Resume af teksten:

De amerikanske aktiemarkeder når nye højder, mens oliepriserne og forventningerne til rentestigninger forbliver høje. Der er en markant forskel mellem stigende aktiemarkeder og høje oliepriser, som påvirker centralbankernes forventninger. Føderalreserven (Fed) ser ud til at hælde mod rateforhøjelser frem for sænkninger, hvilket er ændret fra tidligere forventninger. Den britiske renteforhøjning ser ud til at være mere dramatisk end i eurozonen, men briterne er mindre tilbøjelige til at hæve rentesatserne end Den Europæiske Centralbank (ECB). Markedernes forventninger er tæt forbundet med oliepriser fremfor naturgas, på trods af naturgasens større betydning for Europas energipriser. Centralbankerne kan være mindre tilbøjelige til at reagere aggressivt på olieprisændringer.

Fra ING:

US stock markets are surging to new highs. Oil prices are certainly not back to their lows – and neither are interest rate expectations. One of those things surely can’t be right, can it? This week, James Smith looks at what investors could be getting wrong about central bank policy, as the team builds up to another big week in global markets

Equities are surging to new highs even as oil and rate expectations remain elevated

What markets are getting wrong on rate hikes

One of many striking features of markets right now is the gap between equities, which have shrugged off their mid-war losses and are surging to new highs, and oil prices – and by extension central bank expectations – which remain well above pre-war levels.

It’s hard to believe both are right. And when it comes to the way investors are thinking about central banks, I see four aspects that look particularly difficult to square with our own views here at ING.

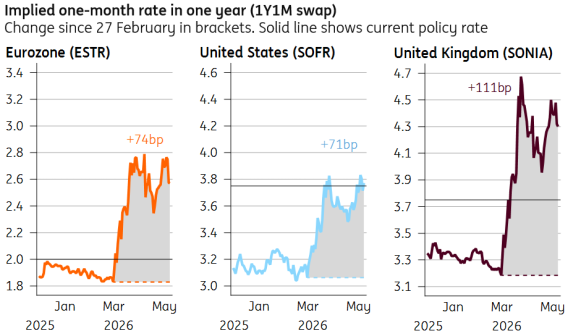

First, Fed rate hikes. Markets now think rates are more likely to go up than down, albeit marginally, after weeks of pricing cuts. The spread between US and eurozone interest rates has widened; the scale of repricing since the war began now looks identical in both regions.

That’s a change. For several weeks, the working assumption was that Europe faced a much more severe inflation shock, warranting greater tightening than in the US.

How central bank expectations have changed

Source: Macrobond, ING

Why the shift? Eurozone data has undershot expectations, while the US has held up better. The recovery in US equities weakens the case for near‑term cuts. And the Fed itself has made a concerted effort to talk up market rate expectations, with several officials keen to ditch the easing bias.

We’re not so sure. James Knightley still thinks rate cut(s) are more likely than not before year‑end – and the disagreement hinges on how you view the US jobs market.

Fed officials increasingly point to collapsing net migration. In 2023, net inflows were 2.7 million. This year, they’re projected at just 0.3 million, with a real risk that figure drops to zero or below. Combined with an ageing population, labour supply growth has effectively stalled. That means zero or even negative payroll numbers are potentially less of the red flag they once were. And bumper numbers like today’s , at a headline level at least, look all the better.

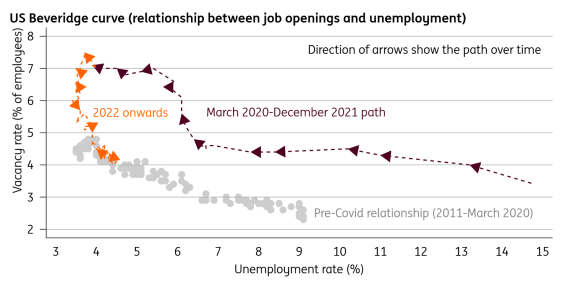

True. But with labour demand also low across various metrics, the jobs market is more vulnerable than it was three or four years ago.

For a long time, vacancies fell without unemployment rising: firms stopped hiring aggressively, but didn’t cut staff. That relationship has now normalised. Any further fall in job openings is much more likely to push joblessness higher than it was two years ago.

And whatever growth remains is extraordinarily concentrated. Private health and social care – less than 20% of total employment – continues to account for a large portion of job creation.

The relationship between vacancies and unemployment has normalised

Source: Macrobond, ING

Second, the UK repricing looks strange. Interest rates are now seen more than a percentage point higher in a year’s time than before the war – around 40bp more than the equivalent ECB repricing.

That partly reflects the experience of 2022, when Britain emerged with a bigger and more persistent inflation problem. The UK is often described as being particularly sensitive to energy shocks.

That’s only half right.

Yes, Britain is among the most reliant on natural gas, which makes up around 32% of total energy consumption, compared with 20% in Germany and 15% in France. But this is not a gas crisis – at least not yet. Natural gas prices have remained far more contained than in 2022.

Look at net energy imports, and the UK actually scores better than much of Europe. Net all that out, and my UK inflation forecasts look virtually identical to our eurozone numbers.

Third, the Bank of England is less likely to deliver two rate hikes than the ECB. Given what I’ve just said, it seems strange that markets are pricing a similar amount of tightening for the remainder of this year in both economies.

Not least because the message from both central banks last week was markedly different. The ECB seemed remarkably clear that it was on track to hike rates in June unless the situation dramatically changes. The BoE, by contrast, implied that simply not cutting rates – which it may well have done had the war not happened – already amounts to defacto tightening. The case for hiking above current levels was far less clear-cut.

True, here at ING we expect a one-and-done hike on both sides of the channel. But if you had to ask me if the ECB or BoE were more likely to hike, or tighten more in total, then notwithstanding UK political risks, it seems pretty clear that it’s the former.

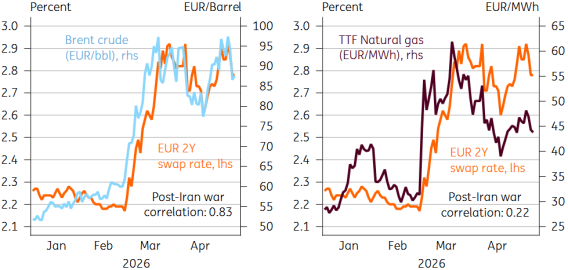

Finally, markets still appear to be overplaying the energy channel. Market expectations for the ECB and BoE are still trading very tightly with oil prices. It’s something our Rates Strategy team has repeatedly flagged; the correlation between two-year euro swap rates and Brent crude since the Iran war has stayed very high at 0.83. For natural gas, it’s just 0.22.

Rate expectations have moved more with oil than natural gas

Source: Macrobond, ING

As I’ve already discussed, that distinction matters. In 2022, natural gas and its impact on electricity prices was arguably the central problem for Europe. In reality, I suspect central banks are going to be less sensitive to oil and more attentive to natural gas, relatively speaking, than those correlations currently imply.

And so long as natural gas prices stay low, central banks are less likely to hike rates as aggressively as markets have recently been expecting.

James Smith

THINK Ahead in developed markets

United States (James Knightley)

Inflation (Tue): A second consecutive 0.9% month-on-month print is expected at the headline level, attributable mainly to the surge in gasoline and diesel prices. Higher airline fares will also contribute, while a rebound in medical care and recreation, after soft March readings, risk a 0.3% MoM for core inflation reading, pushing the annual rate up to 2.7%. We continue to believe the headline surge is temporary given the lack of demand impetus that would risk broader, more persistent inflation.

Retail sales/Industrial production (Thur/Fri): The former is likely to be lifted by higher gasoline prices given that this is a nominal dollar figure. However, other components will be softer with auto sales a drag. Industrial production should post a modest rebound given ongoing strength in the ISM manufacturing index.

The other big event will be Jerome Powell’s final day as Federal Reserve Chair with Kevin Warsh taking over on Friday 15 May.

THINK Ahead in EMEA

Poland (Adam Antoniak)

1Q26 flash GDP (Thu): Following a poor beginning to the year due to the cold winter, economic activity regained momentum in March. Still, we estimate that annual growth was only slightly slower than the 4.1% YoY posted in 4Q25 and amounted to 3.8% YoY, marking a solid start to 2026. The composition of GDP will be published at the beginning of June, but we expect private consumption to have remained solid, while fixed investment underperformed.

Final Apr CPI (Fri): The StatOffice should confirm that CPI inflation increased to 3.2% YoY in April from 3.0% YoY in March. According to our estimates, the increase was driven by an acceleration in core inflation. The key question is whether this stemmed from price rises in narrow components of the consumer basket – such as airfares and holiday packages – or reflects more broad‑based inflationary pressures, pointing to potential second‑round effects following the initial energy shock.

Mar BoP (Fri): We forecast the March current account deficit at €0.3bn, i.e. much narrower than the €1.1bn reported in March 2025. As a result, the 12‑month rolling deficit most likely narrowed to 0.8% of GDP from 0.9% of GDP after February. Foreign trade in goods was almost balanced, amid an 8.1% YoY increase in euro‑denominated exports, while imports advanced by 3.2% YoY. External imbalances remain low.

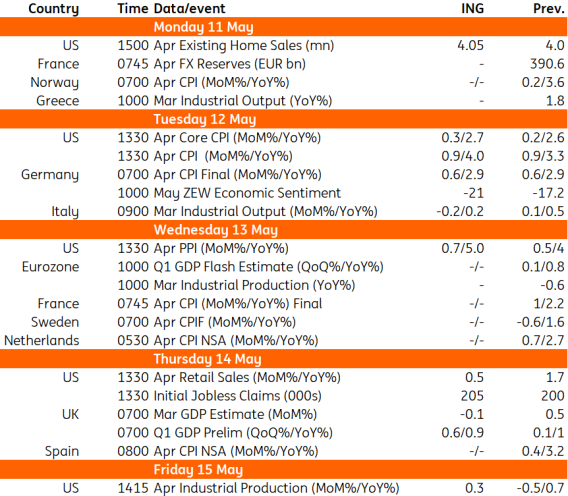

Key events in developed markets next week

Source: Refinitiv, ING

Key events in EMEA next week

Source: Refinitiv, ING

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.