Resume af teksten:

Sydkoreas eksportører viste stærk præstation i første kvartal trods stigende inputomkostninger og forsyningsbegrænsninger. Eksportpriser steg 28,7% i marts, hvilket viser evnen til at overføre omkostningsstigninger til outputpriser. Arbejdsløshedsprocenten faldt til 2,7% i marts, men faldet skyldtes delvist, at arbejdere forlod arbejdsstyrken. Jobvækst var primært i lavtlønnede servicepositioner, mens fremstillingssektoren mistede 41.000 jobs. Importprisindekset steg 18,4% årlig i marts, med forventninger om stigende indenlandsk inflation. Eksportvolumen steg 23% i marts, hvilket styrkede økonomien i første kvartal. Politikers udfordring er at balancere stærk eksportvækst mod svag indenlandsk efterspørgsel og stigende inflation. Det Nationale Pensionssystems FX-afdækningsstrategi kan stabilisere KRW-markedet, med forventet lavere USDKRW ved udgangen af 2026.

Fra ING:

South Korea’s exporters performed robustly in the first quarter, overcoming rising input costs and supply constraints and offsetting weaker domestic demand. The Bank of Korea will face increasing challenges balancing sluggish domestic demand against robust export growth as inflationary pressures intensify in the coming months

Unemployment rate

Jobless rate fell in March, but suggests subdued demand

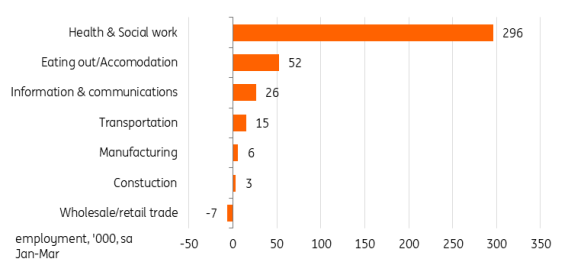

South Korea’s jobless rate fell to 2.7% in March (vs 2.9% in February and market consensus). However, the details were quite weak. The decline, for example, was partly due to workers exiting the labour market rather than to job growth. The labour participation rate edged down to 64.8 (vs 64.9 in February). Also, most of the job growth was concentrated in low-wage, low-skilled service positions and self-employment. By contrast, manufacturing and salary-based employment declined. Manufacturing lost 41k jobs, almost reversing the first two months’ gain. Among service positions, adding the most jobs were eating out and accommodation (37k), transportation (12k), and information & communications (35k). These jobs are mostly non-regular and low-wage, having a limited positive impact on household spending. We think this trend indicates subdued domestic demand.

We are also concerned that supply disruptions lasting beyond two months could weaken labour market conditions across a broader range of industries. Petrochemical activity – including Naphtha Cracking Centres – utilisation rates have already dropped to their lowest levels in March. This type of enforced production slowdown is expected to become widespread and to start hurting employment in other sectors. We think government job programs will provide a buffer, but underlying conditions are likely to deteriorate.

Private sector hiring remained weak in 1Q26

Source: CEIC

Export price index

Exporters transfer increases in input costs to output prices

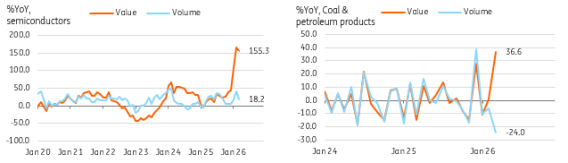

Commodity price hikes boosted the import price index markedly by 18.4% year-on-year in March (vs 1.6% in February). The export price index rose 28.7% in March (vs 11.1% in February). We believe that Korean exports can pass higher input costs on to output prices. As such, we haven’t yet seen much damage to the terms of trade. For coal and petroleum products, export volume dropped 24%, likely due to reduced production capacity and export controls, while the value rose 36.6%. Despite the Middle East conflict, oil imports were little affected until March, when import volume rose 13.4%. We expect this to decline over the next couple of months, with its impact on production activity increasing in the second and third quarters.

Meanwhile, import price increases are expected to drive domestic inflation. Although government policies have capped gasoline and utility prices so far, inflation is projected to rise significantly from April. Travel, transportation, home appliances, and electronics prices have all seen notable increases. The recent weak KRW will add pressures even more.

In volume terms, exports rose 23% in March, outpacing imports at 12.3%. For the first quarter, exports and imports rose 9.3% quarter-on-quarter, seasonally adjusted, while imports grew 4.2%. This indicates a strong net export boost to GDP. Based on stronger-than-expected exports, we expect 1Q26 GDP to grow by 1.0% (vs -0.2% in 4Q25).

Export grew strongly in 1Q26

Source: CEIC

K-shaped recovery put policymakers in difficult position

Today’s data indicates strong economic growth in the first quarter, primarily driven by resilient exports. However, domestic demand has remained quite fragile and inflationary pressures are expected to accelerate in the near future. Additionally, supply disruptions are expected to affect economic activity this quarter and into next. The government’s fiscal support (26 trillion won worth of extra spending) will likely provide some buffer, but growth conditions are likely to soften in the middle of the year. ING thinks supply disruptions will improve in the coming months, though only modestly. If our base-case scenario holds, the oil supply disruption will have a more prolonged impact on inflation than on growth. In this context, we believe that the Bank of Korea won’t be in a hurry to hike rates. But macro conditions will support the BoK focusing on curbing inflation expectations and improving financial imbalances. We think the BoK could hike rates as early as July.

NPS FX hedging is likely to stabilize won

The National Pension Service has established its FX hedging ratio at approximately 15%, allowing for operational flexibility within a range of an additional 5 to 10 ppt. However, specific details regarding the strategic and tactical hedging ratios were not disclosed. By the end of 2025, the NPS’s foreign assets had reached approximately $600 billion, indicating that at least $90 billion is eligible for hedging. Additionally, the NPS intends to issue foreign-denominated bonds next year. This change could further ease pressure on the KRW market. We continue to view geopolitical risk as the main short-term factor influencing the KRW and expect ongoing high volatility. For now, we maintain our 1450 to 1550 range in the near term. However, NPS’s hedging strategies, attractive valuations in the Korean equity market, narrowing policy rate gaps between the BoK and the US Federal Reserve, and increased investment in KTB through WGBI are expected to ease some pressure on the KRW during the second half of 2026. Thus, the USDKRW is expected to decline to 1,425 by the end of 2026.

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.