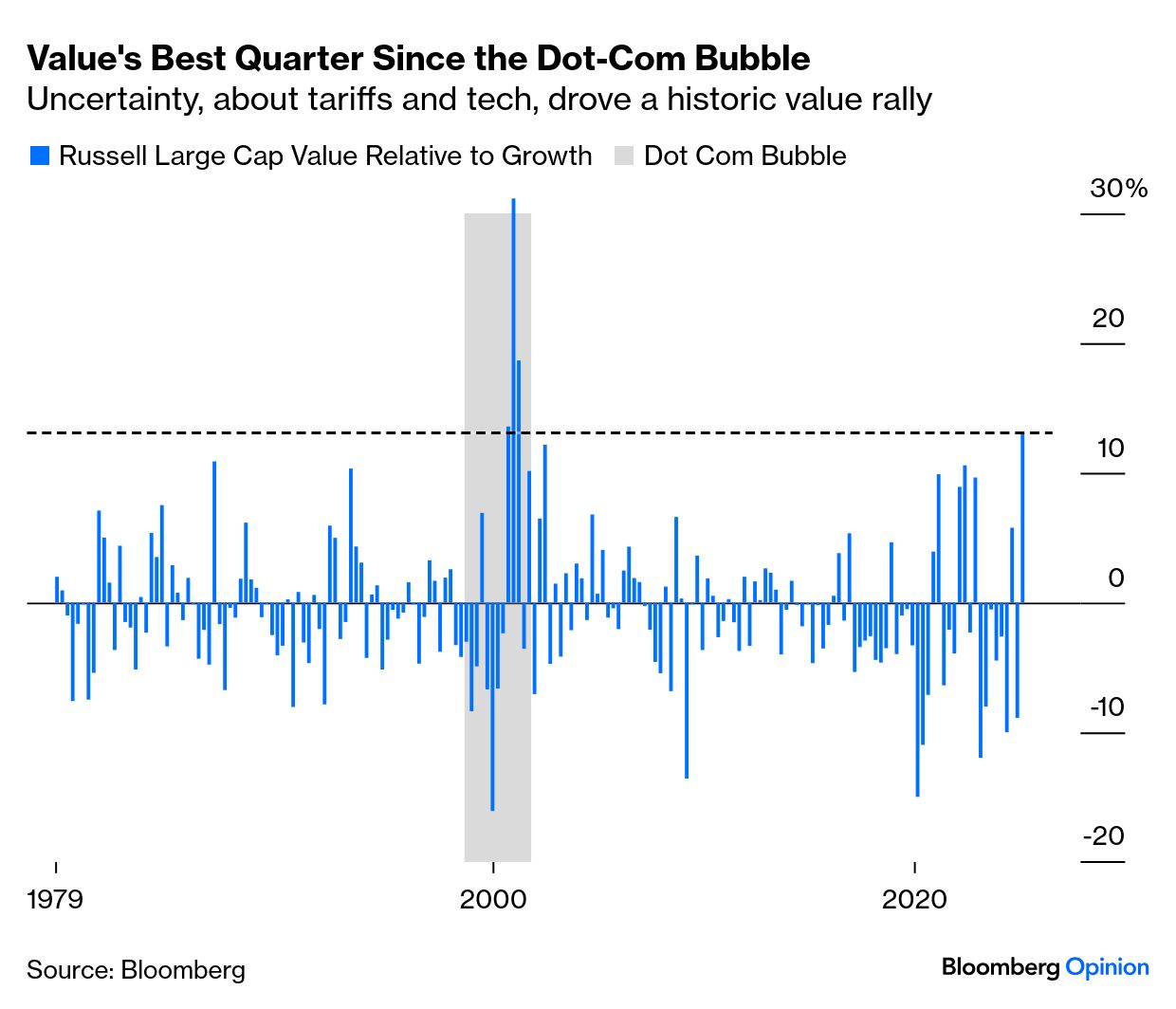

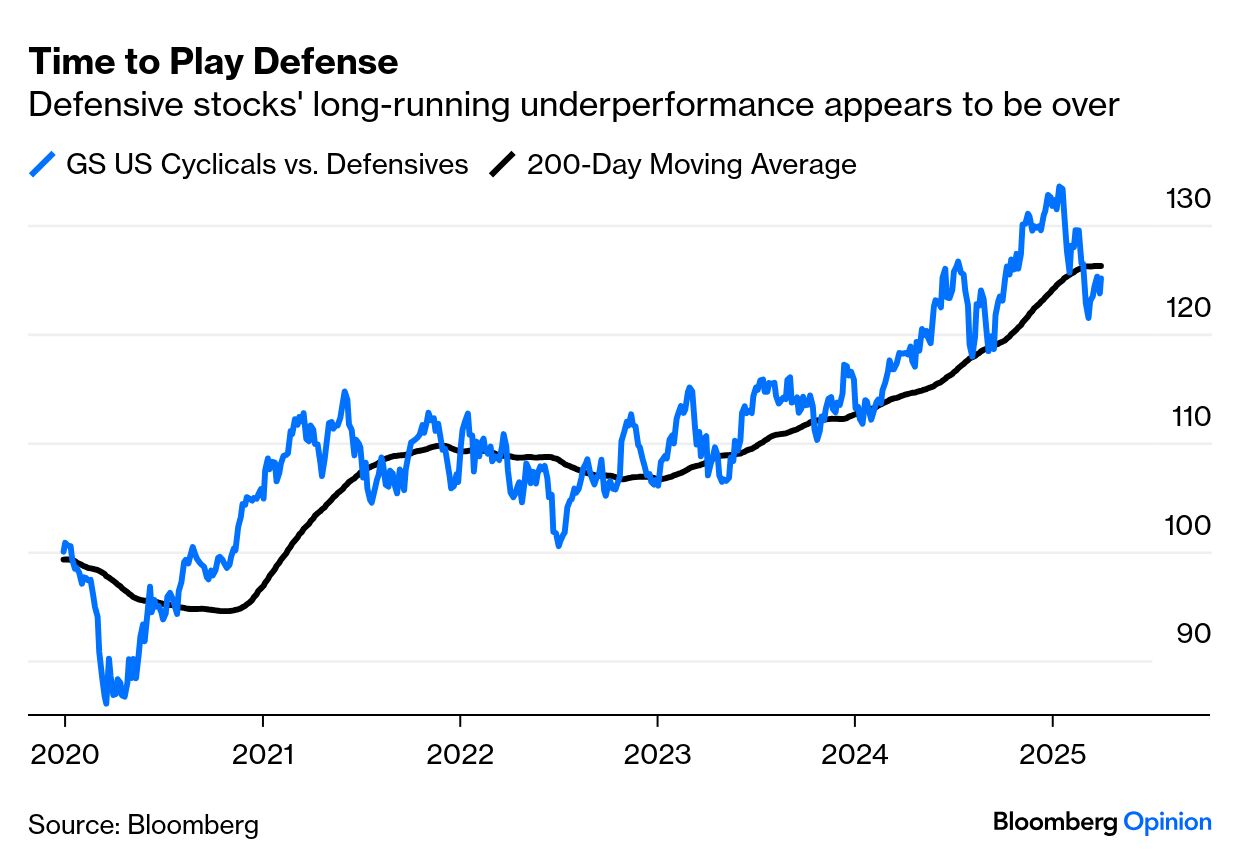

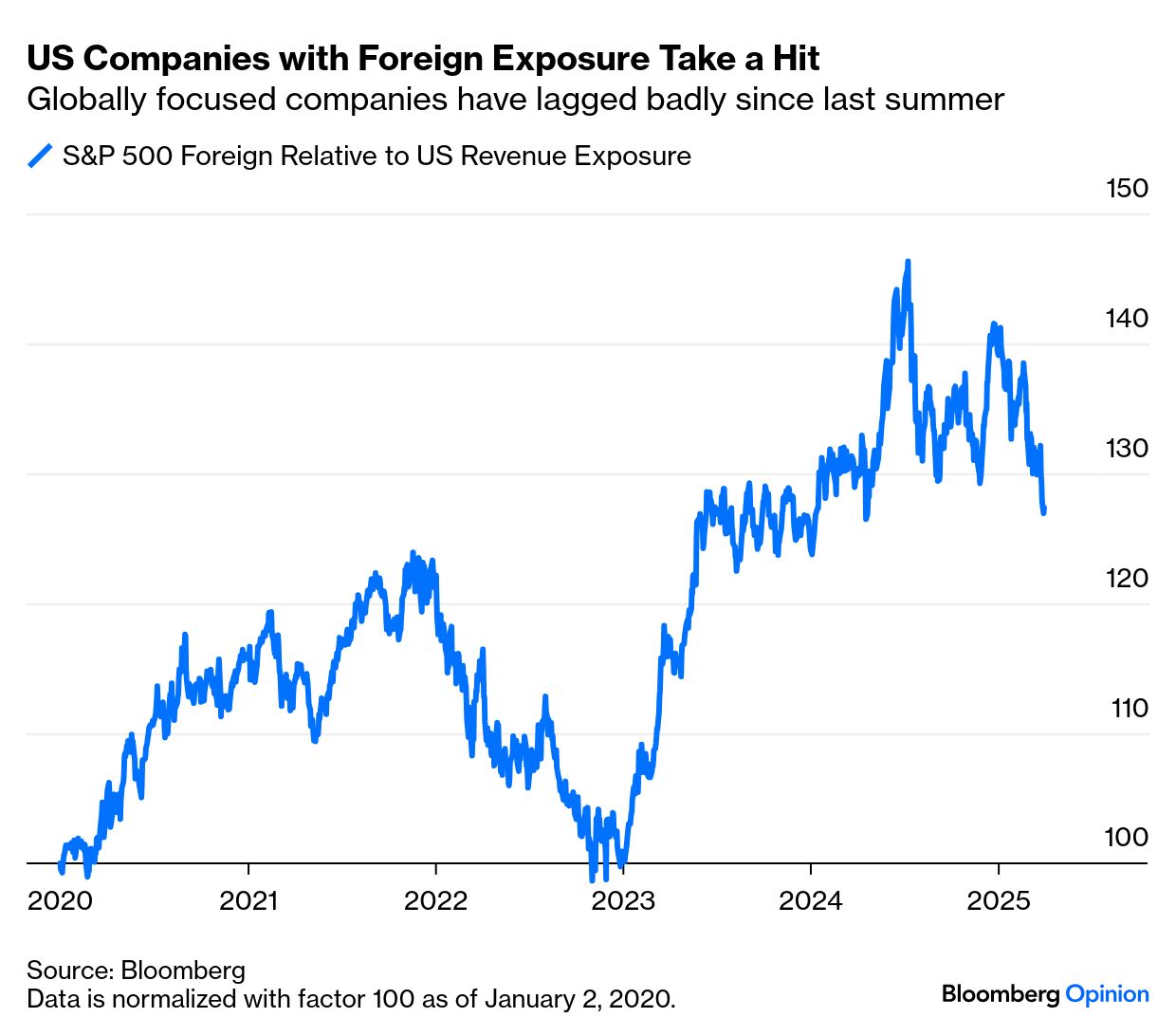

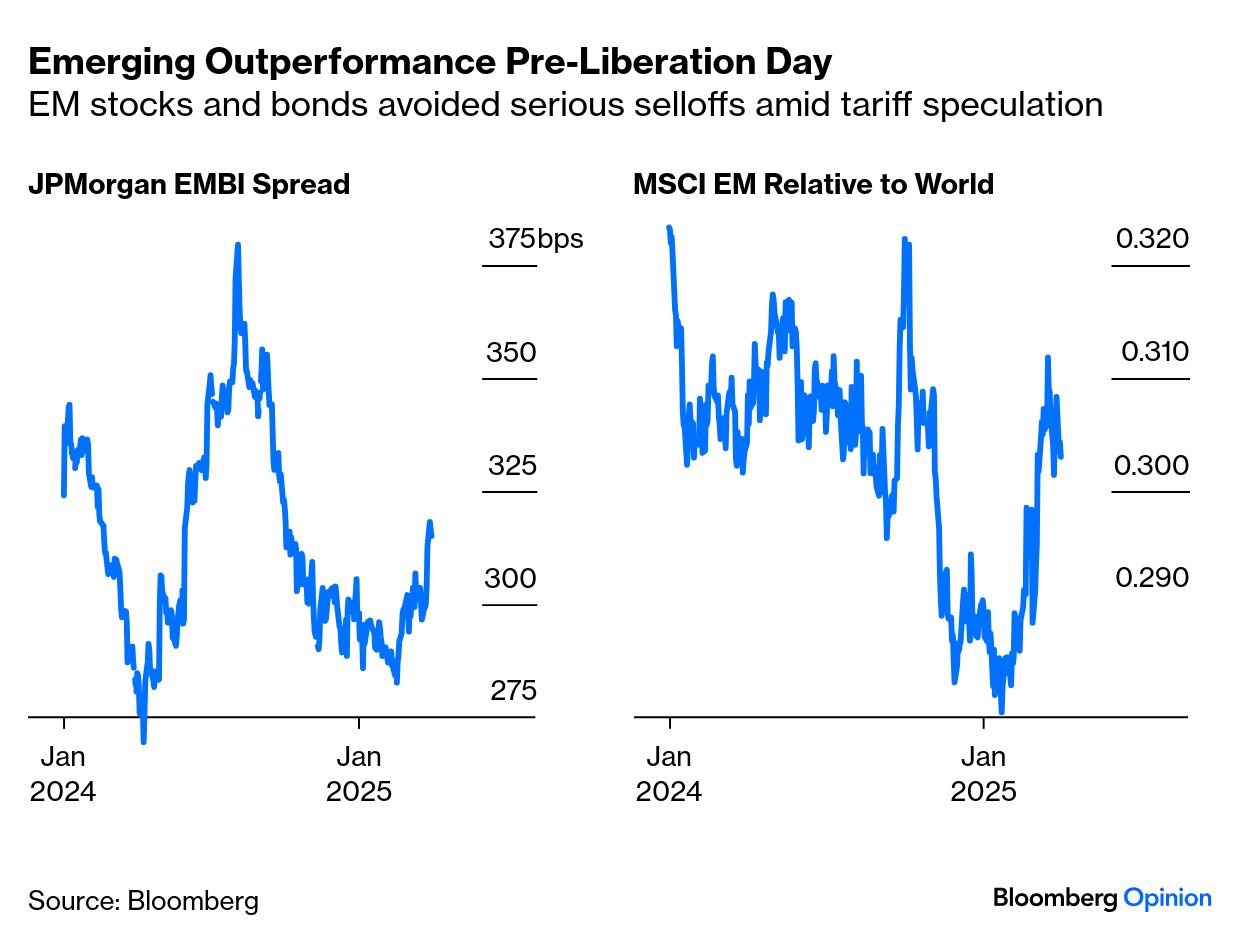

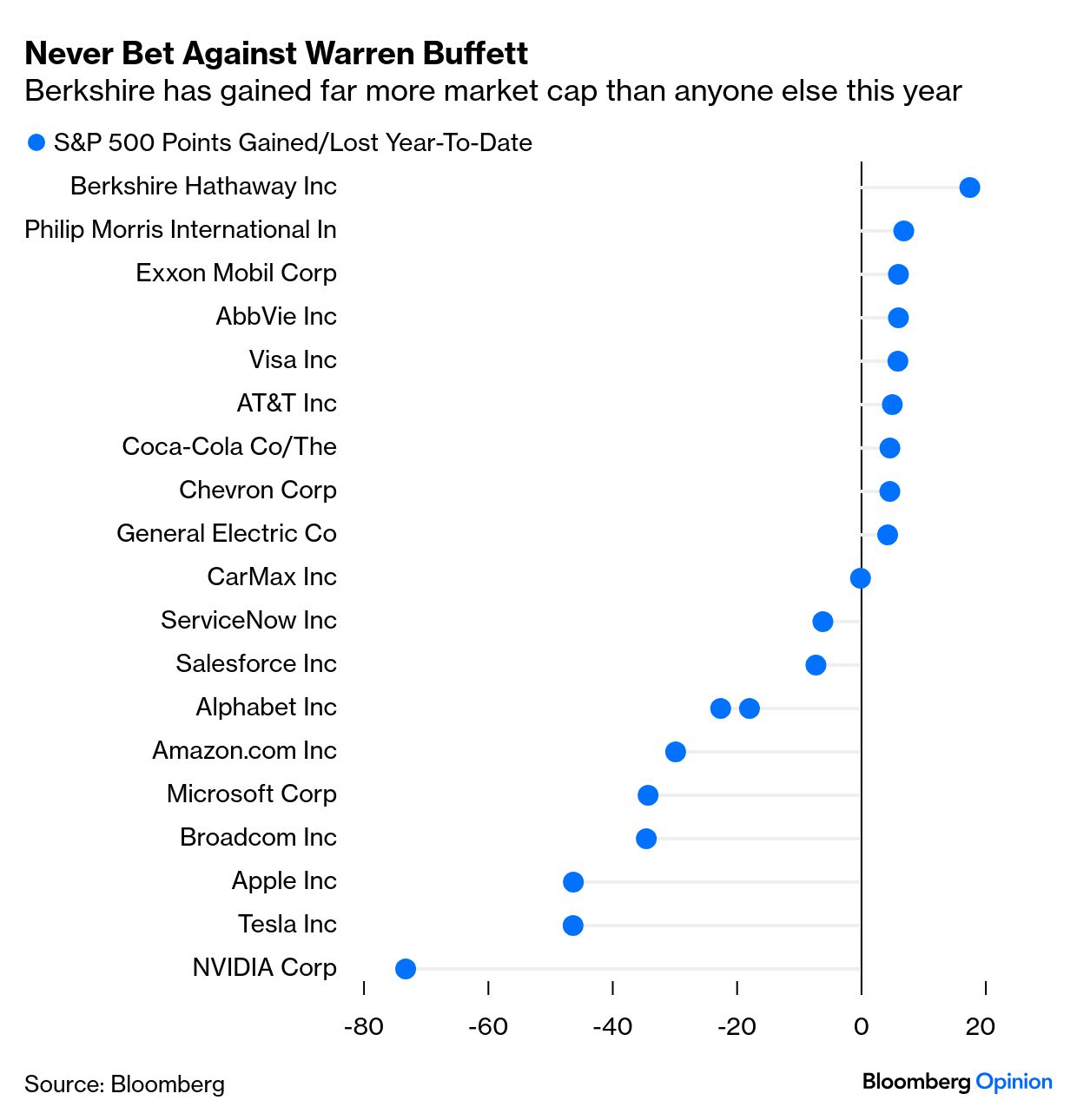

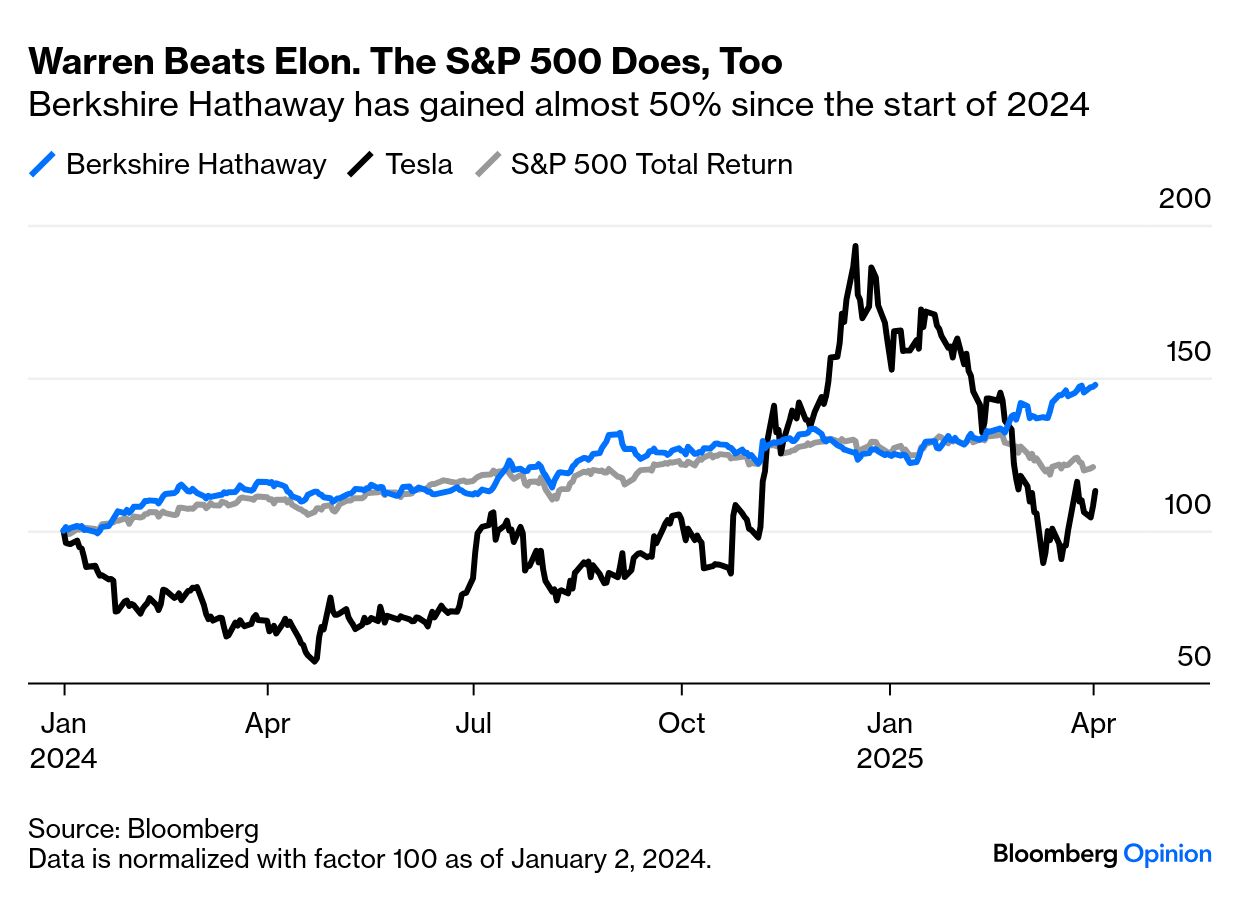

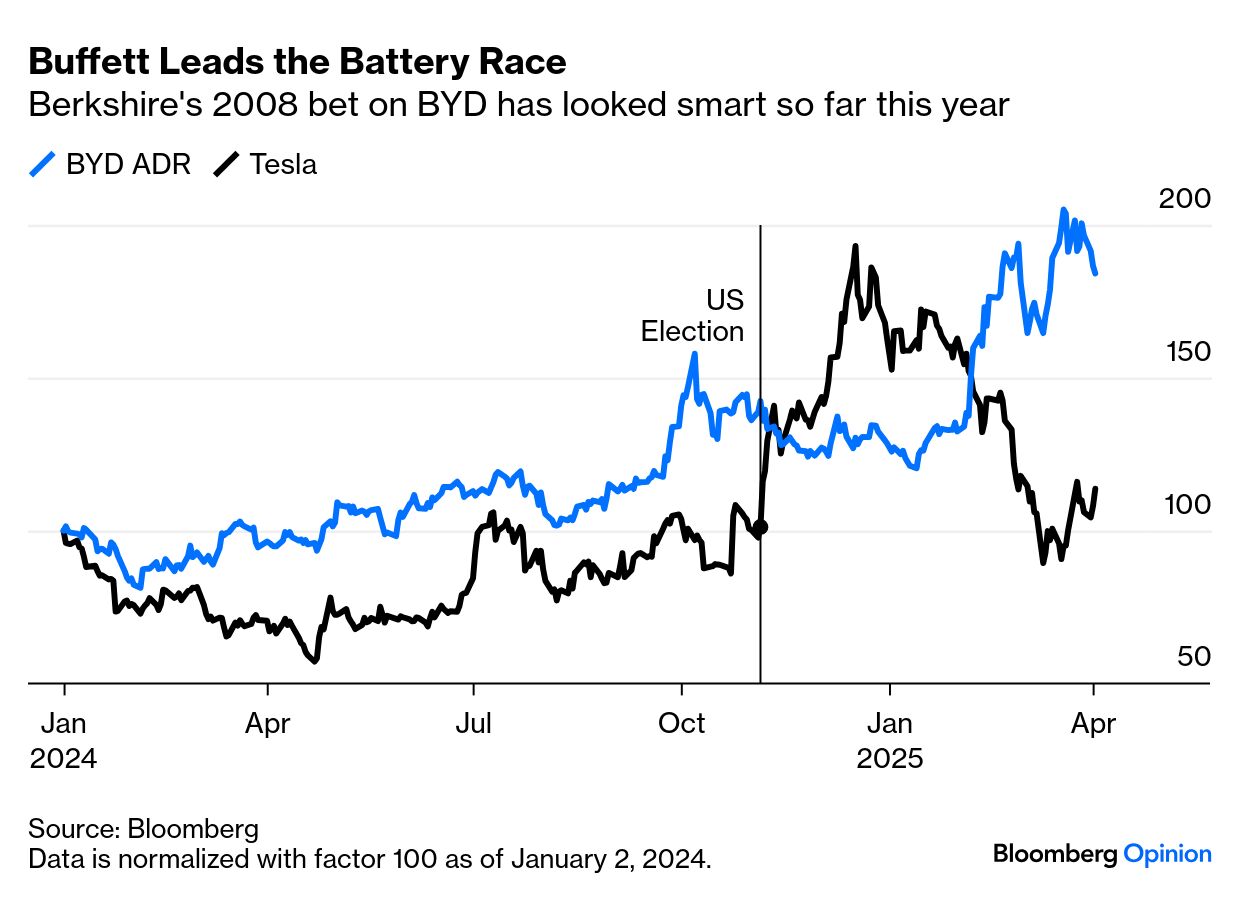

| Investors try not to wait for the news, if they can help it. The response to Liberation Day has been taking shape for at least a quarter, and reflects