Resume af teksten:

Japan oplever en stigning i arbejdslønninger, som kan understøtte en renteforhøjelse fra Bank of Japan (BoJ) i juni. Arbejdslønningerne steg 2,7% år-til-år i marts, men væksten var lavere end forventet. Reallønningerne er steget med 1,0%. Tokyo’s inflation i april steg med blot 1,5% år-til-år, hovedsageligt på grund af regeringens tiltag som prislofter på benzin. USDJPY steg til nær 157-niveauet, trods mulig markedsintervention under Golden Week. BoJ’s forsinkelse i renteforhøjelser kan påvirke japanske statsobligationer (JGB). JGB-yieldkurven er stejlere, delvist påvirket af konflikten i Mellemøsten. Fortsat energiprisstigning forventes at drive inflationen op. BoJ forventes at fortsætte med gradvise rentestigninger i kommende år, med en samlet stigning på 50 basispoint forventet i 2026.

Fra ING:

Steady wage gains are strengthening the case for a Bank of Japan rate hike in June. Clearly, persistent uncertainty in the Middle East poses a downside risk to this outlook. Yet any hesitancy by the BoJ to proceed with further tightening could increase pressure on government bonds and JPY

Labour cash earnings

Real earnings rose 1%

Labour cash earnings rose in March, yet weaker than expected

Japan’s labour cash earnings rose 2.7% year-on-year in March (vs a revised 3.4% in February, 3.2% market consensus). Regular wages rose 3.0%, while bonuses declined 1.5%. Real earnings rose 1.0% in March (vs 2.0% in February, 1.8% market consensus)

Although March wage growth was below expectations, it’s noteworthy that real wages have now increased for three consecutive months. We expect wages to improve in coming months based on this year’s strong Spring wage negotiation (Shunto) results.

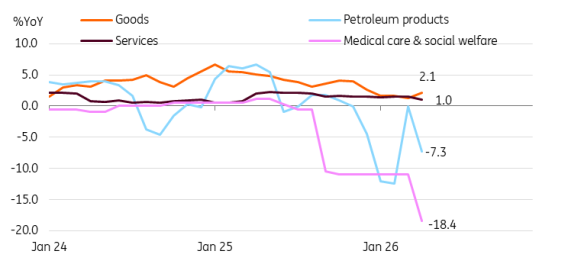

Government actions limited increasing inflationary pressures

The April Tokyo CPI rose a surprisingly modest 1.5% YoY. But this was mainly due to the government’s actions, including price caps on gasoline and the waiving of nursery services fees. If these measures were removed, underlying inflation would remain well above 2%. Government efforts indeed reduced consumers’ burden, but these steps are unlikely to be sustainable. With the real interest rate deeply negative and wage growth expected above 5%, the BoJ may be at risk of falling behind.

Tokyo inflation rose only 1.5% but mostly due to government measures

Source: CEIC

USDJPY climbed up to near 157 level

During the Golden Week holiday in Japan, FX authorities were believed to intervene in the market to stabilise the JPY. The market estimates that the amount was at least 5 trillion JPY. But it seems like the impact didn’t last long. The USDJPY briefly touched 155 on 6 May and traded near 157 this morning. This was already argued by our FX strategists.

Even if the Bank of Japan raises rates in June, as we expect, the effect on the yen will be minimal, as market expectations regarding the Fed shift as well. Therefore, a rate hike in June likely won’t be enough to alter the trajectory of the yen. We believe a joint intervention with the US is possible, especially as US Treasury Secretary Bessent is set to visit Japan en route to China. Markets are expected to remain cautious ahead of Bessent’s visit.

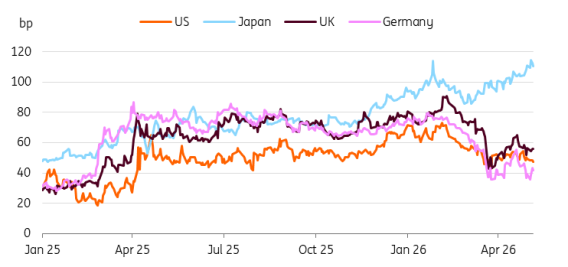

The BoJ’s hesitance on rate hike is likely to weigh on JGBs

The Japanese government bond (JGB) curve steepened after the Middle East conflict began in early March, unlike other developed markets. However, long-term JGB yields were rising even before March. In our earlier research , we argued that increasing long-term yields indicate a return to normal economic conditions, moving away from deflation. The ongoing conflict in the Middle East has contributed to a steeper yield curve in Japan; increases in energy prices are expected to elevate inflation expectations. Meanwhile, the pace of BoJ rate hikes has not kept up with these developments.

Even if the war ends, we expect JGB yields to rise steadily. Large fiscal spending steps to mitigate energy shocks should weigh on JGB yields. Also, energy prices won’t return to the pre-war level. Thus, inflation is likely to rise further and remain sticky. Also, risk-on sentiment may trigger asset rotation from safe assets to risk assets. The BoJ’s policy normalisation will continue, with further rate hikes ahead—though the pace is likely to remain gradual. We expect the BoJ to tighten a total of 50 bps in 2026. The BoJ’s bond purchase operation will also continue to reduce long-end bond demand. All of these point to 10YJGB yields heading to 3%.

JGB yields are expected to rise further

Source: CEIC

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.