As the ECB’s “ambitious roadmap” still lacks detail, we don’t expect it to have major performance implications yet. However, once the central bank’s ambitions take further shape in the next few years, they will unquestionably become a factor of significance to the bond market. Within the corporate bond sector, we still expect to see high carbon-intensive debt underperform, potentially similar to what we saw happen to the tobacco industry after it was stigmatised for its negative health effects some 10-15 years ago.

The ECB’s plan to further integrate climate change considerations into its policy framework form one plank of the central bank’s strategy review, which started in January 2020. (See our research preview, The greening of monetary policy. The Bank aims to use a set of measures over a period of four years, at most, which are designed to be consistent with its objective of price stability. This means that the ‘greening’ of policy will come via its role as bank supervisor rather than through monetary policy.

It’s important to note that at this stage, the ECB has only laid out its ambitions; there are no concrete proposals as of yet. While the ECB has underscored its determination to make its collateral framework and asset purchases greener, actual proposals on this are not expected to be published before next year. As such, any major performance implications should not be expected until the details become clearer.

Furthermore, while the intended greening of the monetary policy framework involves the central bank’s Asset Purchase Programme and collateral framework, the roadmap makes no mention of the potential greening of Targeted Longer-Term Refinancing Operations. In September last year, ECB President Christine Lagarde confirmed that ‘green’ TLTROs would be considered by the central bank as part of its strategy review. In the coming years, as banks are better able to measure the taxonomy alignment of their assets, this may be a topic that could become part of the discussion again.

We would also highlight that the incorporation of climate change risks is focused on the Corporate Sector Purchase Programme (CSPP). The Public Sector Purchase Programme (PSPP), Covered Bond Purchase Programme (CBPP3) and Asset-Backed Securities Purchase Programme (ABSPP) are not explicitly mentioned in the roadmap. For the CBPP3 and ABSPP, this may be related to the fact that banks are not major direct emitters of greenhouse gasses themselves, while green bonds only make up a small portion of these markets.

Green bonds also have a small share in the eurozone public sector bond market. And central bank buying of sovereign bonds is mostly driven by the capital key. EU regulations supporting transparency and data-availability on the climate-related footprint of issuers are, at this stage, primarily designed for large and listed companies (NFRD/CSRD) or financial market participants/financial advisers (SFDR), not for sovereigns. This, in our view, may explain why the ECB’s roadmap is biased towards private sector assets, both for the collateral framework and asset purchase purposes.

Corporate Sector Asset Purchases

The ECB has already been pushing its agenda for climate change, for example, by increasing and concentrating ESG asset purchases in both its Asset Purchase Programme and the Pandemic Emergency Purchase Programme. As it stands, the ECB holds 170 ESG corporate bonds, purchased under CSPP and PEPP. This accounts for 10% of the total corporate debt purchased by the ECB – a substantial chunk of the eligible ESG market. Of these 170 bonds, 104 of them were purchased after November 2019, accounting for 14% of the total purchases since then.

This is indeed a substantial amount considering that demand for ESG debt has been so strong and supply has not really kept pace with this. One catalyst for growth in the ESG market has been the Covid-19 pandemic, which we discuss in our report, Covid the catalyst for ESG in credit.

The ECB has already included a provision in its guidelines for step-up bonds which are, in principle, ineligible as collateral, making the bonds eligible if they are tied to ESG targets. As a result, sustainability linked bonds (SLBs) have become eligible as collateral and for the ECB to purchase. In its roadmap, the central bank stresses that it will remain supportive of financial innovations such as SLBs.

Looking forward

The ECB will adjust the framework for the allocation of corporate bond purchases to incorporate climate change criteria. This will include:

- the alignment of issuers with EU legislation implementing the Paris agreement through climate change-related metrics or,

- commitments of the issuers to such goals.

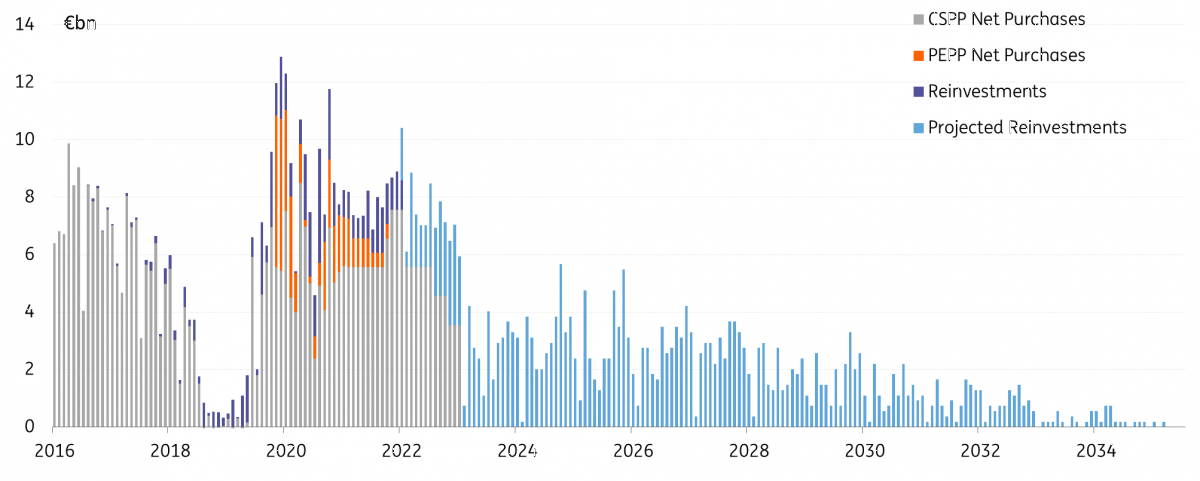

The ECB will develop proposals to adapt the CSPP framework to include climate change considerations between now and mid-2022. Thereafter, the changes will be implemented. The ECB has stated it will continue its net purchases under the APP until shortly before it starts raising rates. Our economists believe this will likely occur in late 2023 to early 2024. In which case, we can assume the ECB will continue actively purchasing up until around mid-2023. From that point onwards, the ECB will continue its reinvestments, which we expect to be around €2.5-3bn per month.

Actual & Projected CSPP, PEPP and reinvestments

Monthly net purchases and reinvestments of CSPP and corporate purchases under PEPP, alongside reinvestments

The ECB still has to nail down specifics on the sustainable allocation criteria under the CSPP. There may also be a transition period for issuers to align themselves with the new criteria in order to remain eligible. Therefore, there will not be any effect on credit spreads as of yet.