ECB har forøget sit opkøbsprogram PEPP til 1350 milliarder euro – mere end ventet – men Nordea venter, at ECB vil forøge opkøbene senere på året, måske helt op til 2000 milliarder euro. Opkøbene har en mærkbar positiv virkning i Italien. ECB forudser en 8,7 procent minusvækst i eurozonen i år. Afgørelsen i den tyske forfatningsdomstol for nylig om ECB’s opkøb påvirker ikke ECB’s uafhængighed, siger Lagarde.

ECB Watch: More will come

The ECB increased the stimulus both in scope and time. The PEPP stands now at 1 350 bn euros and we expect more to follow. Italian bonds rallied strongly and we see more upside for EUR/USD.

Our main take-aways from today’s meeting:

- More stimulus: The PEPP was increased by EUR 600 bn to 1350 bn euros, the net purchases under the PEPP will run at least until the end of June 2021 and the maturing principal payments from the PEPP will be reinvested until at least the end of 2022.

- Weak outlook: The worst of the corona crisis is assumed to be over but the outlook is very uncertain and the risks are biased to the downside. The ECB staff baseline projections expect GDP to decline by 8.7% in 2020 and recover thereafter. The inflation rate is expected to remain clearly below the ECB target at only 1.3% in 2022.

- Lagarde: Comments during the press conference were very careful and we could not learn much about the possible future steps, while Lagarde did not sound too worried about the possible impact of the German Constitutional Court decision on the ECB’s policies.

- Italian bonds rallied and will now continue to be supported for a longer time. EUR/USD has more upside potential, as the risks regarding the future of the Euro are continue to recede.

Future steps: The inflation outlook is extremely weak. In the ECB staff projections, the core inflation is only 0.9% in 2022 which we expect implies more stimulus to come later this year.

Weak outlook merited more easing

The news from the Euro-area economic developments have pointed to some recovery in the recent weeks but the outlook remains very bleak. News especially from the labour market is very negative which is expected to keep inflationary pressures very low or even negative. The ECB sees the path of recovery to be gradual at best.

As a reaction to the dark outlook, the ECB decided to increase the size and length of the monetary policy stimulus at today’s meeting. According to Lagarde, there was a unanimous view that action was needed.

The emphasis of the policy tools continued to be around the PEPP which was increased in size and will also last for longer. The increase of the PEPP by 600 bn euros was slightly more than was widely expected and showed determination of the ECB to be active in its stimulus policies. Given that the medium-term outlook has worsened and there is probably now a wider consensus that the negative impact of the corona crisis will last long, it was not a surprise to see the programme run longer than originally decided.

The ECB continues to focus on other measures than policy rates and our view is that the rates will remain at their current levels for the years to come.

Future steps

Regarding the possible future steps, Lagarde was asked for example about the possibility of buying bank bonds, lending directly to the SMEs or including the downgraded bonds to the purchase programmes. Lagarde was not willing to comment on any of these steps but continued to emphasise the PEPP as the main tool to target the pandemic crisis.

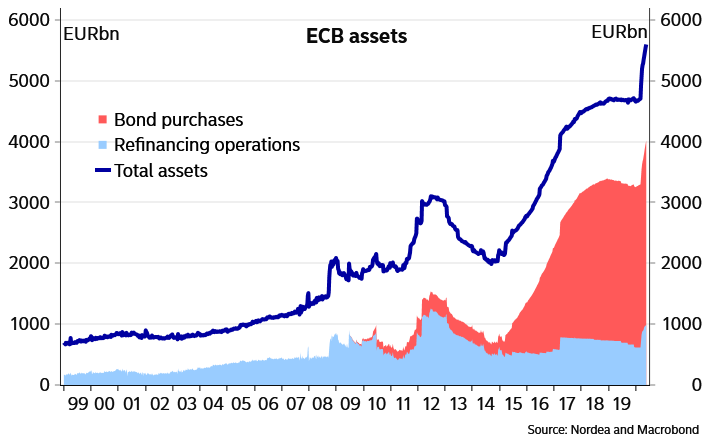

We expect another extension in time and scope of the PEPP later this year but would not rule out also the use of other tools to tackle the currently very weak development in the Euro area. Our expectation has been 1500 bn euros for PEPP but given the increasing public debt burden it seems that even 2000 bn euros could be purchased without completely losing the idea of capital key and issuer limits which despite Lagarde’s talks seems to be guiding the purchases (read our analysis on the purchases here). In June, the ECB will learn about the attractiveness of the TLTROs and those terms could of course be further loosened, especially if the demand disappoints the ECB.

