De lande i Europa, der er mest afhængige af turismen, får det sværest efter coronakrisen, da al erfaring viser, at der går halvandet år fra en recession, før økonomien bliver genoprettet.

Uddrag fra ING:

Which eurozone countries are most vulnerable?

The health crisis in Spain and Italy is the most severe of all eurozone countries. What’s more, southern eurozone economies are especially vulnerable to the economic effects of such a shock. A stronger fiscal response could be necessary to limit the lasting damage

Lasting damage

The most important factor to judge the severity of this crisis is not necessarily the depth of the GDP decline but whether there is any lasting damage to the economy. The chances of a V-shaped recovery differ between eurozone countries because of factors such as company size, exposure to tourism, the share of vulnerable workers and the cushioning of automatic stabilisers.

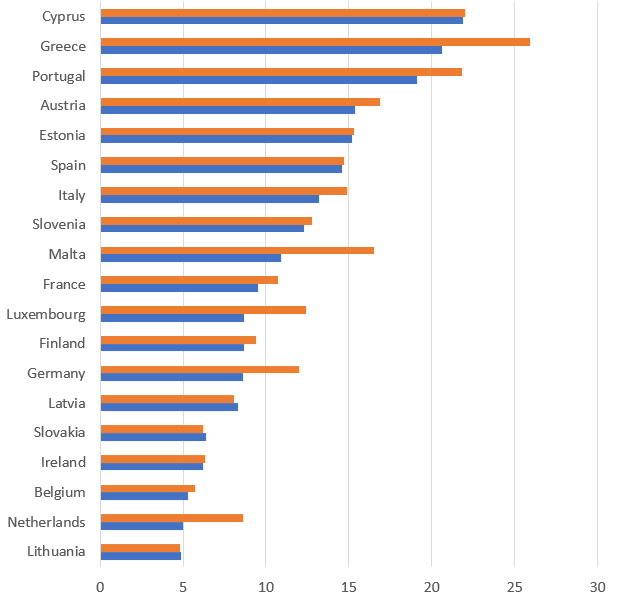

As the lockdown measures taken to counter the virus make it impossible to travel for leisure, the immediate growth impact will be larger for countries with a large tourism and travel sector. Tourism is particularly important in Italy and Spain, accounting for at least 13% of GDP and about 15% of total employment.

Within the eurozone, Cyprus, Greece and Portugal are the three countries with the largest tourism and travel sector. Even though the spread of the virus, at the moment, is relatively limited in these three countries, the growth impact will be large. As fear of travelling will probably last longer than the pandemic itself, it is difficult to expect an immediate recovery once the lockdown measures are lifted.

Research from the World Travel and Tourism Council shows that the average recovery time for visitor numbers to a destination after a major viral epidemic is about 19 months, which suggests that the recovery is unlikely to be V-shaped for the countries that heavily depend on tourism.

The importance of the tourism and travel sector in the eurozone

The labour market

The structure of the labour market can also make a country more vulnerable to the Covid-19 shock. Workers in the informal sector have no social protection and are more difficult to reach with targeted measures, while self-employed and temporary workers generally have lower social protection.

Moreover, a high share of temporary workers make the labour market more cycle-sensitive, meaning that a large number of people can become unemployed in recessions. Here too, Spain and Italy are among the countries that do not score well. These two countries are in the top four in terms of the share of self-employed and temporary workers.

The Spanish experience from the Great Recession gives reason to worry. The unemployment rate rose to 26% in 2013 partly due to the high share of temporary workers pre-crisis, and even though some labour market reform has taken place, temporary workers remain vulnerable.

A high share of vulnerable workers makes a country more sensitive to the Covid-19 shock

Company size and tax systems

Another interesting angle to judge the sensitivity of an economy to the Covid-19 shock is to look at the size of companies. Smaller companies generally have limited financial, managerial and technological resources. It is, for example, more difficult for small firms to respond to the crisis with technological solutions such as telework.

Academic research shows that smaller and younger enterprises are more vulnerable to exogenous shocks. Here too, southern countries are in a bad position as they have a high share of small companies.

The impact of an economic shock is also dependent on the fiscal system. Tax and benefit systems cushion economic shocks, on average about 35% of the impact on household incomes is absorbed by the tax and benefit system in the EU, according to the European Commission.

This differs a lot by country though. Austria sees 45% of an income shock absorbed by automatic stabilisers, closely followed by Ireland, Luxembourg, Finland and Germany. At the bottom of the list ranks Estonia, Spain and Malta, but also Greece and Slovakia have a shock absorption of under 30%. Italy ranks just above that, also below average. This indicates that the social safety net in most northern economies is more developed than in the southern economies, adding to the vulnerability.

South more vulnerable than the north

Southern eurozone economies seem to be more vulnerable to this economic shock than the northern member states. The larger exposure to tourism, smaller automatic stabilisers, larger share of vulnerable workers and higher chance of bankruptcies due to firm size all contribute to an uneven recovery once the virus retreats and restrictive measures are lifted.