In many ways, David Einhorn’s Greenlight appears to be back to its “new normal” – in a letter sent to investors, Einhorn writes that Greenlight again underperformed the market and returned -0.1% in the first quarter, badly underperforming the 6.2% return for the S&P 500 index, before proceeding to bash the Fed, broken markets, Chamath and Elon, the basket of short stocks and much more.

That said, even though as Einhorn writes Greenlight made only a handful of portfolio changes and essentially broke even, “a lot happened. In general, the investment environment – especially from mid-February through the end of the quarter – was favorable as value outperformed growth, and interest rates and inflation expectations rose.”

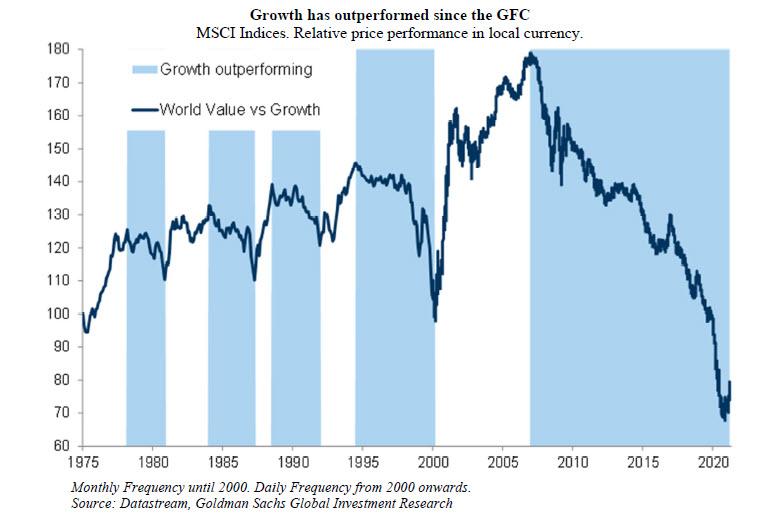

He then asks if the tide has finally turned from Growth to Value, noting that “after a very tough decade, we have only just begun a recovery as shown in this 45-year chart from Goldman Sachs research:”

Part of the shift from growth to value, Einhorn writes, may be coming from higher inflation and inflation expectations. As measured by the inflation swap market, 10-year inflation expectations fell from 2.9% in September 2012 to 0.8% in March 2020. The only significant intervening bounce came in 2016, when expectations jumped from 1.5% to 2.3% on expectations of a major stimulus deal from the Trump admin (which never materialized). It is hardly a coincidence that that was the only year in the last decade in which value outperformed growth, as the Greenlight head notes. Fast forward to now, when after bottoming in March 2020, inflation expectations have recovered to 2.5%. The trend became clearer in the middle of May, and value started outperforming growth then, and especially since the middle of February. Indeed, aince May 15, the value-heavy Greenlight returned 80% of the S&P 500 index with half the net exposure.

Einhorn is even more optimistic about the future when it comes to the “growth to value” rotation:

When the time comes, we will have to figure out how to perform better in deflationary periods. But for now, we believe inflation is only going one way – higher – and we are optimistic about our prospects. The wind is now at our backs. The economy is in full recovery mode. Household balance sheets are stronger than they have been in a long time and household income growth was up 13% in February compared to last year. And this is before the latest $1.9 trillion – with a “T” – pandemic relief stimulus. Corporate capital spending is booming. There are shortages and bottlenecks everywhere. Last month nearly one million jobs returned. There are signs of an emerging labor shortage.

As for the Fed, the Greenlight boss writes that “it fundamentally changed its framework last August. It no longer seems to care that monetary policy works with a lag. Actually, it has embraced an asymmetrical inflation policy: The Fed wants to be ahead of the curve on the downside to protect the stock market and corporate bondholders the economy. Behind the curve is fine on the way up no matter how frothy the stock market the recovery is. Now, it says it is only going to react to actual inflation that exceeds its 2% target for a period of time.”

The letter then goes on to muse how the Fed will know when it is blowing the next bubble, and to stop:

… the Fed has indicated that it believes any abnormally high inflation will be transitory. We wonder, how will the Fed know? Do price increases come with a label that says “transitory”? Our sense is that no matter how hot inflation gets in the coming months, the Fed will continue with zero interest rates and large-scale asset purchases. After all, the U.S. Treasury has a lot of debt to sell and it isn’t clear who, other than the Fed, can absorb the supply.

