… but it is important to note that in today’s negative GDP print, it was net trade (exports less imports) that subtracted -1.9% from the final GDP print, driven by a -1.03% annualized drop in exports. This was the biggest hit to US trade since the great financial crisis.

The breakdown of the chart above is shown as follows, with Net Trade in real dollar terms subtracting $545 billion from US GDP, following the lowest exports number since Q2 2014 even as imports rose to a new all time high (most of it likely going to boost already near record high inventories):

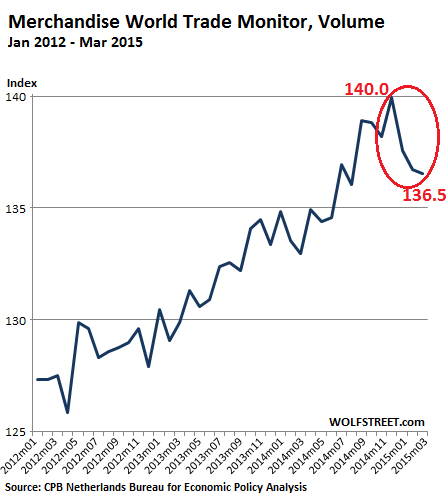

Again, none of this is a surprise, and contrary to what some superficial pundits may claim, this is far more than oil. Deutsche Bank explains:

The first is the surprisingly sharp drop off in global trade in early 2014 that followed weakening into yearend 2014. This is over and above the decline in oil. It is likely affected by the west coast port issues but this doesn’t obviously account for other regional weakness. In the grand scheme of things trade is well correlated with turning points in the interest rate cycle and all else equal clearly “justifies” current low real yields. It is a requirement almost now for trade volumes to stabilize and improve for yields to be stable or higher.

Why trade is so weak may speak to the demand side of the secular stagnation debate. Supply creates demand and maybe demand creates supply; the issue is that secular stagnation can be driven by lack of productivity for lack of investment or innovation. But also demographics and the residual of financial repression can affect the outlook for demand. Note that globally productivity is also very weak whether Japan, Europe or China.

What is really happening is quite simple: the massive surge in the dollar, which we have said since the fall of 2014 will crush both GDP and corporate profits (as confirmed earlier today) has led to a collapse in US exports, and thus, trade contribution to GDP, over and above the deterioration in global trade as is.

Worse: as Aurelija Augulyte conveniently reminds us, it is about to get even worse: the reason, an advance read of the nominal effective USD exchange rate (as in stronger dollar due to fears of an imminent rate hike by the Fed) implies that US exports are about to really crash, which means Q2 GDP may not only not meet the Atlanta Fed’s 0.8% estimate, but may even print negative especially if the US economy can’t stock up on any more inventory (already just shy of all time highs).

So yes, crashing trade as a result of not only the soaring dollar but a secular decline in global demand is horrible news for the economy. But not horrible news for everyone.

As the following chart shows, US Treasurys are once again ahead of the game (certainly ahead of manipulated equities), and reflect not only the Fed’s and other central banks’ monetization of debt (which in turn is dictated by the collapsing global economy), but also the plunge in world trade volumes….

… a correlation which can be seen for global bond yields as well!

In other words, the worse the econ data, as manifested in this case by global trade, the lower bond yields will drop. In fact, with global trade now contracting, global NIRP, already tested in Europe, is just a matter of time.

And the punchline: since the entire concept of QE has been flawed from the beginning, and as we said from day one, will and has led to a disintegration of the economy unless someone stops the crazed central-planners, the lower bond yields drop, the greater the secular decline in aggregate demand (aka “deflation”), the more businesses focus on investing in short-term capital gains (see Chinese stocks) instead of long-term growth projects (see Capex), the worse global trade will get, forcing even more debt monetization, even lower yields, even lower trade, until finally even the central planners realize that money printing as a circular falacy, and have no choice but to finally dump money out of drones (as seen here) in the last ditch effort to spur (hyper)inflation.

And with that final “lights out” act for fiat currencies and the existing monetary regime, they will finally succeed… in destroying themselves.

{kind=link}