Nothing matters…for now | | Flows are in control, and nothing else seems to matter. Oil, volatility, macro — all getting ignored as mechanical buying keeps pushing markets higher. But under the surface, things are getting stretched, and the setup is becoming more fragile. This works… until it doesn’t. |

|

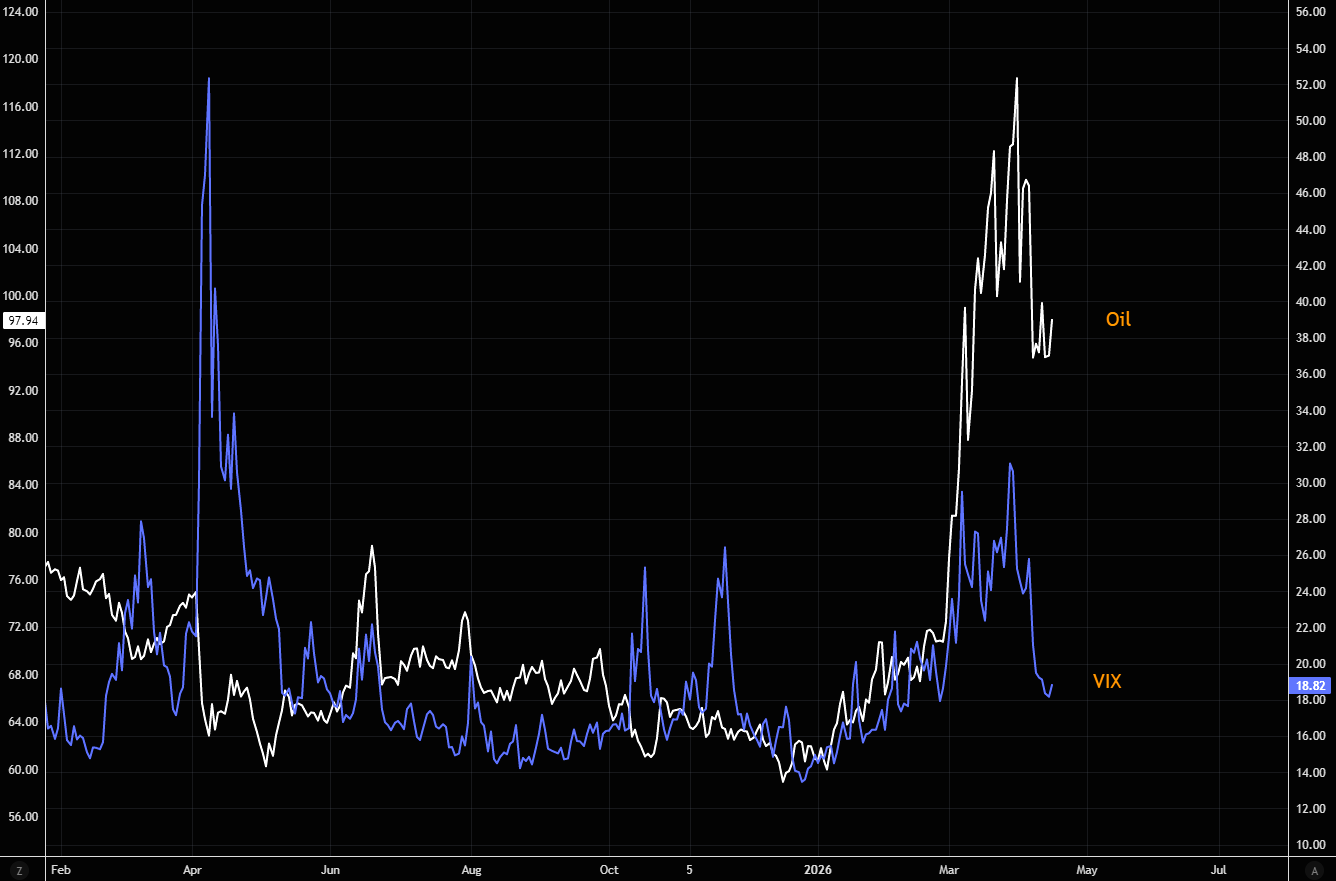

Who cares about oil? | | The SPX vs. inverted oil gap has extended even further. The market has been quick to dismiss the oil connection, but part of this extreme squeeze is driven by mechanical buying, which doesn’t care about oil. |  LSEG Workspace LSEG Workspace |

|

Just in case hedges | | Imagine if the market starts caring about oil again. The gap between oil and VIX is wide, and is getting “uncomfortable”. |  LSEG Workspace LSEG Workspace |

