Merrill venter en bedre aktieudvikling i value-aktier og cykliske aktier i løbet af sommeren og bygger prognosen på den historiske udvikling under bull markets efter store kriser. I det andet år efter et dyk, er det de cykliske aktier og value-aktier, der stiger mest, og det bygger på deres indtjening. Kun én gang har indtjeningen ikke fulgt med. Det store ryk kommer typisk 15-16 måneder inde i et bull market, dvs. i juni og juli – efter krisens kulmination den 23. marts 2020. Det falder sammen med, at det amerikanske vaccinationsprogram er ved at være færdigt, og den økonomiske genåbning vil være godt på vej.

Thought of the week

Next week will mark a year since the COVID-19-induced market low on March 23, 2020.

Historically, small caps tend to outperform large caps in the first year of a bull market, while trends during the second year have been more mixed in terms of large cap vs. small cap and growth vs. value.

We continue to expect value to outperform growth this year as the earnings of financial, industrial and energy companies are much more levered to an economic restart. With earnings a key driver of performance this year, we take comfort in the fact that since 1957, earnings have only contracted once in the second year of a bull run.

However, with the economic re-opening just around the corner, many are becoming wary of when a correction may occur, citing a growing federal budget deficit, rising rates and a return to trend growth.

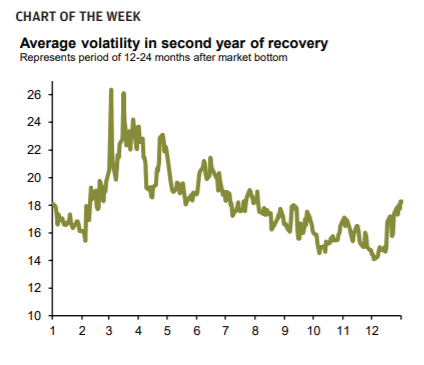

As shown in this week’s chart, which looks at the average path of implied volatility during the second year of a bull market, volatility typically spikes 15-16 months into a bull run, indicating it would not be surprising to see risk assets pull back in June or July.

Interestingly, this is when we expect the U.S. to reach herd immunity and see a major resumption in economic activity.