Resume af teksten:

Nyheden om en våbenhvile mellem USA og Iran har styrket den kinesiske yuan (CNY), hvilket har ført til en revidering af prognosebåndet til 6,70-7,05. Yuans værdi er steget med mere end 2% i år sammenlignet med den amerikanske dollar. Yuanen har overgået de fleste andre asiatiske valutaer i denne periode, især siden krigsudbruddet i Iran. PBoC viser at der ikke er modstand mod en gradvis styrkelse af yuanen. Faktorer, der understøtter denne styrkelse, inkluderer positive markedsforventninger og en stærk handelsbalance. Irans planer om at opkræve betalinger i yuan for passage af Hormuzstrædet har også øget forventningerne til den langsigtede værdi af yuanen. Prognosebåndet for USD/CNY er derfor nedjusteret til 6,70-7,05.

Fra ING:

News of a US-Iran ceasefire has pushed the Chinese yuan higher, breaking through our previous forecast band and prompting an update. We’re setting the new forecast band at 6.70-7.05, formerly our bullish scenario for the CNY this year

China’s yuan has risen more than 2% against the dollar this year

Our updated 2026 USD/CNY fluctuation band

Adjusted lower amid continued bullish factors for the yuan

CNY has outperformed most currencies vis-a-vis the dollar this year

The Chinese yuan has tended to fall in the middle of the pack in terms of its performance versus the US dollar in the past few years, as the currency stability objective of the People’s Bank of China has led to very limited movement in the yuan.

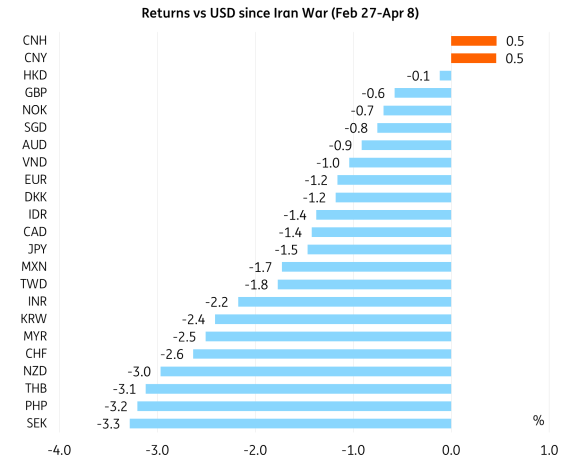

This has changed so far in 2026. Year-to-date, the CNY has actually been one of the notable outperformers against the USD, up 2.3%, easily outperforming most other Asian currencies on the year. Since the outbreak of the Iran war to the time of writing, the yuan (CNY) and the offshore yuan (CNH) are the only currencies in our tracked basket that have actually gained against the USD.

So what’s the story behind this surprising outperformance?

First, the market’s bullish sentiment has carried forward. We wrote about the building bullish sentiment in the last update of this report in January. In our conversations with a wide range of market participants, we note that this bullish sentiment on the CNY remains intact and seemingly quite widespread.

Second, policymakers appear content to allow for further CNY strengthening. There was some question about this when policymakers cut the foreign exchange risk reserve ratio from 20% to 0% in what was an apparent attempt to halt the pace of CNY appreciation. However, after the outbreak of the Iran war, and the immediate spike in oil prices, there appeared to be a change of heart, as the PBoC’s daily fixings suggested a tolerance for further appreciation.

Third, macro level drivers continue to suggest room for further appreciation of the CNY versus the USD if the situation in the Middle East is brought under control. China’s exports are off to another strong start this year, suggesting that the current account surplus is going to remain a positive factor for the yuan. Meanwhile, the currency has largely weathered the widening US–China yield spread, which should resume its narrowing trend if inflation expectations come under control. That is far from guaranteed. Since the outbreak of the war, two dominant narratives have emerged: warnings from experts that markets may be underestimating the impact, and a widely held expectation among investors of a TACO (‘Trump always chickens out’) scenario and eventual normalisation.

Fourth, the CNY has been a surprising winner of the Iran war, despite China’s role as the largest oil importer in the world. At least a few market participants have mentioned re-evaluating the “China risk premium” amid rising global uncertainty elsewhere, which has led to China looking more and more like the adult in the room. While the actual direct impact has been tangential at best, discussions of the potential damage to the petrodollar system and rise of the petroyuan – aided by Iran’s plans to collect a fee for passage through the Strait of Hormuz to be collected in CNY or cryptocurrency – may have also added to longer term bullish expectations for the CNY.