|

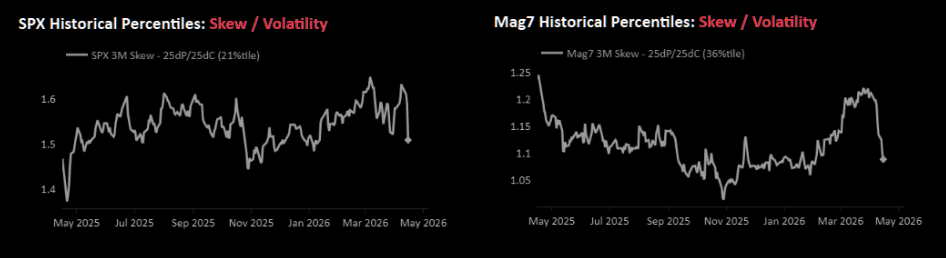

Skewed | | Skew in the form of SPX and Mag7 25d put/25d call has crashed. We come back to what we outlined yesterday: you buy protection when you can, not when you must. This is one of those times. More here. |  Nomura Nomura |

|

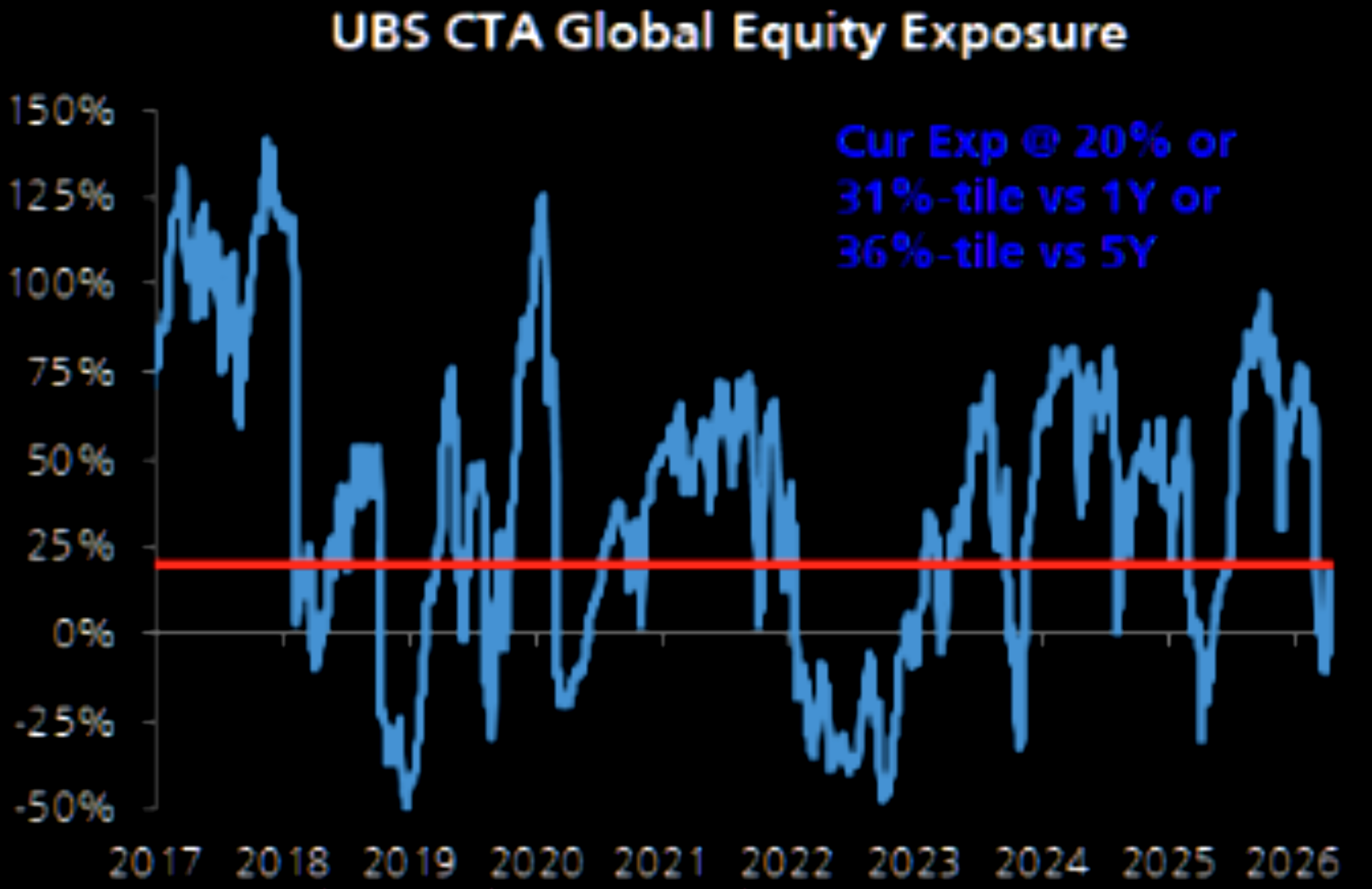

| | The flows behind this move are still powerful. Last week: CTAs bought ~$86bn of equities, ~$45bn in the US. That is meaningful flow. Next five days: another ~$69bn coming, ~$37bn in the US. That is also significant. They buy VWAP-style, and days like yesterday, quiet tape, steady grind higher, show how powerful that flow is. This isn’t something to stand in front of, it’s something to go with, writes GS sales desk. |  UBS UBS |

