Resume af teksten:

Den filippinske regering har erklæret en national nødsituation som følge af oliekrisen, der forårsager mangel på råolie og stigende brændstofpriser. Dette har ført til nedjustering af landets vækstprognose. Filippinerne er stærkt afhængige af importerede olieprodukter, hovedsageligt fra Den Persiske Golf, hvilket gør landet sårbart over for prisudsving og forsyningsafbrydelser. Regeringen forsøger at sikre alternative olietilførsler og indfører målrettede subsidier for at afbøde virkningerne af de stigende priser. Økonomisk vækst forventes at falde som følge af øgede omkostninger til olieimport og højere logistik- og transportpriser. Arbejdsløshedsprocenten er steget, og der er pres på den filippinske peso som følge af en stigende betalingsbalanceunderskud. Den centrale bank forventes at overvåge inflationen tæt, med en potentiel renteændring mulig allerede i april.

Fra ING:

The oil shock has forced the Philippines to declare a national emergency as crude shortages and surging pump prices accentuate the downside risks to growth. We have cut our growth forecast accordingly. While inflation is set to breach the target, raising the odds of a rate hike, monetary tightening alone is unlikely to notably change the peso’s trajectory

Transport strikes and nationwide protests as fuel prices surge in the Philippines

National emergency declared as oil shock intensifies

Oil shortages and persistently high crude prices have become a significant macroeconomic headwind for the Philippines, prompting the government to declare a national emergency. The country is among the most oil‑dependent economies in the region, with energy consumption overwhelmingly reliant on imported petroleum. Domestic crude production is negligible, and over 95% of oil imports come from the Persian Gulf, leaving the Philippines exposed to both price swings and supply disruptions. The transportation sector is the largest consumer of oil products, meaning fuel costs feed directly through to logistics and household expenses. This vulnerability is further aggravated by limited domestic fuel reserves, with the energy secretary noting that the country has roughly 45 days of diesel supply remaining.

Government response: securing supply and providing targeted relief

In response, authorities have begun to secure alternative supply sources, including a 700k‑barrel shipment from Russia. Yet with national consumption estimated at 450–487k barrels per day, this volume would cover only a few days of demand unless additional shipments are secured from Russia or China.

Unlike several Southeast Asian neighbours, such as Indonesia, Malaysia and Thailand, the Philippines maintains fully market‑linked retail fuel prices with no broad-based subsidies. As a result, pump prices have more than doubled since the start of the conflict. To cushion the impact, the government introduced targeted subsidy measures this week. The Department of Energy has activated a $333 million emergency fund to support these transfers, and a new law now permits the temporary suspension or partial reduction of excise duties on selected petroleum products. While the fiscal cost is currently modest at around 0.07% of GDP, the Philippines’ relatively thin fiscal buffers mean that any significant expansion of support would increase pressure on government financing.

Economic impact: growth forecast revised down

The ultimate economic impact will depend on how long the disruption persists, but the shortages are already amplifying existing weaknesses in domestic demand. The direct hit to GDP will come through a higher oil and gas import bill, which is currently about 4% of GDP. Indirect effects will stem from rising transportation and logistics costs, which will feed through to consumer prices. Substitution options are limited: petroleum still accounts for 46% of the Philippines’ fuel consumption while renewables, including solar, hydro and wind, contribute only about 12%. In our base case, with Brent oil prices averaging $80-85/bbl in 2026, the higher oil import bill alone could shave roughly 80bp off GDP growth.

Against this backdrop, we are revising down our 2026 GDP growth forecast to 4.5%, from 5.2% previously. The economy is entering this period of elevated energy costs from a position of vulnerability, following an already weak 2025 performance driven by a sharp contraction in government spending.

Energy consumption is skewed towards petroleum products

Weak fiscal buffers despite collapsed government spending

The primary driver of the 2025 growth slowdown to 4.4% year-on-year was weak government spending. Expenditure rose only marginally by 1.8% YoY in 2025, a sharp deceleration from the strong 20% YoY expansion in the previous year, creating a significant drag on overall growth. However, this spending restraint did not translate into fiscal consolidation. Tax revenues also fell short of target, partly due to the temporary pause in payments for infrastructure‑related government contracts amid investigations into flood‑control projects, which in turn affected withholding tax collections. As a result, the government posted a wider‑than‑expected deficit of 5.63% of GDP, above the official estimate of 5.5% and only slightly below the 5.7% deficit recorded in 2024.