CNY and CNH have been the surprising outperformers since the Iran war broke out

Source: Bloomberg, ING

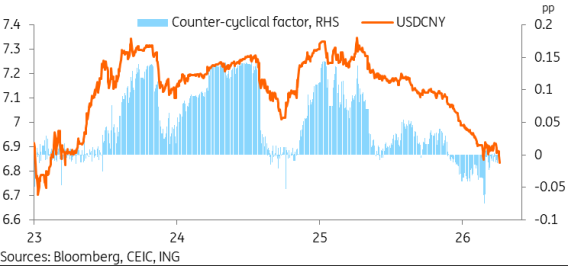

PBoC fixings suggest no opposition to gradual appreciation

In this report series, we’ve often talked about the PBoC’s currency stability objective as one of the key deciding factors for the trajectory of the USD/CNY. The PBoC has exerted its influence on the currency primarily through its daily fixings. The counter-cyclical factor, which is the adjustment it makes to the daily fixing versus the previous day’s market closing price, has been heavily relied on to curb excessive movements of the USD/CNY during periods of heavy market speculation. In the last few years, this has mostly been used to push back against heavy depreciation pressure. Towards the end of 2025, however, this pattern started to reverse, with the PBoC using fixings to push back more cautiously against appreciation.

The PBoC’s counter-cyclical factor has been very close to neutral for most of March and the start of April, after leaning more forcefully against rapid appreciation in previous months. This has sent a signal that policymakers are open to the CNY continuing to strengthen, and remains one of the main factors supporting CNY appreciation. This was a little surprising as the counter-cyclical factor and the cutting of the foreign exchange risk reserve ratio from 20% to 0% had appeared to signal an effort to rein in CNY appreciation back in February.

The outbreak of the war in Iran looks to be the reason for the renewed embrace of a stronger CNY. China remains the world’s largest oil importer, and while a slight appreciation of the CNY certainly won’t offset the surge in oil prices, it can at least help mitigate the potential pain. Other factors may include the senior-level comments on attempting to balance trade and ramp up imports, to which a strong CNY would also contribute. Furthermore, it is possible that higher inflationary pressure and uncertainty from the war will delay potential PBoC rate cuts; as a result, we have pushed our forecasts back from 2Q26 to the second half of the year. Even though PBoC cuts tend to be modest, a delayed rate cut is nonetheless a positive factor for CNY appreciation.

Counter-cyclical factor has been mostly neutral compared to previous years

CNY has shrugged off a sharp widening of yield spreads

US-China yield spreads have been a major driver of the USD/CNY’s trajectory over the past few years. Higher US yields have been a key reason why Chinese exporters have kept a large share of their proceeds offshore, contributing to CNY weakness in recent years. However, as the Federal Reserve resumed its rate‑cutting cycle, the yield spread began a more predictable narrowing trend from early 2025 through early 2026.

The Iran war has quickly derailed this story, as US yields moved higher while Chinese yields edged a little lower. Over recent weeks, the two‑year US–China yield spread widened to its highest level since February 2025. Yet this translated into only a modest softening of the CNY over the same period, and by the time of writing, renewed prospects for peace have led markets to largely shrug off the wider yield spread entirely.

There’s still a relatively high level of uncertainty on this front, mostly from the US side of the equation. If inflation remains under control, and the Fed eventually resumes rate cuts after a few pauses, we’ll likely see a return of the narrowing yield spread story, which will further fuel CNY appreciation expectations. This is one of the reasons why the CNY has strengthened considerably on today’s news of a two-week ceasefire.

However, if we move into a longer rate hold, or worse, a Fed rate hike environment where the yield spread stays elevated, the bullish case for the CNY begins to look weaker. This is a potential outcome of a longer war scenario, and remains worth monitoring.

CNY has continued to appreciate despite spike in yield spreads

CNY’s recent outperformance across the board may not hold if peace is successful

We wrote earlier about the CNY’s surprising outperformance against the USD since the start of the Iran war, beating the other currencies in our monitored basket.

As such, it should come as no surprise that the CFETS RMB index, which heavily weights the euro (17.9%), Korean won (8.5%), and Japanese yen (8.1%) alongside the US dollar (18.3%) has also strengthened noticeably in the same period. This index is up 2.3% since the start of the Iran war, and 2.9% year-to-date.

While we are still optimistic about the CNY’s prospects against the USD, the performance versus other pairs could lag behind by comparison. Other currencies, which have generally fared poorly after the Iran war, could bounce back more strongly, limiting the CNY’s relative scope for further appreciation. As such, the CFETS RMB index could underperform versus the USD if we see a scenario where the peace holds and the strong dollar backdrop fades.

CFETS RMB index has also outperformed in the recent strong dollar environment

Current account shows no sign of letting up so far in 2026

China has been running an especially strong current account surplus in the last couple of years, as external demand has been resilient despite the trade war. Despite facing a largely unfavourable base effect, China’s trade growth appears to be off to another strong start this year. While imports look likely to rebound as well this year, China’s trade surplus will remain very significant.