|

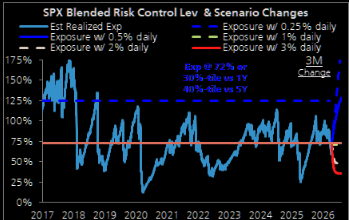

Risk controlled players | | Risk control has not been a meaningful buyer yet, with exposure flat week-over-week, held back by elevated realized volatility. If the pace of the move higher slows, risk control could step in, with potential buying of around $185bn over the next month, assuming SPX averages +/-50bps daily moves, writes UBS. |  UBS UBS |

|

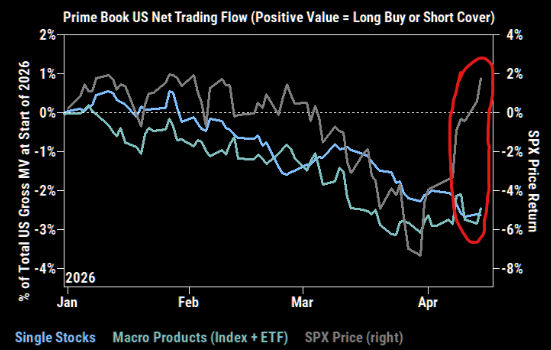

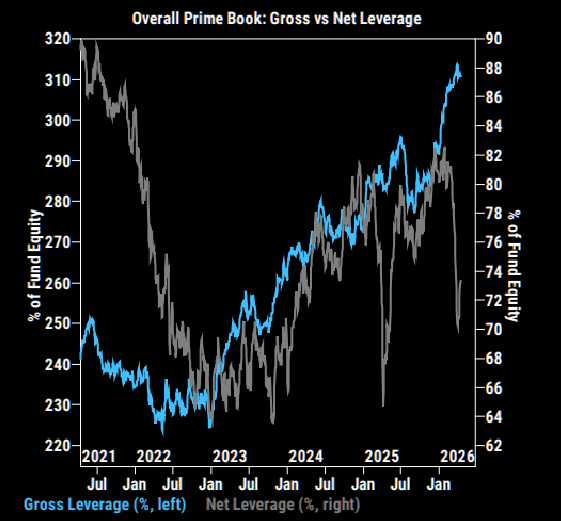

| | We have seen some short covering, but far from massive. There is definitely room for nets to increase further. |  GS GS |  GS GS |

|

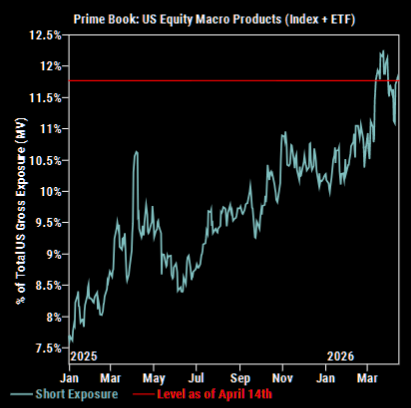

Still short | | “Overall short exposure in macro products (Index + ETF) is only modestly below the peak level seen at the end of March”. |  GS GS |

|

| | The squeeze in MAGs has been truly magnificent. Since breaking above the negative trend line, this sector has exploded higher. Note we are well above the 50-day MA, approaching the upper part of the range quickly. |  LSEG Workspace LSEG Workspace |

