and services, working on these schemes. The construction sector is one of the few positive exceptions, which has been barely hit by the crisis so far.

We expect German unemployment to increase by another million in the coming 12 months

The 2008/9 crisis briefly interrupted the structural improvement in the German labour market, which had been driven by structural changes in the mid-2000s and long-lasting economic recovery. But there is a strong possibility that the Covid-19 crisis could enhance structural changes. The labour market had already started to bottom out and to show some surreptitious signs of worsening prior to the pandemic. The longer the crisis lasts, the higher the chance the German labour market could re-live memories of a long-forgotten past: hysteresis.

It is currently hard to tell how strong this effect will be, but we expect German unemployment to increase by another million in the coming 12 months.

The remarkable fiscal u-turn

With the serious risk that external demand will not kick-start a sustainable recovery and the fact that Covid-19 has not altered the structural weakness of the German economy, the need for fiscal stimulus has been high. After years of international criticism over the perceived inactivity of the government in relation to investment and its adherence to fiscal surpluses, Covid-19 has led to a full u-turn.

Since the start of the crisis, the German government has been transformed, from austerity champion to big spender. In the first phase of the crisis, the government made more than 30% of GDP available to cushion the economic fallout of the lockdown measures. These measures mainly included guarantees and loans for companies but also compensation of income losses for small enterprises and freelancers, as well as short-term work schemes.

This change of heart on fiscal policy isn’t just good news for the entire eurozone but also good news for the domestic economy

These measures were augmented by a so-called stability fund, which were mainly aimed at supporting bigger companies by eventually taking stakes. The third and final step of the fiscal response was a stimulus package, including a temporary VAT-reduction as well as income subsidies, incentives to buy electric vehicles and a large portion for investment in innovation, R&D and renewable energies.

In total, the government has agreed to close to 10% GDP of cash-out fiscal stimulus and some 30% of guarantees and loans. The latest fiscal package ticks many boxes of a perfect stimulus package as it combines short-term support for the economy with investments and incentives to steer structural changes.

This change of heart on fiscal policy is remarkable. It is good news for the entire eurozone as illustrated by Germany’s role in the development of a European Recovery Fund. But it’s also good news for the domestic economy as it increases the chances that Germany will not only be in pole position at the start of the race but will remain a leader of the pack in what probably will be a long test of endurance.

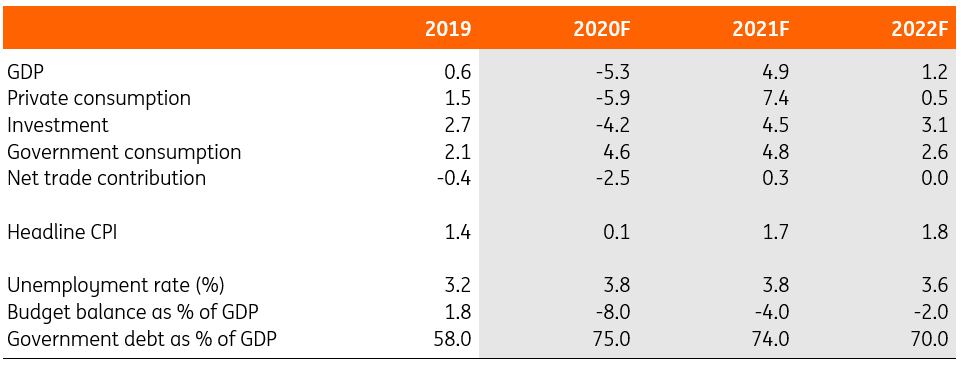

The German economy in a nutshell (%YoY)