Uddrag fra Authers:

SpaceX’s quest for space, the final frontier, threatens to take capital markets crashing through the efficient frontier. Key assumptions about how companies should be governed, how funds should be invested, and how markets can be benchmarked will come under assault in the forthcoming wave of IPOs led by Elon Musk’s space exploration conglomerate.

Bloomberg’s Big Take has a great roundup of the issues (co-authored by former Points of Return colleague Isabelle Lee), while Matt Levine has brilliantly explained the difficulties for index providers (who feel obliged to bend the rules to let the new companies into the benchmarks swiftly to avoid getting out of date) and for passive funds (who risk being massively gamed and used as a vehicle to force investors to channel money into the newly public companies).

The unicorn vogue, in which companies reached unprecedented size while staying away from the public gaze, will now give way to a new phenomenon in which giants are suddenly born fully fledged. As Nir Kaissar comments: “Companies are not supposed to show up on exchanges already the world’s most valuable businesses.”

The power that the founders intend to reserve for themselves, particularly SpaceX’s Elon Musk, is breathtaking; new investors can come along for the ride, but they can’t expect to exert any control. It all looks like quite fantastical hubris. (You can almost hear Kirk and Spock arguing.) If it doesn’t mark a historic market top, many will feel that SpaceX at least deserves t

All true. But it leaves aside the paramount question for many: Will these IPOs bring down the stock market? And at least at first, they probably won’t.

The reason for fear is simple enough. Markets for stocks, like all others, are driven by supply and demand. A huge increase in the supply of stocks should, all else equal, mean lower prices. And the splurge of supply that lies ahead is quite something, and spreads beyond the IPOs; Alphabet Inc. is planning to raise $80 billion, for example.

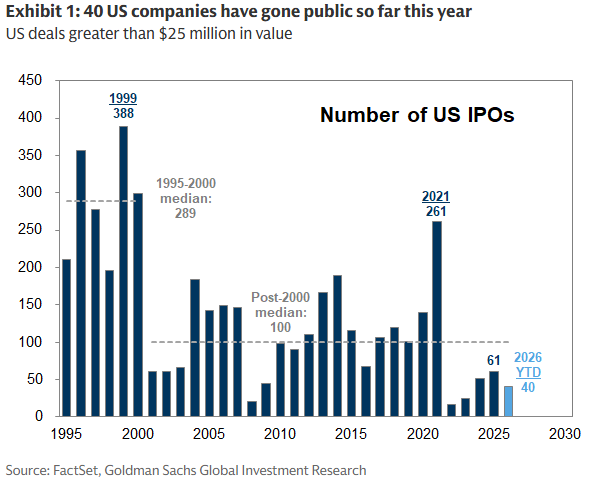

But we need some context. This gusher of new issuance comes after an unusually dry period. There are so many unicorns — private companies worth more than a billion dollars — because so many founders have decided to go public later in their development. Goldman Sachs’ equity strategist Ben Snider shows that IPOs have been in a steady decline, with a particularly fallow period since the burst of issuance in the post-pandemic boom of 2021:

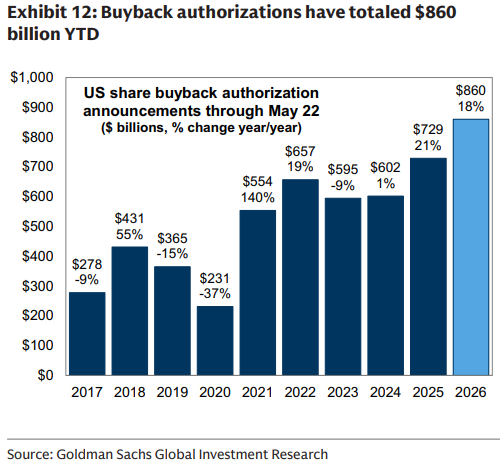

Further, companies have fueled demand for equity, as well as supply, through corporate buybacks, while dividends and cash payments have also shrunk the total amount of equity in circulation. As Snider shows, these are also going up:

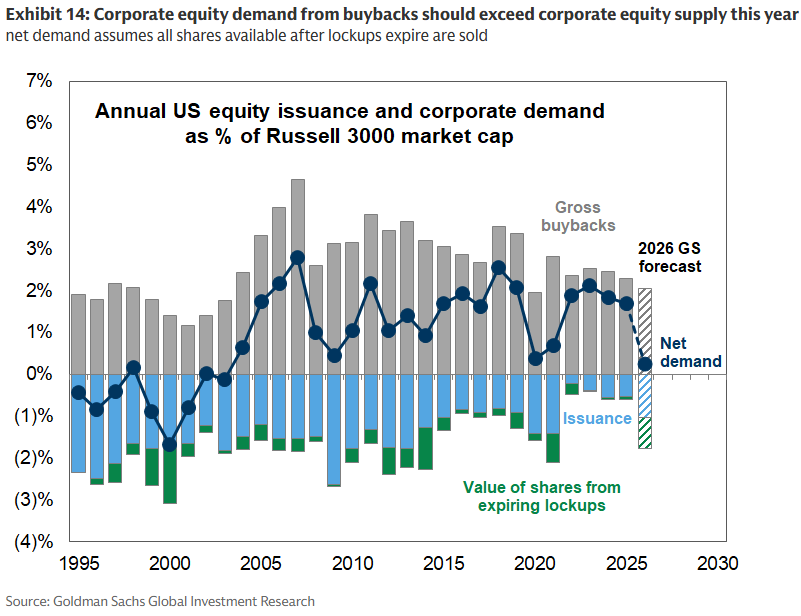

Rob Buckland, Citi’s chief global equity strategist for many years, gave this the ungainly name of “de-equitisation” back in 2003. In combination with exceptionally low interest rates, which make it worth a company’s while to borrow to retire equity — and also make the math of private equity work — it’s proved to be one of the most reliable trends in finance. As Snider shows, corporate equity demand has exceeded supply every year since Buckland coined the term:

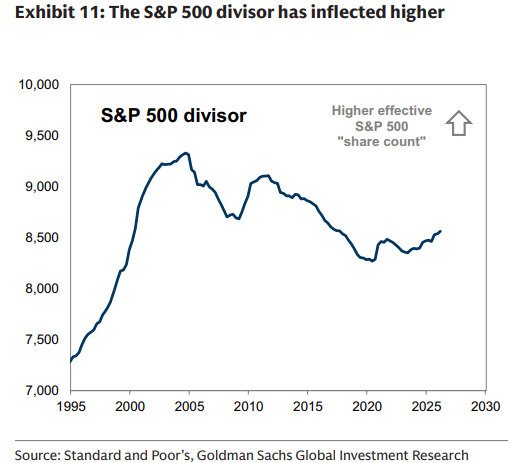

Alternatively, we can look at the divisor used to calculate the S&P 500, a measure of the number of shares. As Snider shows, it peaked in 2003, having exploded higher during the years of the dot-com bubble. It has declined with occasional interruptions ever since:

With private equity ruling the roost and ever more startups growing into unicorns without floating, so the supply of public equity has shrunk. The slivers that the new AI giants will be offering this year won’t turn that around.

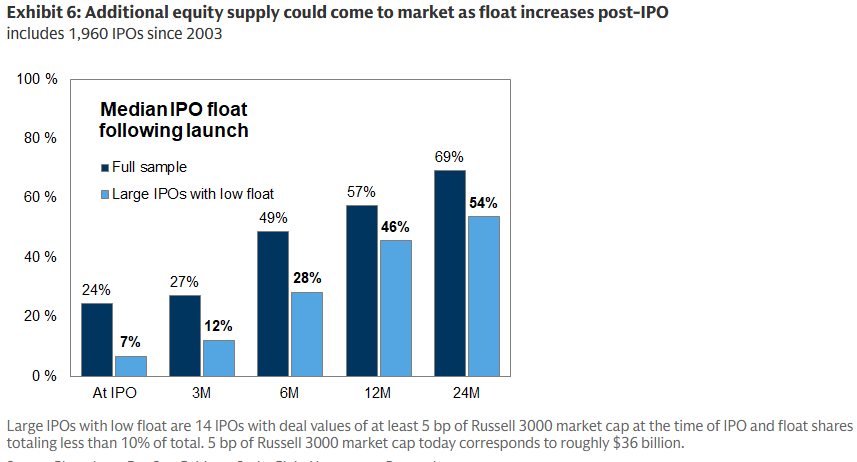

But that brings us to the issue of timing. Much more equity finds its way onto the market once the issue is up and running and lockups for founding executives are over. Goldman’s research shows that big companies with a very low float — putting only 7% or less on the market at IPO — have 54% of their shares in circulation two years later. For the full sample of IPOs it examined, a 24% float at the market debut had turned to 69% within 24 months:

If SpaceX, Anthropic, OpenAI and others follow this pattern, then the weight of new equity supply could well become unbearable next year or in 2028. These are unusually big companies whose leaders — particularly Musk — are unusual men who already have massive fortunes. SpaceX’s float might not grow as fast as the norm. But it would be wise to expect a continuing flow of supply from a company that many find exciting. That will make it harder for others to raise capital and force them to issue at cheaper valuations.

History isn’t encouraging. In the dot-com cycle, the chart further up the page shows that the peak in IPOs came in 1999 — and the top of the market and subsequent crash hit the following year as lockups ended and founders tried to make some cash.

Maybe we should pencil in the end of de-equitisation for 2027. Buckland himself suggests in an op-ed in the Financial Times that the days of the de-equitisation “put” are coming to an end, at least in the US. In the bull market of the 1990s, an equity capital markets banker once told him: “If the ducks are quacking, feed them.”

In a phrase that would baffle Spock, Buckland says: “In US big-cap tech, they have been quacking for some time… It finally looks like they are about to be fed.”