|

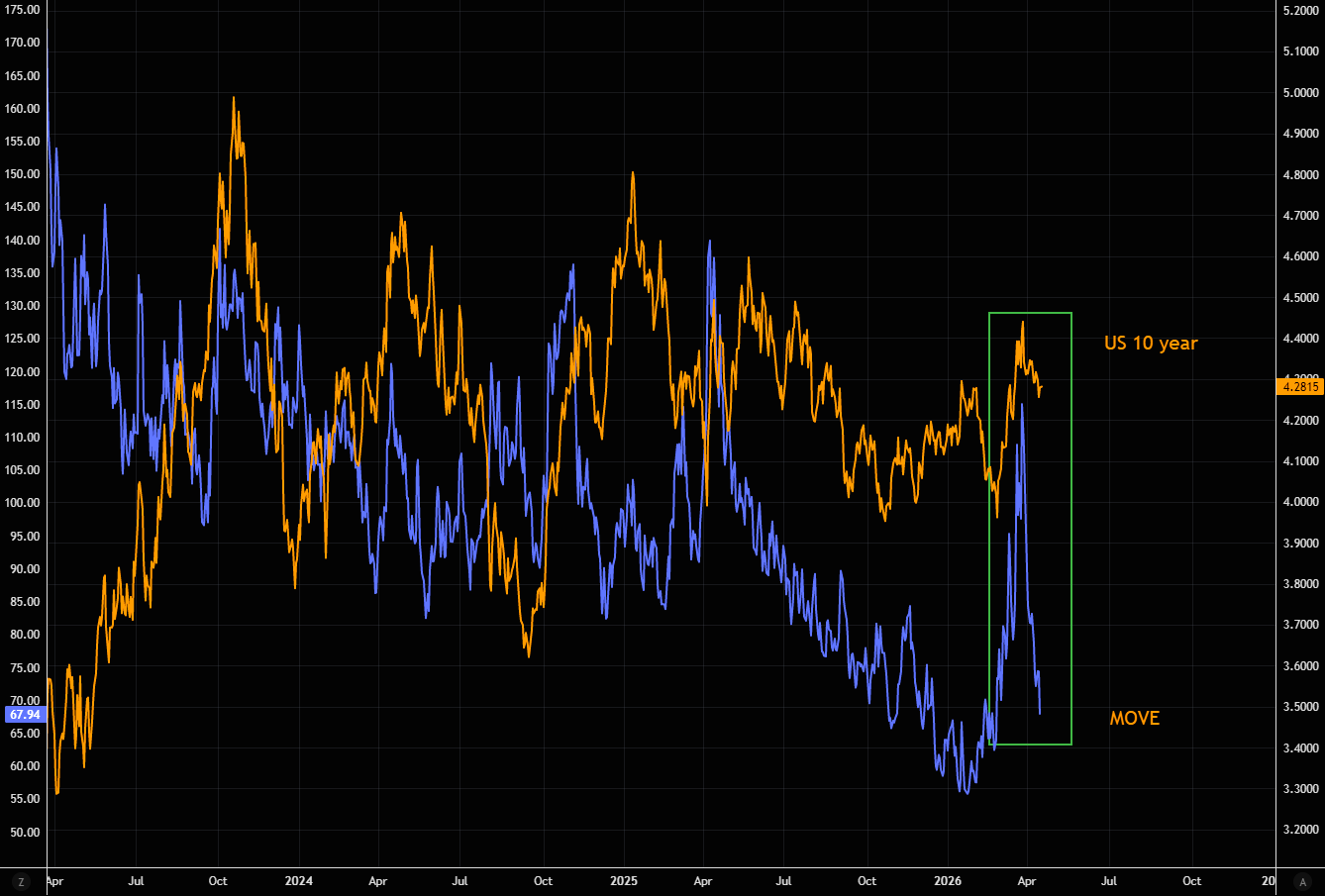

| | Bond volatility, measured by MOVE, surged from around 70 to 115 as the 10-year yield jumped from below 4% to 4.45%. Since then, the 10-year has eased back to around 4.3%, while MOVE has fully reversed the spike. This marks one of the sharpest bond volatility resets we’ve seen. More here. |  LSEG Workspace LSEG Workspace |

|

| | IGV has bounced for the fifth time on those massive supports. This bounce has a lot of similarities to what we saw during the Liberation Day chaos. Last time this setup played out, the move didn’t stop at the first bounce. More on software here. |  LSEG Workspace LSEG Workspace |

|

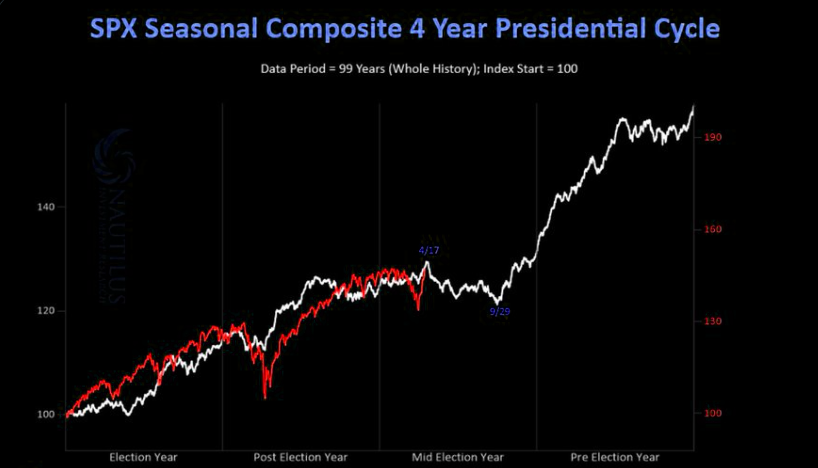

| | SPX election cycle seasonal composite would indicate that the rest of the year will not be spectacular. That makes the current setup even more fragile. More here. |  Nautilus Nautilus |

|