a strong bet on a change in leadership that took hold after the election. Investors are also getting their retaliation in first through a big stock rotation — although the scale of the tariffs may still come as a surprise. “Part of the pullback process is the churn involved in changing global leadership,” says Chris Watling of Longview Economics. “That is, the switch from portfolios dominated by growth stocks, to those with higher cyclical ownership (via defensive sectors).” Within the US, that turn has meant a move into large-cap value stocks, which enjoyed a spectacular first quarter — the best compared to growth, according to the Russell indexes, since the extreme conditions of the bursting dot-com bubble in 2001: Bank of America Corp’s Savita Subramanian suggested there was further upside for large-cap value stocks because they represent “quality and old economy cyclicals.” It’s noticeable that defensive stocks that do well in tough times also enjoyed a rotation in their favor: Also logically, US investors had already been exiting the stocks that were particularly dependent on overseas revenues, as illustrated by S&P indexes. If these tariffs stay in force for any significant period, we can expect this rotation to go a lot further: Emerging markets offer the greatest cause for concern; Asia’s, in particular, are the biggest losers from this package. And yet EM credit held up well in the months leading up to Liberation Day, and stocks outperformed. While there may be emerging cause for concern, there has been one very clear winner so far. Put together a market preference for old economy stocks deriving their income primarily from the US, and for value, and you get Warren Buffett’s vehicle Berkshire Hathaway. Indeed, its stock price has on its own raised the S&P 500 by 17 points so far this year, more than any other company. Nvidia Corp. had accounted for a loss of 70. These are the 10 greatest leaders and laggards for the year to date: Zeroing in on the contest between Berkshire and Tesla Inc., or old economy versus new, the turnaround is remarkable. Since the beginning of last year, Berkshire is up almost 50%. Tesla, judging by the after-hours move in its stock, is underwater: Buffett’s uncanny genius even spreads to an opportunistic acquisition he made in the turmoil of September 2008: a stake of roughly 10% in Chinese battery-maker BYD Co. That worked out well, even if Liberation Day will make life harder. And of late, Warren’s vehicle has even outpaced Elon’s: There’s a new order. The world has been turned upside down. Markets were (kind of, a bit) ready for it. And even at 94, it appears that we can still rely on Warren Buffett. |