While the government has some room to extend fuel subsidies beyond the recently announced package, that fiscal space is limited. Any additional support would risk further delaying capex spending, which would in turn slow the broader growth recovery. Even if spending normalises somewhat in 2026, the drag from tight fiscal conditions on confidence and economic activity will take time to fade. With consumer sentiment still weak, we expect the recovery to remain uneven. As a result, our 2026 growth forecast remains at 4.5%, with risks clearly tilted to the downside.

Philippines has one of the weaker fiscal balances in the region

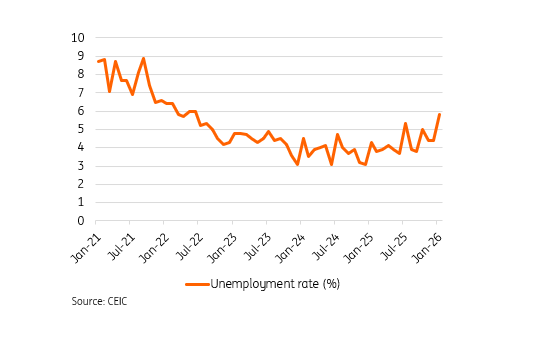

Labour market conditions are deteriorating

Labour market conditions have weakened noticeably. The unemployment rate rose to 5.8% in early 2026 from a recent low of 3.8% in late 2025. Weaker government spending has now translated into softer private investment, job losses, and a slowdown in wage gains. These trends are likely to intensify as higher oil prices raise production costs, discourage hiring, and compress real incomes.

The unemployment rate has picked up sharply recently

Policy outlook: Base case on hold in April, but probability of a hike has risen materially

Historically, the Bangko Sentral ng Pilipinas has shown that maintaining inflation stability is the core driver of its monetary policy decisions. In an unscheduled meeting yesterday, the BSP reaffirmed its commitment to anchoring inflation expectations and taking a forward‑looking approach, particularly amid the risk of second‑round effects from rising oil prices. Previous episodes in 2022 and 2018 demonstrate that the BSP tended to hike rates once inflation breached the upper end of its 4% target.

With Brent crude prices up roughly 40% month‑on‑month in March, headline inflation is now likely to exceed the target band even under our base case. This implies that CPI could breach 4% as early as March, raising the probability of a rate hike as early as April.

However, today’s growth environment is very different from 2022, when GDP growth exceeded 7.5%. The collapse in government spending has fed through to weaker investment and consumption, creating a materially softer growth backdrop and heightening downside risks. Real policy rates were already elevated before the oil price shock, meaning an additional hike would further constrain investment.

Given this weaker growth setting, and assuming the current conflict eases soon, our base case is that the BSP remains on hold in April.

That said, if oil prices stay above $100/bbl in our longer-war scenario, and with limited signs of de‑escalation in the ongoing conflict, the BSP may be compelled to consider raising rates as soon as April.

Price stability has historically been a key mandate of the central bank

External balances under pressure; peso risks skewed to further weakness

Higher oil prices are likely to widen the current account deficit further. Our estimates suggest that sustained prices above $100/bbl in 2Q 2026 would push the current account deficit to 4% of GDP in 2Q from 2.4% in 1Q.

This deterioration heightens depreciation risks for the Philippine peso. The BSP’s recent guidance – that it is not defending any specific exchange‑rate level and that intervention in the FX market remains modest – suggests limited resistance to further currency weakness. While rate differentials matter, historical experience shows that FX performance is more closely driven by external balances. With the USD supported by safe‑haven flows and the Federal Reserve unlikely to ease aggressively in the near term, domestic tightening alone is unlikely to materially shift the peso’s trajectory. A move beyond PHP 61/USD remains a clear risk.

Weaker external balances likely to drive PHP lower

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.