Resume af teksten:

Næste uge byder på flere vigtige økonomiske beslutninger og dataudgivelser i Asien. Kina, Indonesien og Filippinerne vil afsløre deres beslutninger om renteniveauer. Japans inflation og indkøbschefindeksdata samt Sydkoreas BNP-tal vil også blive offentliggjort. Ingen ændring forventes i Kinas låne-primerenter, trods reflation og en indsnævring af handelsoverskuddet. Filippinernes centralbank forventes at holde renterne stabile på trods af svagere vækst. Indonesien antages ligeledes at fastholde nuværende rentesats. Sydkoreas BNP ventes at vokse med 1,0 % i første kvartal, hvor chip-eksport bidrager væsentligt. Japans eksport forventes at stige, mens inflationen forbliver moderat og under 2 %.

Fra ING:

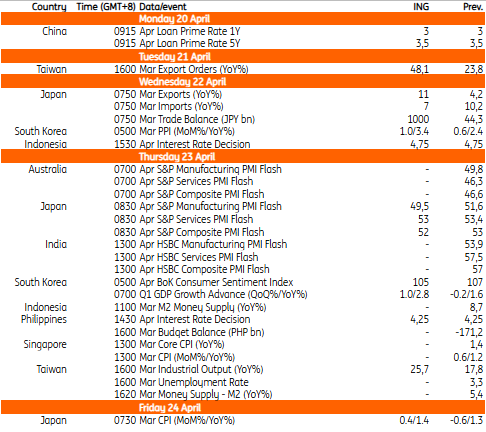

China, Indonesia and the Philippines will announce interest rate decisions. Key data releases include Japan’s inflation and purchasing managers’ index data, and South Korea’s GDP

Asia Research highlights of the week

China’s growth faces pressure from reflation and a narrowing trade surplus Energy shocks in Asia: diverging buffers, diverging growth South Korea’s solid export growth is offsetting weak domestic demand Singapore’s central bank tightens policy as inflation risks rise China’s trade surplus plummets as exports slow and imports surge

China: No change expected to loan prime rates

China’s loan prime rates will be set on Monday; no change is expected. Stronger-than-expected first-quarter GDP data, combined with the recent reflationary trends, may keep the People’s Bank of China on hold until conditions warrant monetary policy support.

Taiwan: Strength expected in upcoming output data

Taiwan releases its export orders on Tuesday. We expect orders to rebound to 48.1% year-on-year in March. Industrial production data will be released on Friday, when we’re looking for a rebound to 25.7% YoY.

Philippines: BSP to hold rates amid weaker growth

The Philippines remains one of the most oil‑exposed economies in the region, prompting us to downgrade our 2026 GDP growth forecast to 4.5%. Against this weaker growth backdrop—and assuming the current geopolitical escalation eases in the near term—our base case is for the central bank to remain on hold in April. However, Thursday’s decision is likely to be close. CPI inflation rose above Bangko Sentral ng Pilipinas’ target, and policymakers have consistently emphasised inflation stability as the primary anchor of its monetary policy framework.

Indonesia: BI to keep rates steady

While Indonesia’s fuel subsidies continue to cap the pass-through from higher oil prices, inflation is still expected to exceed Bank Indonesia’s 2.5% target. At around 3.5%, CPI would remain well below the 2022 peak of about 5% that triggered aggressive rate hikes. With growth softening, BI is unlikely to hike rates. It’s expected to remain on hold on Wednesday.

South Korea: GDP to show growth amid robust chip exports

South Korea’s first quarter GDP is expected to rise by 1.0% quarter-on-quarter, seasonally-adjusted, following a -0.2% contraction in the fourth quarter of 2025. Robust exports, mostly driven by chips, should be the main driver of growth. The oil disruptions should have a limited impact on trade and manufacturing activity, at least in the January-March period. Household and government spending are expected to rise modestly amid the healthy first two months of data. For investment, facility investment should rebound thanks to expansion in chip production lines, while construction investment remains sluggish.

Japan: Strong growth and modest inflation expected

In line with trends observed in other major Asian countries, we anticipate strong Japanese export growth in March. Oil supply constraints are unlikely to pose any significant drag before the end of March, while continued strong external demand for semiconductors and IT products should further bolster export performance. The Flash PMI is projected to decline, particularly as manufacturing figures fall below 50. The ongoing conflict in the Middle East may increase pressure on several manufacturers. However, the service PMI is likely to remain positive. CPI inflation is forecast to remain largely unaffected by elevated global energy prices during March. Government efforts to stabilise gasoline prices should limit the monthly increase to only a modest rise. Both headline and core inflation rates are expected to remain below 2%.

Key events in Asia next week

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.