Not much about Karlsruhe at this stage

Lagarde was asked a number of times to comment the recent decision by the German Constitutional Court. Lagarde’s comments were well prepared and careful. The PSPP has been analysed by the European Court of Justice and recognised of being in line with the ECB’s mandate. The decision has been directed at the German Parliament and Government and according to Lagarde, there will be a solution without compromising the independence of the ECB nor the superiority of the ECJ.

Very low medium-term inflation forecast main reason to act

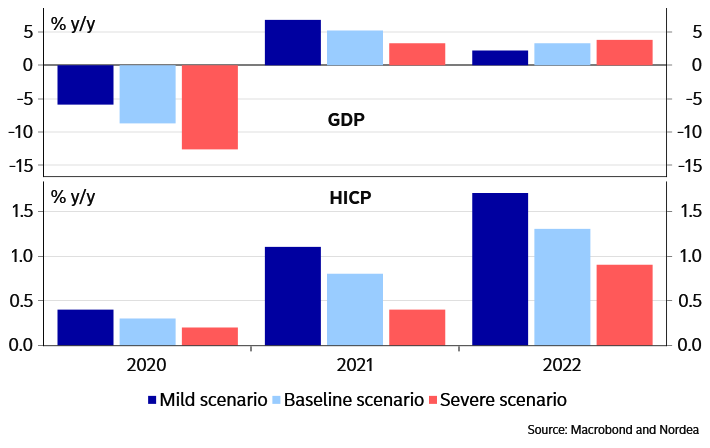

The new staff macroeconomic projections illustrate the ECB’s take on the damage caused to growth and inflation in the Euro area from the pandemic. As was already hinted at in the last weeks, the baseline for growth in the new forecasts lands somewhere between the “medium” and “severe” scenario the ECB presented in April, with GDP at -8.7% y/y in 2020 and 5.2% y/y in 2021 (which is very close to our forecast). A further decline in GDP of 13% is expected for the second quarter, and at the end of the 2022 EA GDP is still below the level of 2019.

Much more interesting however is the outlook for inflation. For this year, the inflation forecast has been revised down significantly to 0.3% y/y, and also at the end of the forecast horizon inflation is seen well below the ECB’s target, at 1.3%. Core inflation was revised down even more strongly, to 0.9% in 2022. In the press conference, Lagarde takes this worrisome medium-term inflation outlook as the main reason justifying the increase in measures announced today.

Big downward revisions in both growth and inflation in the ECB staff macroeconomic projections

As the baseline is surrounded by an exceptional degree of uncertainty, the projections are accompanied by two alternative scenarios along with the baseline. Lagarde remarked that the balance of risks around the baseline are judged to be to the downside, so the severe scenario is probably more relevant than the mild scenario. In their baseline scenario, the ECB “assumes only partial success in containing the virus, with some resurgence in infections over the coming quarters, necessitating persistent containment measures until a medical solution becomes available, which is assumed to happen by mid-2021.”.

