ING har lavet en analyse, der vil give genlyd: Trods bedre produktivitet vil vi fortsat have lav vækst i Europa, fordi arbejdskraften ældes!

Uddrag fra ING:

The new decade: Why productivity growth won’t save us

Eurozone trend growth has declined strongly over the last decade and this is unlikely to change in the 2020s. The main culprit is ageing, which is a double whammy to growth. It not only reduces the growth of the labour force, but is also one of the drivers of the decline in productivity growth, a negative effect that is often overlooked

Over the last decade, western economies, particularly within the eurozone, have been characterised by unusually slow growth, a phenomenon known as secular stagnation.

Europe is now confronted with a slowdown in labour force growth at a time when productivity growth has been dwindling, leading to a decline in potential economic growth. A recent study showed that over the period 2006 to 2014, productivity growth fell short of compensating for the negative impact of ageing on per capita GDP growth in nearly half of the OECD regions.

Demographic trends are relatively easy to forecast. We know that in the eurozone the growth of the working age population has been decelerating over the last decade and will fall by 3.8% in the next 10 years. It is therefore key for stronger productivity growth to compensate for the decline in the labour force. Large changes in productivity growth trends are unfortunately much harder to predict than demographics as they rely on factors like technological change and adoption of new technologies throughout the economy. Productivity growth has been falling in recent decades and the reasons for this have been the focus of much research. Some point to the disappointing pickup of digitalisation in the economy while others look to the impact of low interest rates and banking. But the root cause of the weak productivity trend over past decades can also be found in demographics.

The impact of the ageing population on productivity

Intuitively, you would think that productivity increases with experience but starts to level off at a certain age, when people become less flexible in adopting innovation. However, these generalisations might hide very different trends across sectors. It is obvious that in physically demanding professions like construction, productivity might start to fall at a relatively early age while in other professions, experience could contribute more strongly to growing productivity. Therefore it is not easy to extrapolate micro economic observations to the macro level. That said, empirical research shows that, on average, productivity tends to increase until workers are in their forties and starts to decrease later in their working career. This brings about the idea that the changing age composition of the workforce might indeed have an impact on macro-economic productivity growth. A population where the majority of workers are past their prime working age could act as a drag on overall productivity.

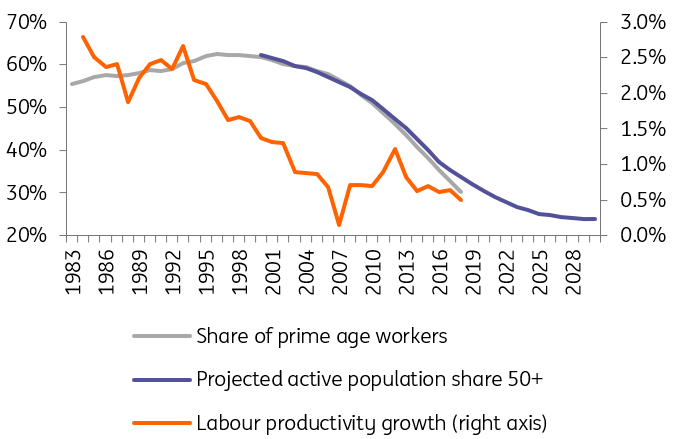

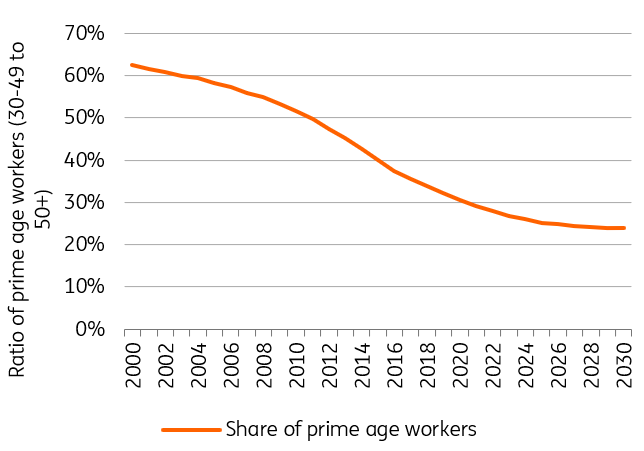

An ageing population acts as a double whammy for potential growth in the eurozone. Various studies have found links between the relative importance of different age cohorts and productivity, all pointing to a positive relationship between a large group of “prime age workers” and productivity growth. A recent study by the IMF finds that a larger share of prime workers in total employment has a positive effect on productivity growth. As the share of prime age workers has been declining (for which we use a ratio of 30-49 to 50+), this has, in part, explained the declining productivity growth.

What can be expected in the coming decade?

We have used the International Labour Organization’s participation rate projections by cohort and Eurostat’s population projections to estimate the future share of prime age workers in the active population (note that we do not take employment estimates but estimates of active population, which also include the unemployed as it is beyond the scope of this piece to make cyclical assumptions for the coming decade). With that, we have a proxy for prime age employment (which we define as the ratio between people employed aged 30-49 and 50+) in the 2020s. While the share of prime age workers will not decline as quickly as it has over the course of the past decade, it will still decline. This means that there will be continued downward pressure on productivity growth coming from the labour market’s composition. To be sure, productivity growth is unlikely to decelerate at the same pace as it has over the last few decades, but the ageing workforce certainly won’t help in the new decade.

The share of prime age workers is set to decline

Source: Eurostat, ILOstat, ING Research

Between countries, differences are significant. The ones with a high share of workers above 50 include Germany (although the share starts to decline from 2022 onwards) as well as Italy, Spain and Portugal. In the Netherlands, France and Belgium, the impact on productivity growth from the labour market will be better than average. This means that with the exception of Germany, the divergence between the core and periphery countries could remain a theme in the 2020s, as potential productivity growth for the core economies seems better than that of the periphery. It’s not just demographic factors that separate the north from the south. The two regions also differ in terms of their digital performance, investment, company size and institutional framework, with the core economies more likely to outperform their periphery neighbours in terms of productivity growth.

The lower share of prime age workers puts pressure on productivity growth in the decade ahead

Source: OECD, BCL database, Eurostat, ILOstat, ING Research