Resume af teksten:

Seks ud af ti hollandske husstande planlægger at reducere forbruget som følge af stigende energi- og brændstofpriser ifølge ING’s daglige undersøgelse. Krigen i Iran har forårsaget en stigning i olie- og gaspriserne, og over 80% af forbrugerne forventer, at disse forhøjede priser vil vare i mindst tre måneder. Denne udvikling har øget hollandske forbrugeres inflationforventninger for de kommende 12 måneder til 3,7% årligt. Mere end en tredjedel af husstandene forventer at skulle skære betydeligt ned eller endda møde økonomiske vanskeligheder. Specielt ikke-essentielle kategorier som rejser og fritidsaktiviteter er målrettet for besparelser. På makroniveau forventes husholdningsforbruget at vokse med 0,5% i 2026 og BNP med 1,0%, selvom forbrugsvæksten nu er mere afdæmpet end før krigen. Regeringen overvejer målrettede tiltag for at hjælpe lavindkomstgrupper og mindske påvirkningen.

Fra ING:

Six in 10 Dutch households intend to cut back on spending in response to higher energy and fuel prices, according to ING’s daily survey. Although such pessimism dampens the outlook for consumption and GDP in the Netherlands for 2026, an expansion is still expected

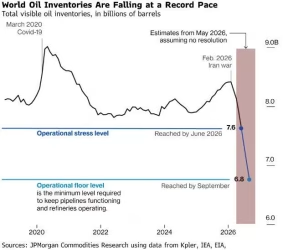

The Iran war has sharply driven up oil and gas prices. Consumers in the Netherlands expect such elevated fuel prices to persist. Among respondents to ING’s daily Question of the Day survey, more than 80% believe elevated prices will last three months or longer.

As early as March, these expectations pushed Dutch consumers’ median inflation expectations for the coming 12 months up noticeably to 3.7% year-on-year. The resulting erosion in purchasing power will clearly dampen consumer sentiment. In April, confidence fell to the lowest level since December 2022.

Most households expect a noticeable financial impact

First and foremost, there’s a widespread belief that prices are putting pressure on Dutch household budgets. Only a small minority of households expect to feel little or no impact from higher prices. The vast majority of Dutch households anticipate a tangible strain on their finances amid higher prices. More than one in three expect to have to cut back materially or even run into financial difficulties. This highlights that, while average household financial positions remain relatively solid, the distributional impact of higher prices matters for consumption patterns.

Large majority of Dutch consumers expect financial impact from higher prices; one third will have to cut back

Share of respondents* who answered the multiple‑choice question: “To what extent do you expect higher prices due to the war in Iran to be a financial burden for your household?”

Large majority of Dutch consumers expects a financial impact from higher prices; one third will even have to cut back

Source: ING Question of the Day (Vraag van Vandaag), calculations by ING Research; *Approximately 30,000 responses to a question asked on 26 March 2026 among ING private customers in the Netherlands; reweighted for representativeness based on age, gender and prov

Majority signal spending cutbacks, often in discretionary categories

Around 60% of consumers cite higher prices as a reason to cut back on spending. Four in 10 households report making behavioural changes to cut their energy and fuel use, such as driving fewer kilometres or turning down the thermostat.

Past energy price shocks show that cutting energy and fuel use meaningfully in the short run is difficult, largely because commuting needs and limited control over home energy efficiency constrain how much households can adjust. Consistent with this, most households that intend to cut back plan to do so by reducing spending in other areas instead. After fuel and energy, hospitality, holidays and leisure activities are most frequently mentioned as cost-cutting categories. Essential items such as groceries are less often targeted for savings.

Most consumers say they are cutting back due to high prices

Response from respondents* in the Netherlands to the multiple-choice question: “Which spending are you cutting back on the most as a result of higher prices caused by the war in Iran?”

Most consumers say they are cutting back due to high prices

Source: ING Vraag van Vandaag, calculations by ING Research; *Approximately 27,000 responses to a question asked to ING customers on 28 November 2025, reweighted for representativeness based on age, gender, and province of residence.

Surveys signal intentions, not certainties

It is important to stress that survey results capture intentions rather than realised behaviour. Historically, consumers do not always act in line with what they say they plan to do. This may particularly be the case when labour markets remain tight and incomes continue to rise. Although the survey data clearly signals growing caution, it remains unclear how far these intentions will translate into actual, broad‑based spending restraint in the coming quarters.

Targeted government support could limit downside risks

Targeted government measures could help cushion the impact on vulnerable households somewhat and, in doing so, support short-term economic activity. Recent policy announcements primarily focus on lower-income groups and energy-saving measures. Survey evidence suggests that such targeted income support enjoys the broadest public backing by consumers.

Any proposed support measures are generally preferred to government inaction. While such policies – especially given their modest scale so far – are unlikely to eliminate all consumer financial concerns, they could still moderate the tendency of some households to make sharp spending cutbacks.

Growth outlook: more subdued, but still positive

At the macroeconomic level, increased consumer caution implies some additional headwinds to growth. Nevertheless, we do not currently see any indications of an imminent household purchasing strike. Households entered the period before the Iran war from a relatively good position, supported by solid wage growth and low unemployment.

As a result, household consumption is still expected to grow in 2026. However, compared with expectations before the Iran war, consumption growth is now projected to be more muted, reflecting higher inflation, weaker confidence and a greater propensity to save. In that sense, the outlook has softened. But it has not yet turned fundamentally negative.

Our latest forecast for 2026 is for household consumption to expand by 0.5% and GDP by 1.0%. That is mediocre, but not a recession. A shift to a more negative scenario would require further deterioration in upcoming data.

Hurtige nyheder er stadig i beta-fasen, og fejl kan derfor forekomme.