It’s not just Powell who is throwing caution to the wind: so are such mainstream econ “experts” as John Oliver:

The bipartisan idea that deficits don’t matter has even reached popular culture. John Oliver dedicated an entire episode of Last Week Tonight to browbeating anyone who is concerned about the growing national debt. His argument boiled down to: (1) nobody knows how much debt is too much; (2) we have a good need to spend money now; and (3) it won’t be a problem until inflation shows up, and we can deal with it then.

To this, Einhorn’s response is simple: “Though one can debate whether the official government statistics are contrived to avoid capturing inflation” – and as we have repeatedly noted, inflation is now decidedly a political measurement, one which has been gamed for decades to make it appears as low as possible “shortages and bottlenecks accompanied by rising demand can only be solved through increased capacity and higher prices. We have also reset the baseline income for non-working adults; it will take higher wages to bring those marginally attached to the labor force back to work.”

Concluding this part of the letter, Einhorn writes that while the Fed says it has the tools to fight inflation (and according to Bernanke can cut it in 15 minutes), “it remains to be seen if it will have the stomach to use them when the time comes. That is a discussion for another day. Right now, we remain positioned for rising inflation and inflation expectations.”

The Greenlight letter then goes on to lay out just how it plans to capture these rising inflation expectations, listing its top positions as follows, and how they performed in the frist quarter:

- Brighthouse Financial (BHF, +22%) benefitted from rising interest rates;

- Danimer Scientific (DNMR, +61%) began its life as a public company;

- Concentrix (CNXC, +52%) benefitted from strong demand and rising estimates;

- Resideo Technologies (REZI, +33%) was helped by the strong housing market;

- Change Healthcare (CHNG, +18%) agreed to be acquired by UnitedHealthcare;

- AerCap Holdings (AER, +29%) agreed to acquire GE Capital’s aircraft leasing business (GECAS) at a discount; and

- An undisclosed healthcare short (-41%) fell due to reduced government reimbursement for its product.

(incidentally, at quarter-end, Greenlight’s largest disclosed long positions were Atlas Air Worldwide, Brighthouse Financial, Change Healthcare, Danimer Scientific and Green Brick Partners, with a net average exposure of 118% long and 81% short).

Which is not to say that there were no glitches. One was underperformance by homebuilder and land-developer GRBK, the fund’s largest position (more on this in the full letter below). The other performance drag was – as usual- Greenlight’s “short basket” of bubble stocks.

What follows next is a tour de force from Einhorn lashing out at all the ways the market is broken, and how the Reddit insanity of Q1 exposed it for all to see:

In late January, the market came to focus on companies with large short interests. Despite having a diversified portfolio, a number of our positions fell into this group and experienced sudden, sharp rises. We adjusted to the dynamic by reducing our exposure to single name shorts, both in number and sizing. To mitigate the potentially uncomfortable net long bias that would have resulted, we added macro hedges of market index and index option shorts. While we do not expect this to be a permanent change, we will evaluate and modify as we go. The performance of our short portfolio in 2020 and in early 2021 was unacceptable, so change is certainly needed. If we swing a little less hard, we should hit more balls. We have also revised our internal analyst incentive structure to fully emphasize alpha creation.

Much has been made of the short-squeezes in late January. In fact, Congress held hearings, where it called the leaders of Robinhood, Melvin Capital and Citadel and an individual investor who made a great call on GameStop (GME) to testify. We have a few thoughts about this to share.

First, it is very healthy for market participants to discuss and debate stocks. This is true both privately and publicly. There are rules about fraud and manipulation that need to be followed, but investors discussing why they think GME (or any other stock) should go up or down ought to be encouraged. There is no reason to drag anyone before Congress for making a stock pick.

Second, it is also fine to make bad stock picks. If a hedge fund takes a big position in a stock and is wrong, it loses money. Isn’t this how it is supposed to work?

Third, payment for order flow is just disguised commissions. We are in a world where consumers, especially young ones, expect internet services to be free, or at least free to them. A quote widely attributed to Richard Serra about commercial TV in 1973 says it best: “You’re not the customer; you’re the product.” If you want the broker to work for you, pay a commission.

Fourth, Robinhood suspended trading in certain stocks because it was undercapitalized. It is possible that it wasn’t following the regulatory requirements. A regulatory sanction is probably appropriate – but as we’ll discuss below, we won’t be holding our breath.

