Resume af teksten:

Den Reserve Bank of Australia forventes at hæve renten med 25 basispoint den 5. maj. Inflationsrisici i Australien stiger, hvilket understøtter rentestigningen. Filippinernes BNP forventes at vokse med 4,3% år-til-år trods høj inflation, som forventes at stige over 5% i april på grund af højere oliepriser. Sydkoreas inflation forventes at accelerere trods regeringens forsøg på at begrænse stigninger i benzin- og elpriser. For Taiwan forventes april-inflationsdata at vise stigende inflationstryk med en høj eksportvækst. I Kina er der en stille uge forventet på grund af fejring af Arbejdernes Internationale Kampdag fra 1.-5. maj.

Fra ING:

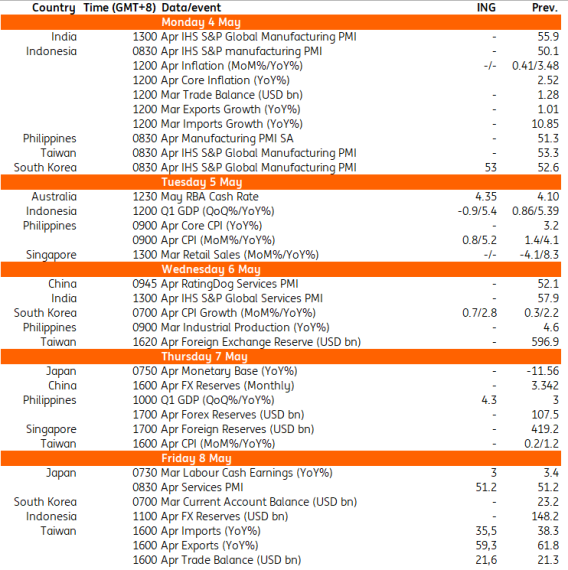

The Reserve Bank of Australia is expected to hike interest rates. Key data releases include GDP and CPI from the Philippines, and inflation from South Korea and Taiwan

Asia Research highlights of the week

China’s PMI data suggests domestic demand remains soft Inflation risks rebuild in Australia, supporting RBA tightening Bank of Japan’s hawkish hold reflects high geopolitical uncertainty Singapore’s growth engines remain intact despite rising energy pressures

Australia: RBA expected to hike by 25bps

We expect a hawkish 25bp Reserve Bank of Australia hike at the 5 May policy meeting. The broader inflation risk backdrop has shifted to the upside. Higher oil prices are likely to generate second-round effects that could place renewed pressure on services inflation. With further pass-through of higher oil prices into transportation, electricity, and utility costs, CPI inflation is likely to remain elevated in the second quarter, strengthening the case for policy action by the RBA.

Philippines: Higher inflation and weaker consumption despite GDP recovery

We expect Philippine GDP growth to recover to 4.3% year-on-year, largely reflecting favourable base effects and some pick-up in government spending. However, consumption growth is likely to remain subdued as unemployment edges higher. On the industry side, weak soft construction activity should continue to weigh on growth, while services activity remains relatively resilient.

We expect CPI inflation in the Philippines to rise above 5% in April. This will be driven by the continued pass-through of higher global oil prices into domestic prices and emerging second-round effects. Higher rice prices are also likely to contribute to the uptick in food inflation.

South Korea: Inflation to accelerate despite government action

South Korea’s consumer prices are expected to accelerate as rising oil prices begin to impact the costs of other goods and services. Government actions should limit increases in gasoline and electricity prices relative to global commodity spikes. But costs for air travel, logistics, and petrochemicals are likely to rise more sharply. The recent weakness of the KRW and the sharp rise in semiconductor prices are beginning to pass on to the prices of other goods. In March, import prices rose 18.4% year-on-year (vs 1.6% in Feb), and prices excluding food and energy rose 10.2% (vs 5.5% in Feb).

China: A quiet week amid Labour Day holidays

It should be a quiet week ahead for China with its Labour Day holidays set from 1-5 May. In terms of data, markets may monitor holiday consumption and travel data as it is released. We’ll also get services and composite RatingDog PMI data.

Taiwan: April inflation should start showing energy price passthrough

Taiwan releases its CPI and PPI inflation data for April on Thursday. We expect to see more signs that inflationary pressure is picking up in April after March showed limited passthrough from higher energy prices stemming from the Iran war. Taiwan releases trade data on Friday. We’re looking for another strong month, with 59.3% YoY export growth and 35.5% import growth, leading to a trade surplus of $21.6bn.

Key events in Asia next week

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.