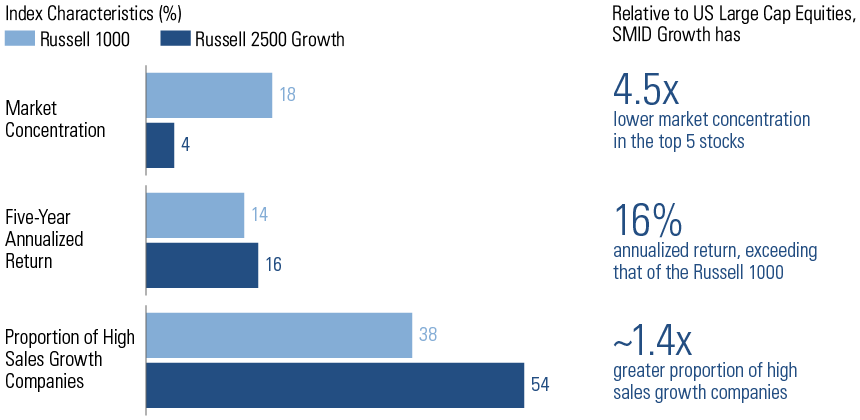

Goldman Sachs har analyseret de mindre selskaber og deres performance i forhold til de store og velkendte firmaer, og banken konkluderer, at der er rigtigt mange gode investeringsmuligheder, som ligger gemt under radaren – ingen lægger mærke til dem. Selv de fem største selskaber blandt selskaberne i indekset for de mindre, Russell 2500, udgør kun 4 pct. af indeksværdien, mens de fem største i Russell 1000 indekset for de store selskaber udgør 18 pct. af værdien. De udgør en chance for investorerne uden at øge risikoen. Mere end halvdelen af de mindre selskaber i Russell-indeksene har en vækst i omsætningen på over 8 pct., og de giver et årligt afkast på 16 pct. mod 14 pct. for de store selskaber.

Below the radar

SMID growth may offer investment variety without sacrificing returns

Leaning into companies with smaller public profiles may be an option for reducing concentration risk while seeking exposure to “growth” characteristics. The five largest companies in US small and mid-cap (SMID) growth make up only 4% of the index, relative to US large cap at 18%.

Yet historical performance between these indices has been similar given the sector composition—info tech, healthcare, and consumer discretionary make up ~60% of both indices.

Additionally, more than half of SMID growth companies have sales growth above 8%. We think these features make SMID growth an attractive response to the risk of regulation and concentration.

Source: Bloomberg and GSAM.

Top Section Notes: As of November 30, 2020. Chart shows the US equity market concentration based on the market capitalization of the largest five companies in the Russell 1000 Index. Shading reflects US recessions. ‘Average’ refers to the long-run average from January 1995–November 2020. Bottom Section Notes: As of November 30, 2020. Chart shows characteristics of the Russell 1000 Index (US Large Cap Equities) and Russell 2500 Index Growth (SMID Growth) across market concentration, annualized return, and proportion of high sales growth companies. Diversification does not protect an investor from market risk and does not ensure a profit. ‘Market concentration’ refers to the market capitalization of the largest five companies for the Russell 1000 and Russell 2500 Growth indices, respectively. ‘Annualized return’ refers to the five-year gross total annualized return of the Russell 1000 and Russell 2500 Growth from December 2015–November 2020, inclusive. Companies with ‘high sales growth’ have annual sales growth of 8% or greater. For illustrative purposes only. Past performance does not guarantee future results, which may vary.