The punchline: Einhorn slamming Chamath and Elon for pouring the “real jet fuel” on the GME squeeze:

Finally, we note that the real jet fuel on the GME squeeze came from Chamath Palihapitiya and Elon Musk, whose appearances on TV and Twitter, respectively, at a critical moment further destabilized the situation. Mr. Palihapitiya controls SoFi, which competes with Robinhood, and left us with the impression that by destabilizing GME he could harm a competitor. As for Mr. Musk, we are going to defend him, half-heartedly. If regulators wanted Elon Musk to stop manipulating stocks, they should have done so with more than a light slap on the wrist when they accused him of manipulating Tesla’s shares in 2018. The laws don’t apply to him and he can do whatever he wants.

Many who would never support defunding the police have supported – and for all intents and purposes have succeeded – in almost completely defanging, if not defunding, the regulators. For the most part, quasi-anarchy appears to rule in markets. Sure, Dr. Michael Burry, famed for his role in The Big Short, reportedly received a visit from the SEC after tweeting warnings about recent market trends – and decided to stop publicly speaking truth to power. But for the most part, there is no cop on the beat. It’s as if there are no financial fraud prosecutors; companies and managements that are emboldened enough to engage in malfeasance have little to fear.

Einhorn then concludes with three anecdotes to demonstrate his argument that this is not only an “anything goes” market where crime is rampant, but proving just how broken the market has become.

First, consider the investigation of Tether by the Office of the Attorney General of New York (OAG). As Einhorn explains, “tether is a cryptocurrency that is always worth a dollar (the value is “tethered” to the dollar). Tether is one of the largest cryptocurrencies with about $40 billion outstanding, yet it has not been audited or regulated in any serious manner. In theory, Tether is supposed to have $1 of cash backing every Tether issued. Except it didn’t, at least when it was investigated.” Incidentally, for anyone still confused, Tether is how the Chinese launder billions in domestic funds abroad and outside the Chinese firewall as we explained in December, although so far few have the desire to expose this reality. In any case, here is Einhorn’s lament:

The OAG conducted a two-year probe and found that Tether deceived clients and the market by overstating reserves and hiding approximately $850 million of losses around the globe. Tether and its sponsor, Bitfinex, “recklessly and unlawfully covered up massive financial losses to keep their scheme going and protect their bottom lines,” said the OAG. Further, “Tether’s claims that its virtual currency was fully backed by U.S. dollars at all times was a lie.”

Did the OAG shut down Tether? Did anyone get arrested or even lose their job? Was the regulatory infrastructure changed to make sure this doesn’t happen again? No, of course not. The OAG assessed an $18.5 million penalty and Tether agreed to discontinue “any trading activity with New Yorkers.” It was as if Bernie Madoff had been told to pay a small fine and stop ripping off New Yorkers, but to go ahead and have fun with the Palm Beach crowd.

Einhorn next highlights one of the stocks most hated by the bearish community: GSX:

The media is focused on how the banks allowed excessive leverage and poorly (or properly) managed their risks. The real story is how Arch-Egos was able to buy up most of the float of GSX Techedu, causing the stock to soar 400% in the face of unrefuted allegations of massive fraud. The SEC has an ongoing investigation of GSX but appears to not have noticed a single fund (or a small group of funds) essentially cornering the market. A traditionalist could say this was market manipulation and transparently illegal.

The professional poker player finally points out some of the insane moves observed in pennystocks in Q1, focusing on a tiny deli owner in rural NJ:

Strange things happen to all kinds of stocks. Last year, on one day in June, the stocks of about a dozen bankrupt companies roughly doubled on enormous volume. Recently, the Wall Street Journal reported a boom in penny stocks.

Someone pointed us to Hometown International (HWIN), which owns a single deli in rural New Jersey. The deli had $21,772 in sales in 2019 and only $13,976 in 2020, as it was closed due to COVID from March to September. HWIN reached a market cap of $113 million on February 8. The largest shareholder is also the CEO/CFO/Treasurer and a Director, who also happens to be the wrestling coach of the high school next door to the deli. The pastrami must be amazing. Small investors who get sucked into these situations are likely to be harmed eventually, yet the regulators – who are supposed to be protecting investors – appear to be neither present nor curious.

We don’t find it at all surprising that Einhorn’s conclusion from his capital markets observations over the past quarter is identical to ours, when we discussed the insane stock moves that dominated much of January and February:

“From a traditional perspective, the market is fractured and possibly in the process of breaking completely.”

Einhorn’s full letter is below: