Merrill hæfter sig ved, at økonomien har været rimelig god trods coronakrisen. Der er en form for dualisme. Derfor forudser banken, at den amerikanske økonomi vil få en vækst i fjerde kvartal på 3 pct., og at væksten næste år bliver på 4,5 pct.

The Dualism of Market Fundamentals

Dualism, or the quality of having a dual nature especially of opposing principles, seems apropos to current market fundamentals.

The sell-off in global equities recently has focused on the negatives as it relates to event risks like the U.S. elections this week and the rising number of coronavirus cases.

On the other hand, higher bond yields and better performing cyclicals have pointed to rising economic activity. In the backdrop of likely further choppy trading in the weeks ahead, we attempt to explore the dualism that exists within key fundamentals that should ultimately dictate where asset prices are a year from now.

The coronavirus remains the top concern for investors, with cases spiking in parts of the U.S. and Europe. This has changed the reopening narrative to one replete with concern about another shutdown.

A prolonged pandemic would likely be the result of slower progress on the science

front. But as individuals and businesses are learning to adapt, it could be less of a

major headwind to growth as safety precautions are learned and implemented. Over

the course of the eight months since the World Health Organization declared the

coronavirus outbreak a pandemic, society has for the most part tried to limit the

spread of the coronavirus including through social distancing, wearing masks and basic hygiene.

Meanwhile, testing capability has increased, and the healthcare community has

become more skilled at treating patients. Taken together, these have helped to keep

hospitalizations and death rates relatively contained allowing specific regions within

states to continue to steadily reopen.

Even without a firm handle on the coronavirus, a rebound in economic activity has

been possible. Many businesses have been able to hire back workers. The number of

continuing unemployment claims has moved consistently lower, declining by 17 million from its high of 24.9 million in early May.

Small business optimism has improved to levels not seen since the beginning of the

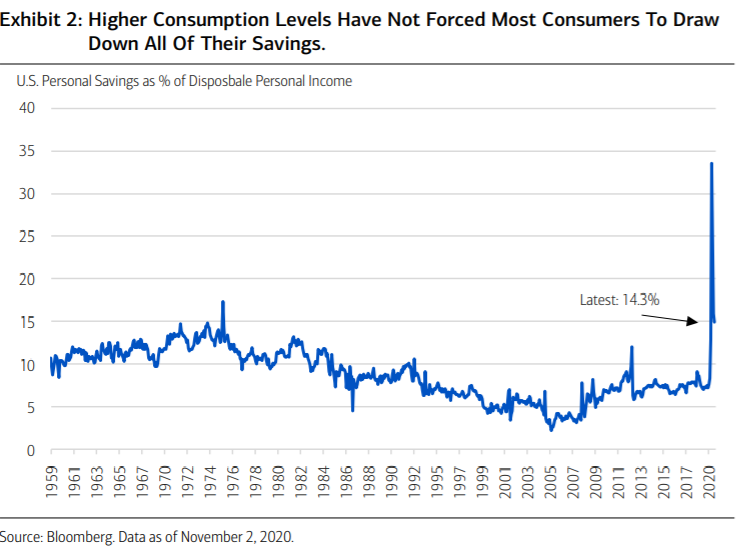

year. Retail sales have surprised to the upside. Higher levels of household savings from earlier in the pandemic have been used to support spending. At 14%, the savings rate is still higher than the pre-pandemic level of roughly 8%, meaning there is still somecushion for consumers

We cannot ignore the possibility of regional shutdowns and further targeted reversals

in reopenings. We do not envision, however, prolonged nationwide shutdowns similar to those enacted in March and April. As such, our base case remains that growth and consumption continue to improve with the expectation of real GDP to be up 3% for Q4 and 4.5% for 2021.