ING gennemgår finansieringen af EU’s nye og gigantiske Covid-19 fond, der skal hjælpe EU-landene med at komme gennem coronakrisen. Private investorer ventes at købe hovedparten af fondens obligationer. ING venter, at der skal udstedes ca. 800 milliarder euro over de kommnde seks år.

The second wave of debt: EU Covid-19 funding and market reaction

September sees the start of EU Covid-19 funding programmes. We look at the borrowing needs from various EU supranationals, the potential for ECB support along with the market impact. EUR supra will undergo a step change in borrowing and private investors will be required to buy most of the new debt. And we think they’ll require cheaper valuations.

Coronavirus response: EU supranationals are coming of age

EU and Eurozone member states have learnt their lesson from the previous crisis. If the monetary union is to survive the current economic shock, its response needs to be forceful and coordinated. Between April and July, member states agreed on a range of crisis-fighting tools to support countries with the least fiscal space.

Most of these entail a degree of joint issuance from existing EU and Eurozone supranational entities. While these entities are already known issuers on the debt market, the new crisis-fighting apparatus means a step-change in the amounts to be raised.

Below, we detail our debt sale expectations from European supras in the coming years. We also discuss the implications for the EUR debt landscape, in particular the behaviour of traditional safe debt buyers and their possible market impact.

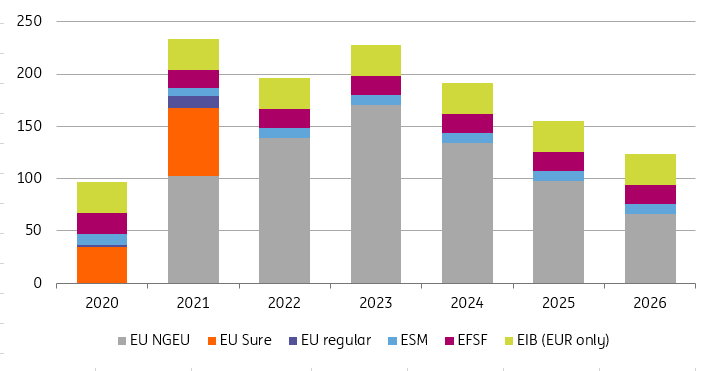

Estimated annual funding needs of European Supras (EURbn)

Source: EU/ESM/ING

The funding impact of the Covid-19 response on European supranationals

Around €1090bn in financial assistance has been made available by various EU entities in response to the coronavirus epidemic and its economic consequences. This should, in theory, require commensurate debt funding from European supranational issuers.

We think debt issuance of around €800bn over the next six years to fund these programmes is a more realistic figure. Here are the details:

Læs hele rapporten fra ING her: