Merrill har analyseret de europæiske tillidsindikatorer og konstaterer, at indikatorerne for erhvervstillid har været langt mere positive den seneste tid end indikatorerne for servicesektoren. Da servicesektoren tæller langt mere i f.eks. Frankrig og Spanien end i Tyskland – henholdsvis omkring 70 pct. og omkring 60 pct. – så er der potentiale for større vækst og dermed kursstigninger i lande med en høj servicesektor, fordi det er der, der har været dramatiske fald sidste år, og fordi det er der, at der kan ventes et stort opsving efter coronakrisen, mener Merrill.

Diverging Paths in Europe

In the final quarter of 2020, the real gross GDP of the euro area contracted by -0.6% from

the prior quarter. In our view, renewed restrictions to limit the spread of the coronavirus

have played an outsized role on the service sector, which comprised 66.2% of the region’s

economy in 2019, according to the World Bank.

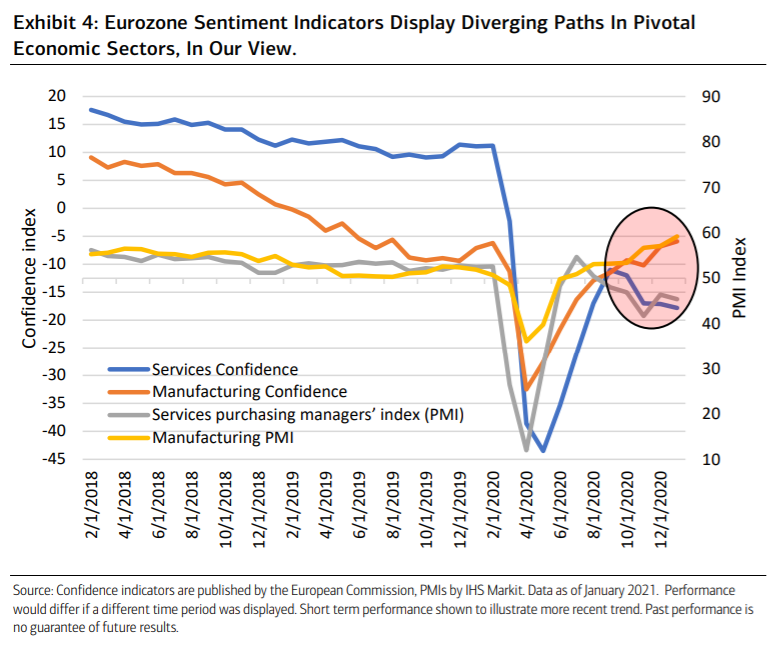

From its nadir of -43.5 in May last year, the European Commission’s service sector

confidence indicator peaked at -11.0 in September but has since fallen to -17.8 in January.

In contrast, with a reading of -5.9 to likely begin this year, its manufacturing counterpart

hit its highest result since August 2019, well before the pandemic hit the bloc.

This

indicator bottomed in April at -32.5. These trends correlate well with those from Markit’s

Purchasing Manager Indexes, which aim to capture business conditions in the private

economy (Exhibit 4).

With 88.2% of the bloc’s economy exposed to trade in 2019, according to the World Bank, manufacturing in the euro area has benefitted off a rebound in the growth of global trade volumes, which rose 1.5% in November on a year-over-year (YoY) basis, the quickest pace since March 2019.

The diverging paths of the service and manufacturing segments of the economy may have

regional implications. On a YoY basis, Germany’s real GDP has currently outperformed

other major euro area economies throughout most of the pandemic, such as those of

France and Spain, according to Bloomberg.

It may not be a coincidence, due to the service sector of the two latter countries having comprised 70.2% and 67.6% of their economies respectively in 2019, compared to 62.6% for Deutschland.

Whether this development becomes prolonged may depend on whether Europe can

accelerate its coronavirus vaccination drive, which would raise expectations for quicker

reopening plans.

This could allow for the service sector segments of these economies to rebound. Once the coronavirus pandemic is under control, governments could take greater advantage of the EU’s fiscal recovery fund and the stimulative monetary policy of the European Central Bank to focus on structural reforms, in our view.