Resume af teksten:

Ungarns vælgere gav Tisza-partiet en to tredjedeles flertal ved valget, hvilket afsluttede Fidesz-partiets 16-årige dominans. De officielle resultater er endnu ikke på plads, men Tisza forventes at have vundet 138 af 199 pladser. Orbán-regeringen fungerer som en midlertidig regering, indtil den nye regering dannes inden 13. maj. En særlig lovlig ordning er gældende på grund af krigen i Ukraine. Økonomisk set kan der forventes ændringer, men det nuværende økonomiske pres kan påvirke kortsigtede resultater. Markedet forventer, at relationerne til EU forbedres, men det kan tage tid at genoprette tilliden. Den nye regering skal håndtere budgetudfordringer og overveje euro-vedtagelse. Valutamarkedet har reageret positivt på oppositionens sejr, selvom globale usikkerhedsfaktorer kan påvirke udviklingen.

Fra ING:

Following a record-high turnout, Hungarian voters handed power to the Tisza Party. This comfortable two-thirds majority victory paves the way for a smoother and faster political and economic transition. However, the country’s economic structure and its dependencies will limit the short-term impact on the real economy

Peter Magyar addresses supporters after his party wins a landslide in Hungary’s elections

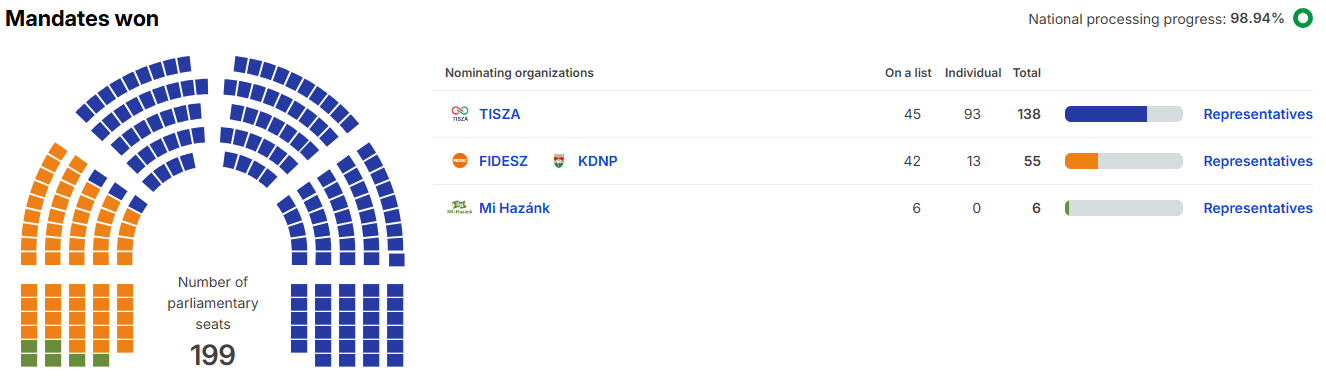

The election results

Hungary delivered a clean political break. The Péter Magyar-led Tisza Party won a decisive, two‑thirds parliamentary majority on record-high turnout, ending Viktor Orbán’s Fidesz party’s 16‑year dominance and securing full legislative control in a single vote. While the results are still not official, the most likely outcome is that Tisza won 138 of 199 seats. The three single-member constituencies are still in limbo due to the extremely tight race, and late votes from abroad can change the official outcome. However, none of the possible outcomes would jeopardise the supermajority. In this respect, the result signals not fragmentation but consolidation: voters coordinated around one credible challenger.

Source: valasztas.hu

What’s next in politics?

Until the new government is formed, the Orbán administration is acting as a caretaker government. The new Parliament must be formed within 30 days after the election, so by 13 May. This date is important from another perspective. In Hungary, a special legal regime has been in effect continuously since May 25, 2022, as a result of the state of emergency declared due to the “armed conflict in a neighbouring country,” namely the war in Ukraine. According to current legislation, this state of emergency will remain in effect until May 13, 2026 (parliament decided last October to extend the 180-day state of emergency once again). In other words, the President of the Republic must convene the inaugural session of the new National Assembly following the April 12 elections.

So, while a caretaker government’s actions are limited due to the state of emergency, in theory, the Orbán administration remains in full power until the new government is formed. However, considering the election results, we doubt that the outgoing party will make any major decisions.

What’s next in economic policies?

From a macro perspective, the key takeaway is the unexpected strength of the mandate for regime change, which reduces short-term policy uncertainty while raising expectations of institutional repair, EU relations and fiscal credibility more quickly than expected. We expect to see many positive headlines in the coming weeks, as Péter Magyar attempts to gain a head start in improving relations with neighbouring countries (such as those in the Visegrad Group ) and with the European Union.

While there is widespread expectation that the Magyar government will quickly resolve the EU-fund-related issues, the reality is that it may take longer. Due to allegations of Hungarian spying on EU officials, trust in Hungarian institutions has fallen to a low point. To regain this trust, more than just symbolic measures are needed. In this respect, the RRF deadline could prove too tight, even with a supermajority.

The Hungarian budget is also facing pressure to be restructured, given that the macro backdrop on which it was based has changed significantly. So, first, the new government needs to come up with a new macro baseline that can serve as a credible building block for the reshaped budget. The new government also needs to reshape the economy, and while it can start work on that, a structural change can take more than one political term.

The new government also needs to decide on the price shield measures, which will remain in place until May. Time is of the essence, and in this respect, the most probable outcome would be an extension until the government has more clarity on the fiscal and economic situation. Speaking of fiscal, this year will probably be about dismantling the inherited budgetary and economic policy structure, which could lead to even worse fiscal metrics in the short term. However, the long-term gains may be sufficient to persuade market players and rating agencies to allow the new government time to reshape the country. We think that the first 100 days will be seen as a grace period. Hence, in our view, the first round of sovereign rating decisions in late May and early June won’t result in any change.

Last but not least, the government could set a target date for euro adoption, establishing a path to reach it, which can be shaped later. If timed perfectly, this could boost market confidence and give the Tisza party more time to work on the Hungarian economy with some tailwinds.

What about the HUF?

The scale of the opposition’s win was a surprise. Although market positioning is difficult to read after the US-Iran conflict, the return of EUR/HUF to pre-conflict levels last week suggests that the market was pricing in a simple majority victory for the opposition.

From the market’s perspective, the constitutional majority allows for a smooth transfer of power for the opposition and a faster path to unlocking EU funds, which are the main focus of investors, giving Hungarian assets another reason to extend their rally.

CEE FX performance vs EUR

31 Dec 2024 = 100%

Source: NBH

The situation in the Middle East significantly obscures the situation, with the expected market opening in a risk-off mood and pressure on the entire CEE region. However, if we were to assume some calm in this, we expect EUR/HUF to stabilise at levels of 355-360 and the bond and IRS curves to move down by about another 30-40bp in the coming days. In our view, the long end of the curve should benefit most from the result, with a better GDP outlook driven by the expected inflow of EU funds and, at the same time, the topic of euro adoption, which the opposition emphasised in its election campaign. On the other hand, the short end will remain burdened by the US-Iran conflict and higher energy prices, preventing the central bank from cutting rates in the coming months despite FX outperforming CEE peers. This will result in curve flattening.

However, another unknown and an increasingly volatile factor in the coming days will be the timing of profit-taking. Given the significant global uncertainty, investors are likely to want to realise profits earlier than usual, which is likely to lead to higher volatility.

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.