ECB’s alternative scenarios

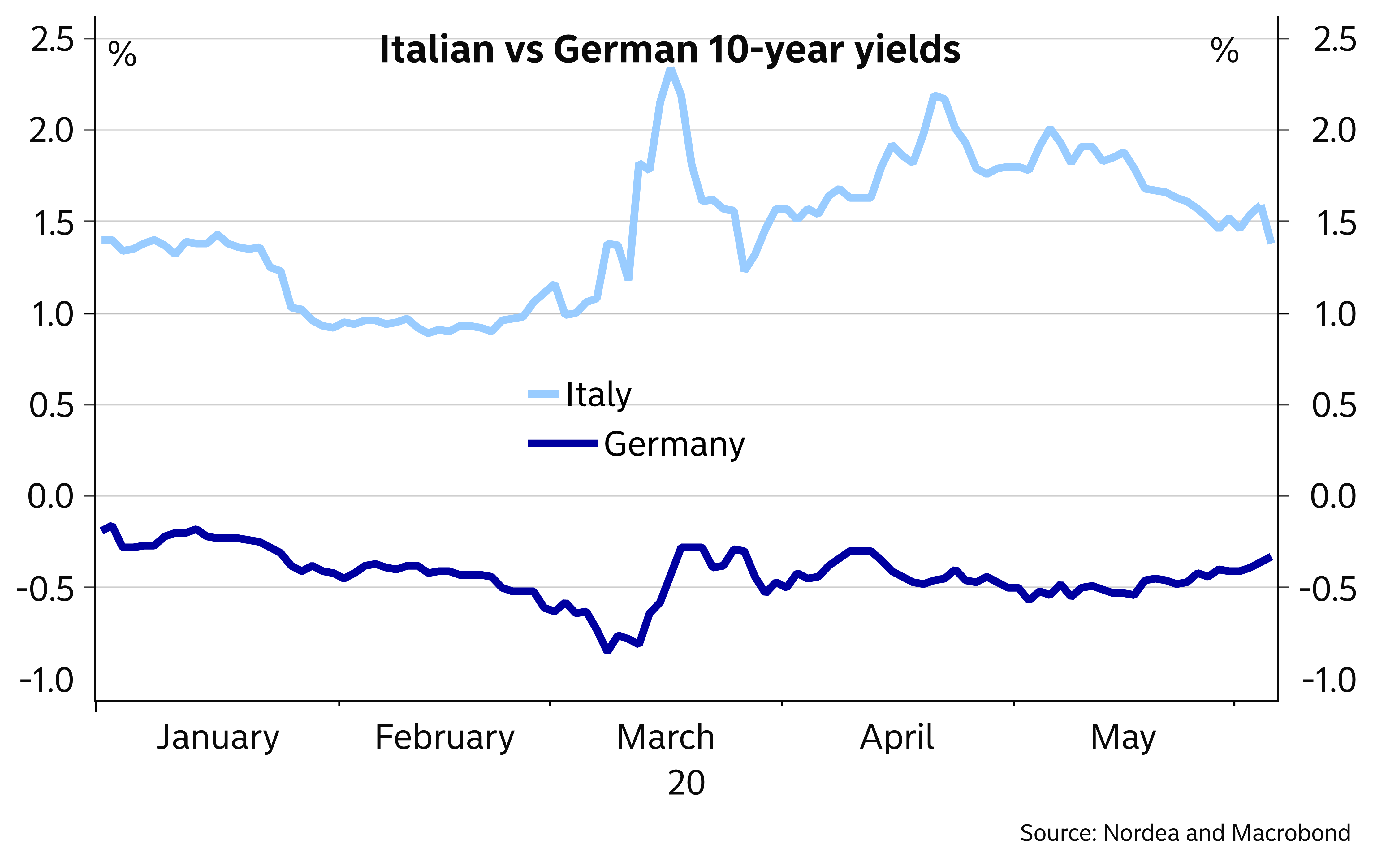

Big rally in Italian bonds

The biggest beneficiary of today’s ECB action appears to be Italy, with Italian bonds posting a strong rally. This is understandable given that today’s decisions ensure that large-scale ECB purchases will continue at least into the middle of next year. After all, large government issuance needs will continue for sure past the acute phase of the corona crisis. While the PEPP data released just a few days ago implies that the PEPP is not as flexible as the ECB has advertised, the larger PEPP envelope and the longer duration of the programme will ensure the ECB will be able to continue supporting countries like Italy in significant magnitude for a longer time.

It will be interesting to see, whether the increase in the PEPP envelope will lead to any changes in the pace of buying. Most likely the pace of purchases will not at least increase now that government bond markets have been working rather well again. Government bond markets will continue be sensitive to news on how the discussions on the Commission’s recovery fund are proceeding, but the ECB’s continued support should shield the markets from more serious bouts of volatility for now – unless of course the political situation suddenly deteriorates in Italy or the economy takes an abrupt turn for worse.

German yields climbed a bit following the ECB’s message. One can find some steepening potential for the German curve. First, the ECB will target its purchases to the shorter end of the curve, where most of the issuance takes place. Second, the recovery fund proposal will shift some credit risk for Germany to bear, and if the fund manages to lift hopes about an economic recovery even mildly, it should put some upward pressure on longer German bonds. In the big picture, however, German yields will most likely remain low.

The EUR continued to strengthen on the ECB news, as the risks regarding the future of the Euro area fell further. We see further upside ahead for EUR/USD. The allotment of the next targeted longer-term refinancing operation (TLTRO), the first with the new looser terms, on 18 June will be interesting. Weak demand there could further help the EUR, as it would mean a smaller increase in excess liquidity.