ING analyserer de seneste bestræbelser fra den tyrkiske centralbank og bankmyndighederne for at standse den dramatiske nedtur i økonomien, på aktiemarkedet og i valutaen, der er blevet halveret over de seneste få år. En vending er måske på vej. Udenlandsk kapital strømmer atter til Tyrkiet, der tidligere har været et stærkt investormarked.

Turkey’s current account deficit widens again in September

Despite efforts by the central bank and the banking regulation and supervision agency to normalise things since August, the current account balance continues to deteriorate on the back of widening trade deficit and a fall in services income

Better than the consensus, Turkey’s current account deficit in September turned out to be US$2.4 bn.

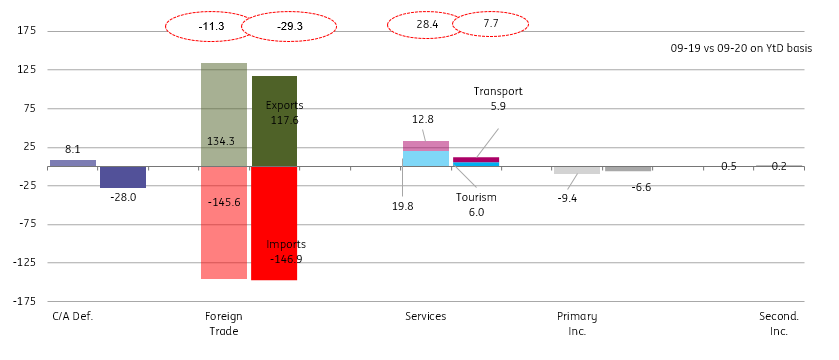

In the first nine months of the year, the cumulative figure has been widening at a rapid pace and reached US$28 bn. Based on the monthly data, continuing deterioration in the services balance is due to contraction in transport and tourism revenues and in the goods balance due to high gold imports are the drivers.

The worsening in the first nine months is down to the deterioration in core and gold deficits in the goods balance and plunge in services balance with the breakout of Covid-19.

Breakdown of current account (US$ bn, YtD)

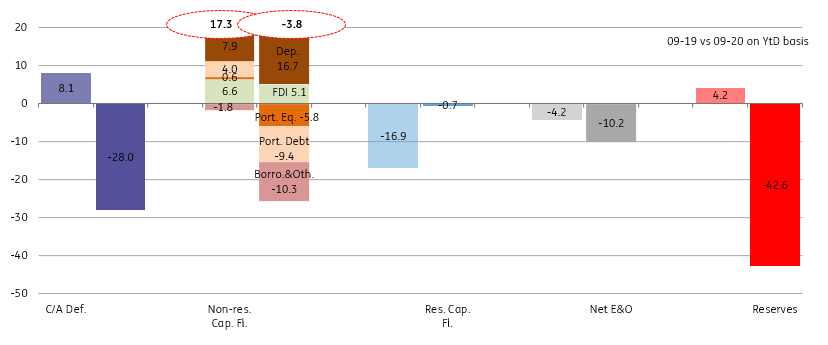

The capital account recorded another negative reading in September given residents’ outflows standing at US$4.5 bn, despite non-resident inflows around US$3.3 bn. With the current account deficit and marginally negative net errors and omissions, reserves recorded another large depletion at US$3.6 bn (US$42.6 bn on a year-to-date basis).

- Regarding the non-resident flows, the key debt creating items witnessed US$3.3 bn inflows and offset a large portion of the impact from residents moves.

- These inflows were attributable 1) trade credits rising by US$2.7 bn 2) portfolio investments in the local debt at US$0.5 bn 3) banks’ US$0.8 bn net borrowing (positive in the long-term for the first time since Nov-19).

- Accordingly, in September alone, the long-term rollover ratio for banks was at 123% vs 60% for corporates. On 12M rolling basis, banks’ rollover ratio has maintained improving to 83% vs 63% for corporates. This shows that the pace of deleveraging is relatively higher in the corporate sector while banks’ net borrowing has been increasing in comparison to the last year.

- On the flip side, net borrowing for the corporate sector was negative at US$0.4 bn, due to long-term credit payments, while deposits of foreign banks at the local banking system dropped by US$1.0 bn despite some inflows to foreign deposits at the Central Bank by US$0.3 bn.

- Non-debt creating flows, gross foreign direct investment flows stood at US$0.9 bn while outflows from the equity market turned out to be US$0.3 bn.

Breakdown of capital account (US$ bn, YtD)

Overall, despite normalisation efforts by the central bank and the banking regulation and supervision agency since August, the current account continues to deteriorate on the back of a widening trade deficit and fall in services income.

The deficit is mostly due to the net gold trade which is another indicator of locals’ changing portolio preferences to more safe assets, though core deficit exlucindg gold and energy is also widening given high core imports requiring further normalisation moves by policymakers.

On the capital account, subdued capital flows point to continuing challenges on the external outlook this year. This shows that rollover ratios and portfolio flows should improve to avoid further reserve losses.