Merrill har analyseret den voksende kløft i væksten mellem USA og Europa. Kløften er vokset siden 3. kvartal sidste år – med stigende tendens i USA og faldende tendens i Europa. Det understreges af en enorm kløft i antallet af vacinationer og af nye lockdowns i Europa. Det kan få en negativ virkning på indtjeningen i de globale, amerikanske selskaber, som henter 55 pct. af deres ikke-amerikanske indtjening fra Europa, og det kan få dollaren til at stige. Da det også har geopolitisk betydning, kan det få en negativ virkning på de amerikanske kapitalmarkeder, mener Merrill.

What a Drag: What Divergent Transatlantic Growth Means for U.S.

Investors

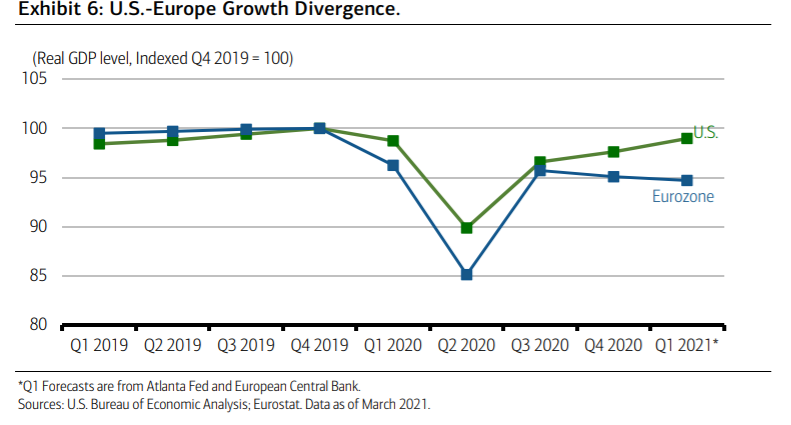

A year ago, the U.S. and the European Union (EU)—the world’s two largest economies—

were navigating the same economic storm wrought by the coronavirus. A year on,

however, Europe’s recovery has been driven off course, while America sails on to calmer

waters. As depicted in Exhibit 6, a significant growth gap has emerged between the U.S.

and Europe early in 2021.

America’s economic trajectory is upward owing to the double-barreled policy response

from Washington and coronavirus vaccines rollout that is now running at over 2 million

jabs per day. In Europe, meanwhile, the vaccine rollout has come late and has been

afflicted with miscues.

The result: Just 14 doses have been administered per hundred across the EU, versus 41 in the U.S.

Rather than reopening, many parts of Europe are shutting down—again. The tourist-dependent Mediterranean economies will likely face another lost summer; meanwhile, not one euro from Europe’s much-vaunted Recovery and Resilience fund announced last summer has yet to be spent.

The upshot: The eurozone area started the year in recession, while the U.S. powered ahead.

Europe’s drag on the transatlantic economy could potentially manifest itself in the

following ways:

• Weaker-than-expected global earnings for U.S. multinationals considering that the EU

accounts for roughly 55% of U.S. foreign affiliate income, a proxy for global earnings;

• A wider-than-expected U.S. merchandise trade deficit with Europe; the latter tallied a

near-record $175 billion last year and is poised to expand again this year; and

• Unexpected U.S. dollar strength, with U.S.-EU growth differential and spreads on U.S.

10-year bond yields versus German bunds clearly in favor of a stronger greenback.

In addition to all of the above, a weakened and divided EU isn’t much help in bolstering a

common transatlantic front when it comes to dealing with China, North Korea, Middle East

tensions and Russia. The heavy lifting—not for the first time—will likely fall to the U.S. In

the end, Europe’s a drag, with clear implications for the U.S. capital markets.