Saxo Bank har analyseret den tyske og europæiske inflationsudvikling og konkluderer, at den tyske inflation er blevet højere end ventet, på 5,1 pct., og at den bider sig fast og breder sig til større dele af samfundet. Det er ikke kun en pandemi-virkning. Nu rammer inflationen for alvor husholdningerne, og det kan påvirke forbruget. Banken venter, at inflationen for hele året bliver højre end i 2021 – på 4 pct. Den højere inflation vil lægge pres på ECB for at reagere, men Saxo Bank tror ikke, at ECB på sit møde på torsdag vil sætte renten op.

Chart of the Week : German inflation

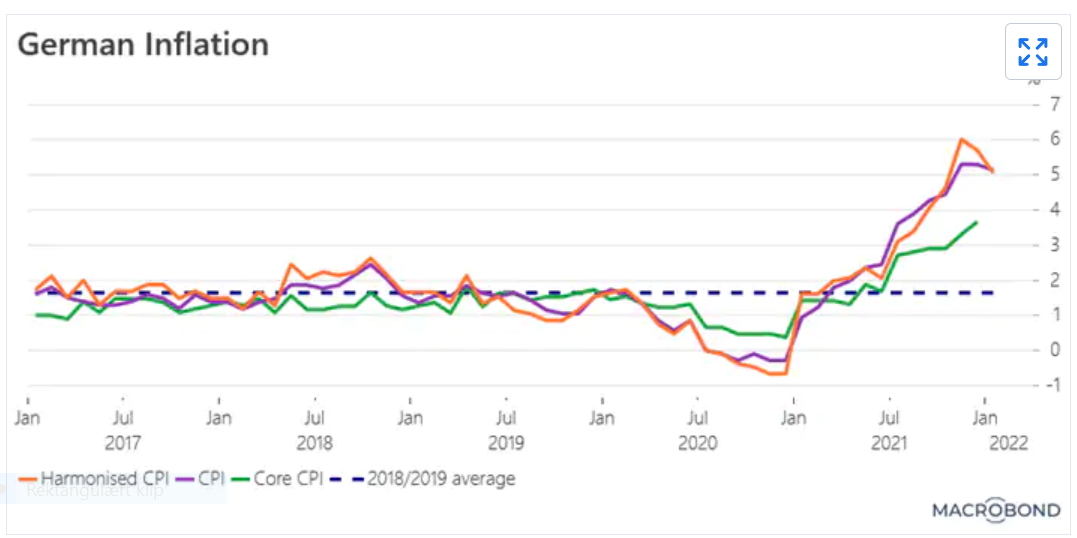

Summary: Our ‘Macro Chartmania’ series collects Macrobond data and focuses on a single chart chosen for its relevance. This week, we focus on the first estimate of Germany’s inflation for January.

Click here to download this week’s full edition of Macro Chartmania.

Germany’s Harmonised Index of Consumer Prices (HICP) is out. According to a first estimate, it stood at 5.1 % year-over-year in January, from 5.7 % in December. This is much higher than the economist consensus of 4.7 %. We had upside surprises in other eurozone countries. Spain January HICP decreased less than expected, at 6.1 % year-over-year versus anticipated 5.5 %, for instance.

On a positive note, the base effects from the VAT reversal no longer show in Germany’s year-over-year print. This was expected. But inflation remains elevated. The VAT base effects were partly offset by strong energy prices (gas notably) and transportation costs and some services too (packaged holidays and leisure).

There is growing evidence that inflation is becoming more broad-based and that the services component could be the main headache in the coming months. Higher inflation is also passed on to households. This is negative for consumption.

Since the beginning of the year, prices have started to increase, sometimes quite sharply. Think TV broadcasting prices and even various kinds of administrative prices.

Looking ahead, we expect average inflation will be higher this year than last year in Germany. The peak in inflation is certainly not behind us yet and could be reached only in the next two to three months. And if the energy crisis is back in winter 2022, we don’t see how inflation could retreat to 2 % on average anytime soon. We forecast that German inflation will average 4 % this year with risks tilted on the upside.

Inflation surprises in the eurozone will likely force the European Central Bank (ECB) to revise upward its inflation projections in March. The ECB staff projected a 60 basis point drop in the euro area HICP in Q1 this year. This is way optimistic. But the ECB is likely to refrain from changing its monetary policy in the near term.

The staff still considers the bulk of inflation is mostly related to the pandemic effect and the imbalances between demand and supply. This is partially true. There are other structural factors pushing inflation higher, such as the green transition and wage-price spiral in some sectors, in our view. This should not be neglected.

Following the release of the German inflation, the money markets have readjusted their expectations. They now price a 10 basis point ECB rate hike by September (which was not the case previously) and over 25 basis points by December. We think the ECB will face quite a communication challenge later this week.

On one hand, it will have no choice but to confirm a more hawkish stance on inflation (it cannot dismiss the recent inflation figures) and on the other hand, it will have to keep the money market speculation on an upcoming rate hike in the coming months at bay. Expect volatility on EUR crosses on Thursday afternoon, for instance.