This is relevant for the CNY as the currency has shown clear historical correlation with the current account, as exporters tended to remit proceeds back into the CNY. This relationship appears to have broken down in recent years. While the current account balance has risen sharply, USD/CNY has remained largely range‑bound. This reflects exporters holding a greater share of foreign‑currency proceeds due to more attractive yields abroad relative to China, as well as generally subdued domestic investment appetite – underscored by the fact that 2025 marked the first year on record in which fixed‑asset investment contracted on an annual basis since data publication began.

What does this mean for the CNY? Assuming that exporters eventually begin to convert holdings back to the CNY – either to meet domestic obligations or as yield spreads narrow – this would translate into a lot of pent-up demand for the CNY. We have already observed this to be a factor during the CNY’s rally to date, but considering the current levels for the CNY and the current account balance, it could be argued there’s still plenty of room to go.

Current account balance suggests more strength for CNY ahead

Rise of the ‘petroyuan’ remains a long-term theme rather than a short-term catalyst

Iran’s potential move to turn the Strait of Hormuz into a tolled passageway – requiring payments in cryptocurrency or CNY – has sparked lively debate about what this could mean for the yuan’s future. This includes renewed interest in the so‑called ‘petroyuan’, perhaps last discussed prominently near the start of the Russia–Ukraine war, when sanctions on Russia resulted in much of the country’s oil trade with China moving to the CNY.

One interesting argument was that, if the Iran war were to end with Iran successfully controlling the Strait of Hormuz, this could lead to a system in which payments for passage are collected in CNY, and eventually to oil trade flows through the Strait and into Asia being denominated in CNY. In this scenario, the Iran war would be seen as dealing a major blow to the petrodollar system, with the CNY emerging as a key beneficiary amid an acceleration towards a ‘petroyuan’ system, and the world taking another step towards a more multipolar order.

It’s not surprising why this topic has garnered interest and discussion. However, there are a few logical leaps that appear to occur here; it’s assumed that the trade going through the Strait would be priced in CNY, rather than just the fee for passage. This would require the cooperation of all of the Gulf states, and there hasn’t been anything to indicate that such a shift is currently in the works. It also assumes that Iran permanently assumes control of the Strait, and passing ships willingly pay the fees.

In the near term, the impact is likely to be very incremental. After all, there is not a strong level of clarity on Iran’s criteria for letting ships through the Strait of Hormuz, with only a small number of tankers currently permitted to transit. Among those ships that have secured passage, it is unclear whether or not a toll was paid, and whether the payments were made in CNY or other currencies.

In a thought exercise where we take the most optimistic assumptions, where traffic to the Strait of Hormuz is fully restored to around 100 vessels a day or 36k vessels a year, and that every single vessel that passed through the Strait ended up paying a USD 2mn equivalent fee in CNY, we’d still only get a somewhat paltry USD 72bn or RMB 491bn.

In a vacuum, this increases CNY demand and global usage. But how significant is that in the grand scale of things? Considering that China’s Crossborder International Payments System (CIPS) handled around RMB 180tn of payments in 2025, an extra RMB 491bn wouldn’t be negligible but far from a gamechanger.

Nonetheless, the fact that the CNY was requested as a payment currency certainly is something interesting to watch. It is a real-world example of the CNY’s rising clout and a vote of support for China acting as a counterweight to the US-dominated financial system.

CNY’s continued outperformance pushes us into the bullish forecast band

We are moving on from the previous baseline forecast fluctuation band of 6.85-7.25 for the USD/CNY, and lowering the new forecast fluctuation band to what was formerly our bullish scenario forecast of 6.70-7.05. We lower the year-end USD/CNY forecast to 6.75.

The CNY has performed stronger than expected after policymakers ended the pushback against appreciation, and has largely shrugged off a strong dollar environment and elevated global uncertainty to continue its appreciation trajectory.

Risks to the band look roughly balanced at this point. Bullish factors remain in place, but markets also look largely positioned for this already, and it would still be a little surprising to see the PBoC tolerate the CNY strengthening past 6.70 this year; recall that the 6.70 level was basically the strongest for the CNY since currency stabilisation became a more prominent theme back in 2023. On the other hand, a bearish reversal past the top end of the band would likely require new catalysts such as a substantially more hawkish global central bank environment widening China’s yield spreads versus other countries, or a renewed pessimism setting in on China’s growth. These are certainly possible if we see a strong inflationary impact from the war in Iran, or if China’s efforts to bolster domestic demand fall short.

Forecast band shifted lower as CNY continues to outperform

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.