Morgan Stanley har analyseret den amerikanske flybranche og har lavet en rundspørge, som viser, at de forretningsrejsende regner md, at deres rejseaktivitet vil blive normaliseret i løbet af 2022. Morgan Stanly opstiller fire grunde til, at investorerne allerede nu kan gå ind i den kriseramte sektor, nemlig ved at udvælge de selskaber, der har det bedst fundament, og som har en stærk indenrigsposition, som har mellemlange flyruter, og som har en stærk passagerloyalitet og styrken til at starte ud med lave flypriser. Krisen vil rydde ud i mindre profitable selskaber.

US Airlines Prepare for Takeoff

A U.S. airline recovery may take years, says the market consensus, yet four factors suggest a shorter-than-expected return trip—and an investor opportunity.

Since March 2020, the coronavirus pandemic has battered U.S. commercial airlines, creating billions in losses, as passengers eschewed air travel. Although small signs of improvement have emerged, current market consensus believes that passenger traffic recovery will remain slow—with volumes unlikely to recover to pre-COVID levels until late 2023 or early 2024.

However, in a recent report from Morgan Stanley Research, the firm’s equity analysts lay out a more optimistic timeline for recovery, thanks to pent-up demand, fewer competitors than in past global crises and a more stable fuel-price outlook.

“Although the next 6–12 months contain risks from pandemic uncertainty, historical trends suggest a faster rebound in passenger traffic, which could make the industry’s long-term prospects more bullish,” says Ravi Shanker, equity analyst covering the North American transportation industry.

Just how bullish? Shanker says that, based on current operational conditions, air travel demand could return to pre-COVID levels by late 2021 or early 2022. However, near-term turbulence and vast operating and financial differences among airlines mean that investors will need to be selective about stock picks.

Weighing Passenger Demand

Demand, the biggest consideration for airlines in the COVID era, also offers the least visibility. To map the trajectory of demand recovery, Shanker and his team compared the pandemic with historical precedents of disruption and recovery. After previous demand shocks passenger volumes took about four years to return to pre-crisis levels, which explains the current consensus for a 2024 recovery.

However, compared with 2001 and 2008, the COVID disruption is deeper and more widespread. The severity of lockdowns and international border closings have created pent-up demand, by consumers and corporate travel alike, that could advance the recovery timeline. A Morgan Stanley AlphaWise survey from July 2020 indicated consumer interest in resuming air travel once a vaccine is available.

A recent Alphawise survey found a majority of corporate travel managers expect air-travel demand to return to pre-COVID travel levels by 2022.

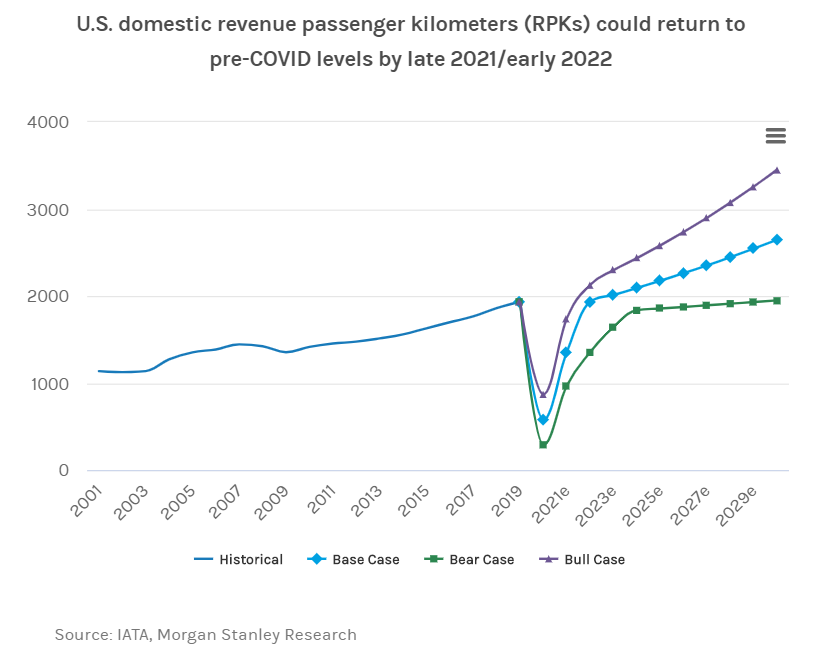

In their base case, Shanker and team forecast that U.S. revenue-passenger kilometers could return to pre-COVID levels by late 2021 or early 2022—with a bear case of 2024 that’s in line with the consensus—and a bull case of early 2021. How the U.S. and global nations navigate the pandemic’s trajectory and international border reopenings will no doubt affect these projections.

“Ultimately, even when we take the second or third wave of the pandemic into account, long term, we see very limited permanent demand substitution for air travel as a result of COVID, post-vaccine,” says Shanker.

U.S. domestic revenue passenger kilometers (RPKs) could return to

pre-COVID levels by late 2021/early 2022

The Nagging Supply Issue

Ongoing supply-side concerns have long nagged the industry.

The report’s analysts feel confident that management teams will quickly look to restore capacity flights to pre-COVID levels—especially when they no longer need to block middle seats for social distancing. Fewer domestic airlines and less competitive pressure also help.

Furthermore, load factor—a measure of flight capacity—jumped by four to five percentage points coming out of the past five U.S. economic downturns.

Load factors could snap back to as high as 70%, and available seat miles could reach 2019 levels by the second half of 2021, but fares/passenger revenue per available seat mile may take several years to bounce back—similar to the 2001 recovery.

Balance Sheet and Cost Actions

Thanks to the CARES Act, U.S. airlines have managed to control their cash burn, averting potential near-term liquidity issues. However, with the CARES Act expiring—and CARES 2 likely delayed until after the U.S. election—some airlines have already begun to trim costs with furloughs or layoffs, and may even start to cut passenger routes.

While the report doesn’t foresee widespread risk of bankruptcies, investors should favor companies with the most balance-sheet “firepower” and the least restrictions from government financial assistance.

Some Stability for Fuel Costs

A key question: How will jet fuel prices trade, as the world recovers? They fell by about 75%, after closed economies, borders and shelter-in place mandates grounded flights around the world.

“Jet fuel prices should stay relatively low and steady over the next one to two years, if crude oil prices hold steady,” says Shanker, something that could help U.S. airlines save money and support their positive medium-term outlook.

Given the strong correlation between jet fuel and oil prices, and the forward strip calling for Brent of $45-$55 a barrel over the next several years, Morgan Stanley estimates that jet fuel prices to be range-bound at $45-$65 a barrel—much lower than the 10-year historical average of around $90 a barrel.

For investors, near-term volatility and the industry’s uneven history of capacity discipline means quality still wins, says Shanker, who favors low-cost and ultra-low-cost carriers.

“Airlines with high domestic leisure exposure, medium length of haul (500-2,800 miles), strong customer loyalty and/or attractive fares will see demand come back first and have the best ability to play offense. Alternatively, airlines with high margins, relatively strong balance sheets and strong management teams that focus on passenger revenue per available seat mile will be the most defensive.”